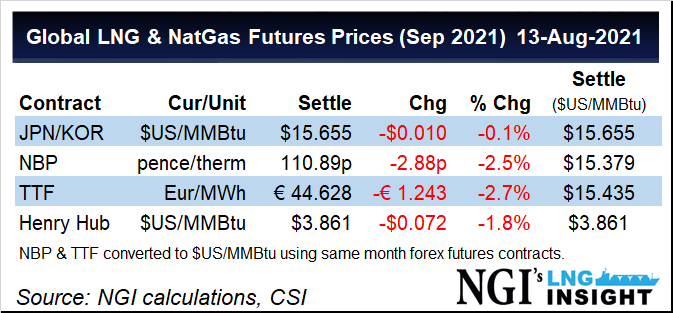

European natural gas prices again set records Monday as Russian pipeline imports were poised to fall further next month, exacerbating fears that the continent would be short of supplies this winter as storage inventories remain low.

Gazprom PJSC booked a fraction of the 15 million cubic meters (MMcm) of firm transportation capacity available through Ukraine for September. The company took just 650,000 cubic meters of the capacity to move natural gas to Europe, according to auction data released Monday.

“European gas fundamentals remain tight, with the persistent weakness of Russian supply as the main source of concern,” Engie EnergyScan analysts said in a note Monday.

Engie said Russian flows slipped to 267 MMcm Friday, down from 268 MMcm on Thursday. They’ve...