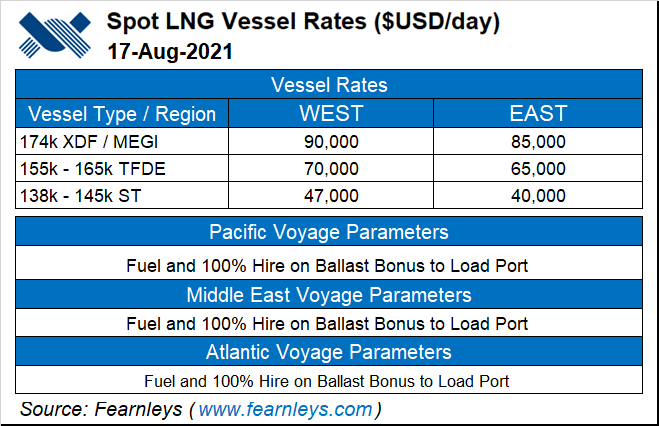

The liquefied natural gas (LNG) shipping market is expected to tighten in the coming years as carrier owners fill charters and older, higher emitting vessels are pushed out of the market, Flex LNG Ltd. CEO Øystein Kalleklev said.

One-year term charter rates have risen since the start of the year as global LNG demand has increased amid a colder-than-expected winter and easing Covid-19 restrictions. For standard 155,000-165,000 cubic meter carriers, day rates have gone from about $50,000 at the end of 2020 to about $80,000 currently, according to Flex, citing data from Fearnleys. Day rates have shot even higher for the newer, 170,000-cubic meter carrier models favored by Flex, from about $60,000 at the end of 2020 to $115,000 currently.

“This illustrates that market...