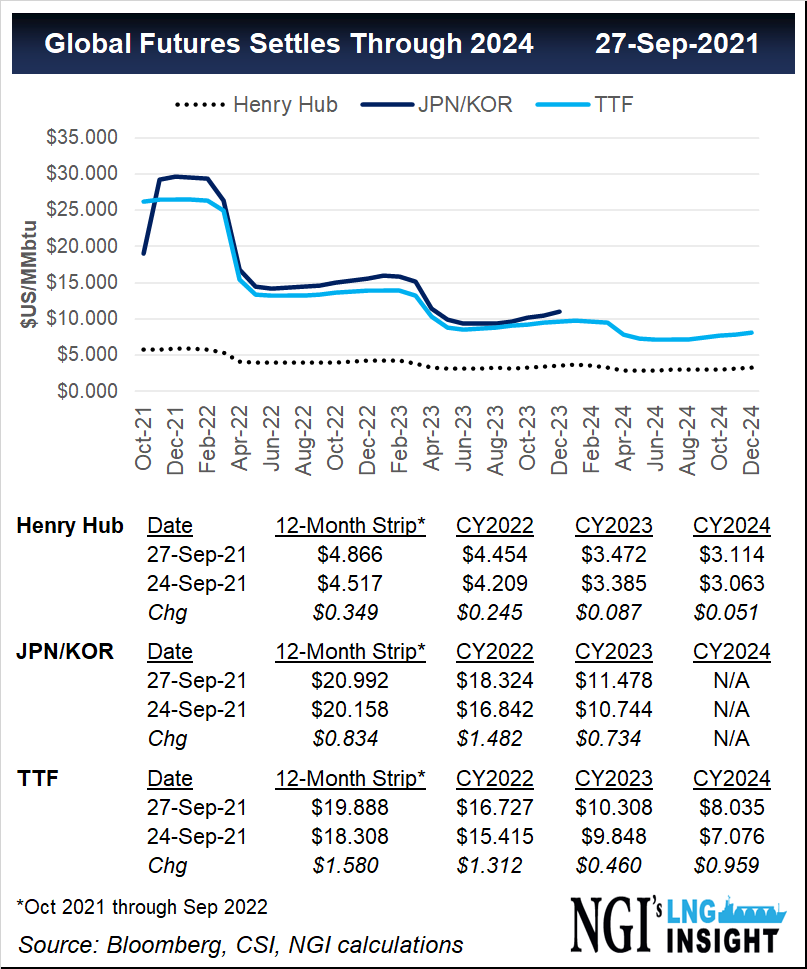

Natural gas prices across the world climbed higher on Tuesday, fueled by the prospect that there will be energy shortages from Europe to Asia this winter.

British and Dutch benchmarks closed higher Tuesday, beating an all-time record set Monday after finishing close to $30/MMBtu. In the United States, prices also continued climbing toward $6 as the October contract was set to expire Tuesday, also surpassing a high for 2021 on Monday. In Asia, spot liquefied natural gas (LNG) prices for the second half of October were assessed at more than $31.

Coal, carbon and wholesale power prices have also surged as power generators across the world scramble to meet demand.

“Concerns are still big regarding supply during the coming winter, as storage levels are still well below the...