Editor’s Note: NGI’s Mexico Gas Price Index, a leader tracking Mexico natural gas market reform, is offering the following column by Eduardo Prud’homme as part of a regular series on understanding this process.

With the constitutional reform proposal for the energy sector shot down, President López Obrador will find it hard to reverse the structural energy reform that occurred in 2014. Most likely, the legal framework in force in December 2018 will essentially prevail. However, presidential power will continue to hamper private participation in the sector. In terms of projects, what can we expect to change or happen in the natural gas market from now until the end of his presidency on October 1, 2024?

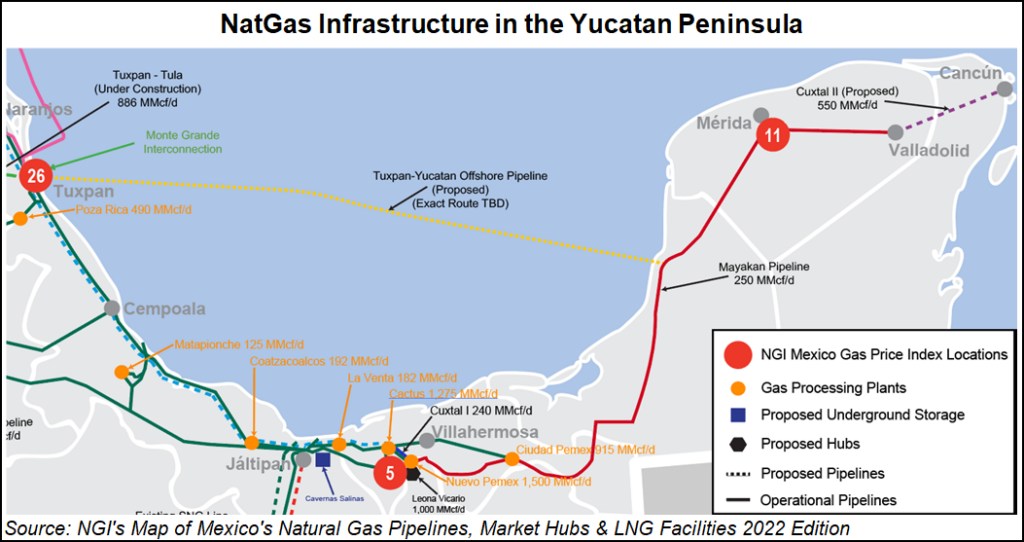

AMLO, as the president is called, has within his reach a simple...