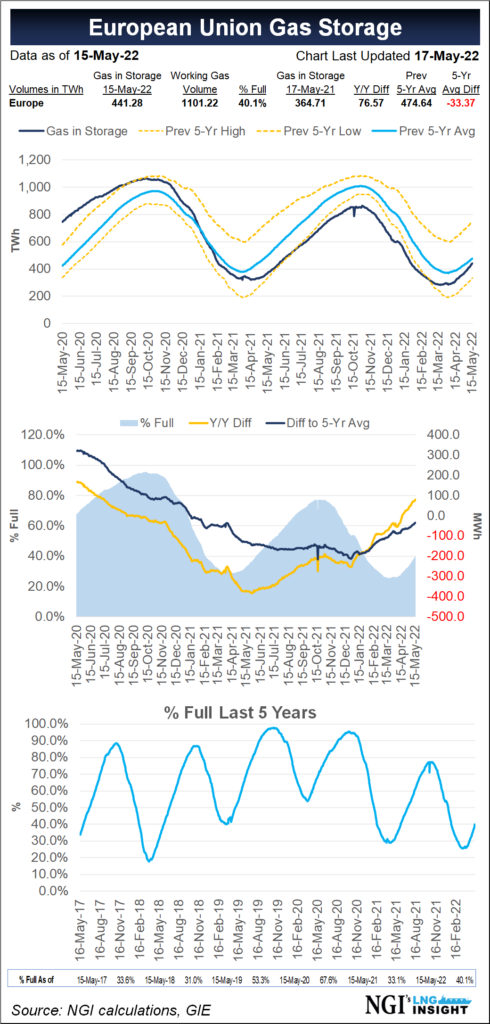

Europe’s natural gas storage inventories continue to rise at some of the fastest rates on record as an influx of liquefied natural gas (LNG) cargoes lands on the continent to take advantage of strong prices.

Storage stocks are at roughly 40% of capacity, which is below the five-year average of about 45%, but roughly aligned with the previous 10-year average. Injections have accelerated since the beginning of April, according to data from Gas Infrastructure Europe.

The shift by the European Union (EU) away from Russian fossil fuels after the invasion of Ukraine, combined with the need to refill depleted storage inventories after winter and lackluster demand in Asia, is driving more LNG cargoes to Europe.

Demand for delivery slots remains strong, prompting sellers without...