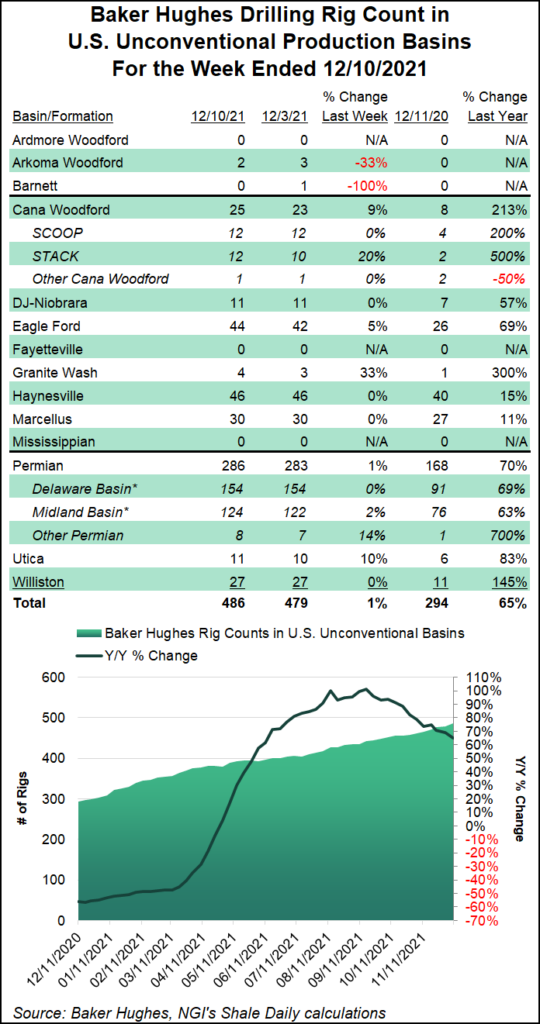

A result of gains in both oil and natural gas-directed drilling, the combined U.S. rig count climbed seven units to 576 for the week ended Friday (Dec. 10), according to updated figures from Baker Hughes Co. (BKR).

Four oil-directed rigs and three natural gas-directed units were added in the United States for the week, putting the overall domestic tally 238 units ahead of its year-earlier total, according to the BKR numbers, which are partly based on data from Enverus.

Six U.S. rigs were added on land, along with one in the Gulf of Mexico. Eight horizontal rigs were added, partially offset by a one-rig decline in vertical units.

The Canadian rig count fell three units to 177 for the week, up 66 rigs year/year. The three-rig net decline there was focused entirely in the oil...