Markets | E&P | LNG | NGI All News Access

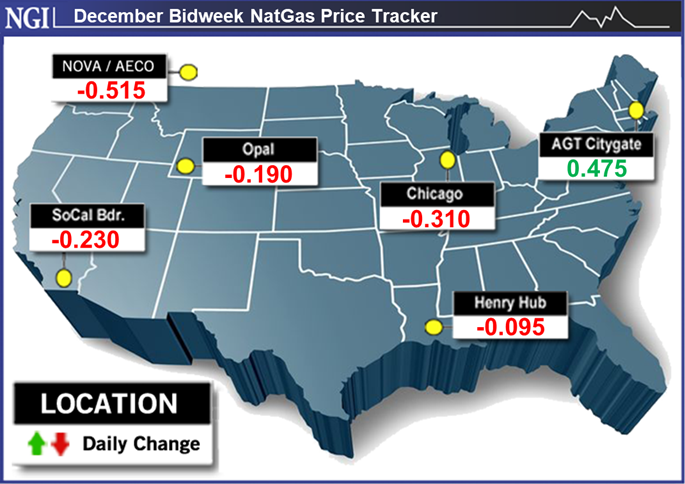

December Natural Gas Bidweek Prices Slip Lower Amid Mild Temperatures, Dubious Outlook

Share on:

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1258 | ISSN © 2577-9877 |

Markets | E&P | LNG | NGI All News Access

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1258 | ISSN © 2577-9877 |

Energy Transition

Natural gas end users are increasingly focused on sustainability and have shown a keen interest in the availability of low carbon fuel options. Still, the question often arises – are they willing to pay a premium? At the recent LDC Gas Forums Southeast in Ponte Vedra Beach, FL, executives of local distribution companies and natural…

April 25, 2024By submitting my information, I agree to the Privacy Policy, Terms of Service and to receive offers and promotions from NGI.