Russian natural gas exports to foreign markets dropped nearly 46% year/year in 2022, when they were impacted by a steep decline in deliveries to Europe, according to Gazprom PJSC.

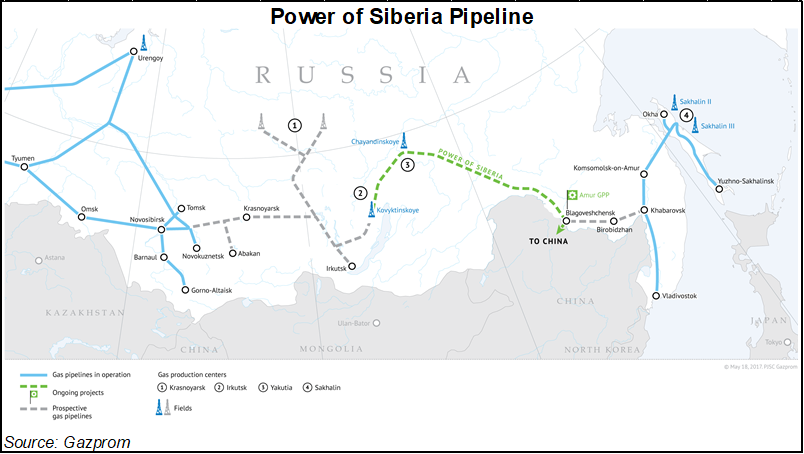

Exports, including those to China via the Power of Siberia Pipeline, dropped to 100.9 billion cubic meters (Bcm) last year, or about 3.6 Tcf. That’s compared to 185.1 Bcm, or roughly 6.5 Tcf, in 2021.

Gazprom had a “very, very difficult” year, Gazprom Chairman Alexey Miller reportedly said at a conference late last month. Gazprom produced 412.6 Bcm of natural gas last year, a 20% decline from 2021 volumes, he said.

“Gazprom will not be able to find any substantial new export outlets over the next decade,” said Jonathan Stern, a senior research fellow at the Oxford Institute for Energy...