NGI Data | NGI All News Access

Cash, Futures Put Up Double-Digit Gains In Shortened Pre-Holiday Weekly Trading

Share on:

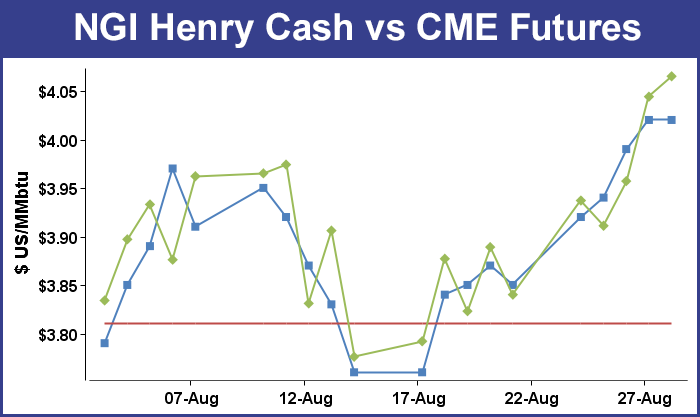

By the end of the four-day trading week ended August 28, bulls had clearly gained control with all high-traffic market points in the black and the NGI Weekly Spot Gas Average posting a healthy 11-cent rise nationally to $3.71.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |