Markets | E&P | LNG | NGI All News Access | NGI The Weekly Gas Market Report

Haynesville’s Soaring Natural Gas Output Said Sustainable as LNG Exports Grow

Natural gas production in a former darling of the onshore unconventionals, the Haynesville Shale, is getting serious looks from new suitors, including operators looking for export stores, with production on course to hit record heights, according to Rystad Energy.

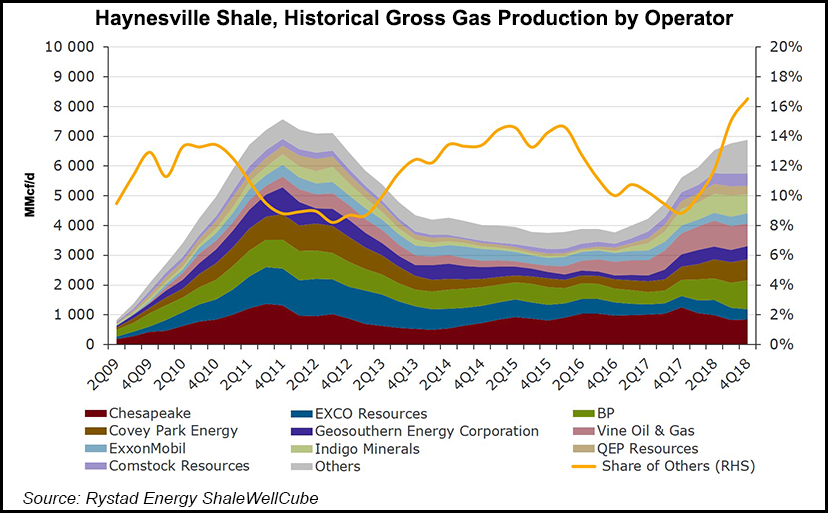

Rystad Energy research indicates the Haynesville, which straddles East Texas and northern Louisiana, was able to add 1.85 Bcf/d gross between 4Q2016 and 4Q2017 as its resurgence began. Last year, another 1.3 Bcf/d was added.

Production needs to increase by another 700 MMcf/d to hit all-time highs last seen in 2011.

“We conclude that Haynesville Shale’s revival, for the second year in a row, looks sustainable,” Rystad partner Artem Abramov said.

He pointed to the play’s proximity to liquefied natural gas (LNG) export terminals along the Gulf Coast, including Cheniere Energy Inc.’s up-and-running Sabine Pass facility in Louisiana.

“Achieving new all-time high gas production levels should happen within a matter of months,” Abramov said.

Driven by continued expansions at the Sabine Pass project, which began exporting gas just as Haynesville output began to increase, domestic exports increased substantially last year.

Rystad is forecasting domestic LNG production this year to surpass 40 million metric tons/year (mmty) as liquefaction capacity is set to double. Additional project ramp-ups are scheduled in Texas (Freeport and Corpus Christi), Louisiana (Cameron) and Georgia (Elba Island).

Currently sanctioned LNG plants are expected to produce about 65 mmty by 2022, and Rystad is forecasting U.S. output to reach 150 mmty by 2030.

“The demand for U.S. LNG is driven by the Asian market, where China, India and emerging markets will account for the largest portion of the growth,” senior analyst Sindre Knutsson said. “Rystad Energy forecasts global LNG demand to reach 560 mmty by 2030, with Asia accounting for more than 75% of total volumes.”

Before the collapse in U.S. gas prices in the second half of 2008, the Haynesville was considered to be one of the world’s most prospective gas reservoirs, with the capability to drive growth in domestic production for years.

However, sustained low gas prices from 2009 to 2011 “effectively derailed its growth prospects,” and the Appalachian Basin’s lower cost reserves drew more prospectors to the Northeast.

“After peaking in 4Q2011, gas production in Louisiana entered into a multi-year decline phase, losing almost 4 Bcf/d by the fourth quarter 2016,” according to researchers.

“Haynesville Shale is truly a different play today than it was in the first growth phase,” Abramov said. “Well productivity doubled from 2012 to 2018 measured in initial production rates and current estimated ultimate recovery. Even when productivity is normalized per perforated lateral foot, we observe 20-40% improvement over the last six years.”

Robust well productivity and low development costs in part are attributed to updated completion techniques by the play’s top three oilfield service (OFS) providers: Schlumberger Ltd., Halliburton Co. and BJ Services. The OFS operational efficiencies are considered “central to the Haynesville renaissance,” said the Rystad team.

“The clear trend we saw in Haynesville over the past six years has been a dramatic increase in the market share of Halliburton, Schlumberger and BJ Services,” Abramov said. “In 2015, Halliburton was able to increase its market share to 40% from 10%. Schlumberger reached a 28% market share in 2018. Combined, Halliburton, Schlumberger and BJ Services now account for 90% of the Haynesville market.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 | ISSN © 1532-1266 |