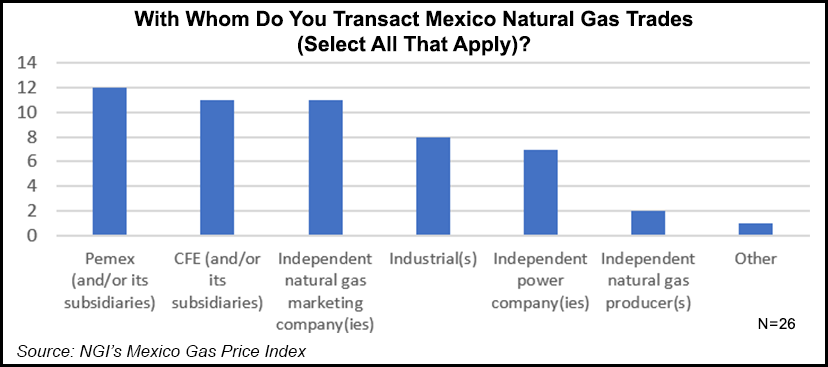

Private sector shippers are starting to make their presence felt in the Mexican natural gas market, according to the second survey of natural gas buyers and sellers in Mexico conducted by NGI’s Mexico GPI.

In response to the question, “With Whom Do You Transact Mexico Natural Gas Trades?” Mexican state entities Comisión Federal de Electricidad (CFE) and Petróleos Mexicanos (Pemex) led the list, but independent marketers featured in some way in 42% of total responses, tied with CFE and second only to Pemex.

“CFE, Pemex, and independent marketers basically came in a tie for first place,” said NGI’s Patrick Rau, director of strategy and research. “This is a statistical sampling and may not necessarily represent the actual population. As such, we believe CFE and Pemex...