Markets | Natural Gas Prices | NGI All News Access

Bearish Storage Injection Curtails Furious Rally for October Natural Gas Futures

Share on:

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |

Markets | Natural Gas Prices | NGI All News Access

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |

Markets

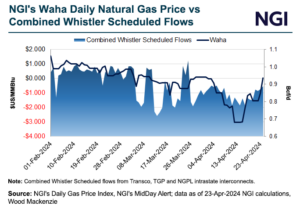

Natural gas futures finished higher Tuesday after a choppy session that began in the red, supported by a rebound in U.S. LNG exports and a blitz of pipeline maintenance that sent gas production estimates lower. At A Glance: West Texas prices flip positive MVP pipeline ready to start in May Production falls below 97 Bcf/d…

April 23, 2024By submitting my information, I agree to the Privacy Policy, Terms of Service and to receive offers and promotions from NGI.