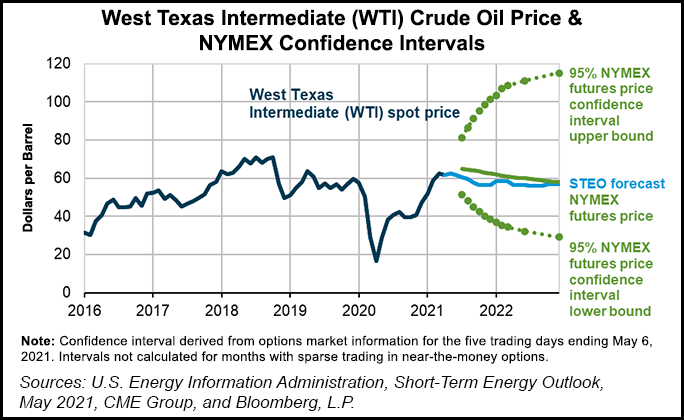

Brent crude oil prices are set to average $65/bbl during the second quarter before declining to $61 for the second half of 2021, the Energy Information Administration (EIA) said in the May edition of its Short-Term Energy Outlook (STEO).

In the report, published Tuesday, EIA said Brent prices averaged $65 in April, unchanged from March. This comes as the market has “considered diverging trends in global Covid-19 cases,” researchers wrote.

“In some regions, notably the United States, oil demand is rising as both Covid-19 vaccination rates and economic activity increase,” EIA said. “In other regions, notably India, oil demand is declining because of a sharp rise in Covid-19 cases.”

After sliding to $61 for the second half of this year, Brent prices are set to remain...