NGI Data | NGI All News Access

Weekly Quotes Gain; Futures Bulls Savoring Storage Data

Traders and marketers can breathe something of a sigh of relief that the mind-bending volatility of the winter is past, but market bulls were treated to the first storage report of the newly-minted injection season.

The reported build of just 4 Bcf was music to their ears, and for the week ended April 11, the NGI Weekly Spot Gas Average rose 6 cents to $4.55. The majority of points registered gains of anywhere from a few pennies to about 20 cents, and losses were mostly confined to the Midwest where all points were in the red about a nickel. Of the actively traded points Tennessee Zone 4 Marcellus had the greatest gains, adding 22 cents to average $3.83 and the Algonquin Citygates were the biggest loser dropping 61 cents to $4.73.

From a regional perspective the Midwest was down 6 cents to $4.78 and the Midcontinent was slightly improved with a decline of 2 cents to $4.45.

Both the Rocky Mountains and Northeast added a nickel to $4.43 and $4.35, respectively, and California was higher by 7 cents to average $4.79.

Texas and Louisiana proved to be the week’s regional winners. East Texas was higher by 15 cents to $4.53 and South Texas added 17 cents to $4.47. South Louisiana was up 18 cents to $4.54.

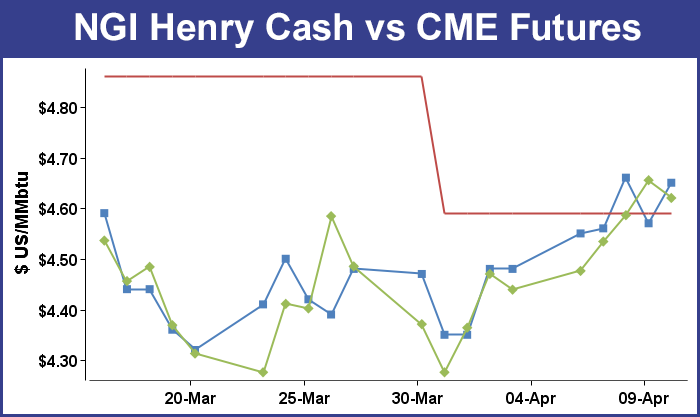

For the week May futures added 18.1 cents to $4.620.

Futures traders see the market as within a narrow range for the moment. “I think the market will have a tough time running up next week. I look for a range of $4.65 on the top and back to $4.45 on the bottom,” said a New York floor trader. “It looks like a trading range, but the range has just ratcheted up,” he said. “From May to October the whole board trades together. There’s no [financial] incentive to store gas.”

Market observers saw Thursday’s response to the thin 4 Bcf gas storage build as “…exaggerated, but the lift above our expected resistance at $4.61 appeared to trigger some additional speculative short covering,” said Jim Ritterbusch of Ritterbusch and Associates in closing comments Thursday to clients. “We had suggested taking profits at the $4.61 level or higher, and we are leaving open the likelihood of a reaction back down into the $4.50-4.60 zone where we will look to establish long holdings. Looking out through next week, [Thursday’s] action reinforced our ultimate expectation for a climb up to the $4.80 area.

“Storage at 826 Bcf is now roughly 1 Tcf below the five-year average. While we don’t expect the market to close this entire gap by next fall, we do feel that at least 70% of this shortfall will need to erase in order to provide adequate winter supply. This narrowing in the shortfall of some 100 Bcf/month will continue to require an elevated pricing environment, even allowing for structural uptrends in production. All in all, we are maintaining a bullish trading opinion and we suggest working this market strictly from the long side.”

Others aren’t too worried for the moment about the slow start to the injection season. “While we remain relatively constructive on US natural gas prices, we are attempting not to read too much into the recent modest pace of injections. After all, the industry started last year’s injection season off to a slow start (April 2013 injections were the lightest recorded since 2007),” said Teri Viswanath, director of commodity strategy at BNP Paribas. “Therefore, light restocking in April is probably not indicative of the overall trend for the rest of the injection season. However, the current slow start to restocking increases the odds that the industry will not be able to build a large enough inventory buffer to prevent the possibility of winter-time price shocks.”

Ahead of the release of storage data by the Energy Information Administration Thursday, some were optimistic for a smooth storage refill. John Sodergreen, editor of Energy Metro Desk (EMD), suggested that refill will go smoothly, with ample gas in inventory by the end of October. “The next eight-10 weeks of inventory builds will largely set the tone for the rest of the year. It remains our belief that we will get very close to record tallies by the end of the season in November. EIA tells us that production is up a few points but demand is up far less.” Sodergreen’s EMD poll showed an average 15 Bcf build.

Others saw about the same. A 15 Bcf increase compared to last year’s 25 Bcf pull and the five year injection pace of 9 Bcf. ICAP calculated a build of 14 Bcf and a Reuters poll of 23 traders showed an average 13 Bcf with a sample range of +4 to +20 Bcf. Tradition Energy calculated an increase of 18 Bcf.

With the lean 4 Bcf injection inventories now stand at 826 Bcf and are 849 Bcf less than last year and 997 Bcf below the 5-year average. In the East Region 5 Bcf were withdrawn and the West Region saw inventories unchanged.. Inventories in the Producing Region rose by 9 Bcf. The Producing region salt cavern storage figure increased by 8 Bcf from the previous week to 68 Bcf, while the non-salt cavern figure rose by 1 Bcf to 294 Bcf.

In Friday’s trading gas for physical delivery over the weekend and Monday worked lower as weather-driven declines in the East and Northeast were able to offset broader market strength in the Midcontinent, Rockies and Great Lakes. Futures traders said the day’s setback may set the stage for more rangebound trading and at the close May had lost 3.5 cents to $4.620 and June had fallen 3.6 cents to $4.635.

Friday forecasts of the warmest weather in months in the East were enough to send buyers packing. “The warmest weather since last autumn is in store for much of the East spanning Sunday and Monday and will feature 80-degree temperatures in some locations. The warmup may bring a surge in pollen as well,” said Alex Sosnowski, AccuWeather.com meteorologist. “After a winter and early spring where temperatures have averaged well below normal, it will feel like summertime for a day or two in much of the East. Mild air building in the Eastern states through Saturday will be just a tease compared to the warmth coming Sunday into Monday for many areas east of the Mississippi River.

“The warmth is likely to reach all the way into northern New England and the Maritimes. Only locations with a southern exposure to chilly ocean, sound or bay waters will stay relatively cool. For most areas in the mid-Atlantic, Sunday will be the warmer of the two days as cloud cover and showers will begin to invade the region. For much of New England, New Brunswick, Nova Scotia and Prince Edward Island, Monday will be the warmer of the two days, thanks to a stiff southwesterly wind. Despite Monday’s warmth, temperatures will stop short of record levels in most areas. For many locations, record highs this time of the year are well into the 80s and lower 90s.”

The high Friday in Boston of 65 degrees was expected to hold Saturday before jumping to 73 Monday. The normal high in Boston is 54, according to AccuWeather.com. New York City’s Friday high of 74 was seen dipping to 68 Saturday before making it back to 74 on Monday. The seasonal high in New York City is 60. In the nation’s capital the high Friday of 78 was predicted to slide to 73 Saturday before making it to 78 Monday. The normal mid-April high for Washington, DC, is 66.

“The [East] market area is pretty mild, and no one wants to buy gas over a weekend with weather like that,” said an industry veteran.

Gas for delivery over the weekend and Monday on Tetco M-3 shed 46 cents to $3.79, and gas bound for New York City on Transco Zone 6 fell 65 cents to $3.57.

Marcellus and Appalachian locations were also weak, but gas on Columbia rose slightly. Deliveries to Transco Leidy fell 58 cents to $3.20, and deliveries to Tennessee Zone 4 Marcellus shed 44 cents to $3.33. Gas on Dominion South was lower by 38 cents to $3.68, but packages on Columbia Gas TCO rose 2 cents to $4.50.

Both Columbia TCO and Dominion are in close proximity but incur different market dynamics. “Dominion is a pipe which is long production. Everyone is trying to move gas off Dominion to a higher market area,” said the industry veteran. He added that Columbia Gas TCO was better situated to handle storage injections, and demand for storage gas could be keeping the price firm.

Physical traders trying to move gas into New England had to deal with scheduled maintenance for Algonquin’s Southeast Compressor station. Industry consultant Genscape reported that the work is “scheduled to start on Monday the 14th and lasts till the 27th. Capacity through Southeast will be reduced from a seasonal capacity of 1,200,000 Dth/d to approximately 1,065,000 Dth/d. Flow through Southeast CS averaged 1,300,000 Dth/d in the past week with an operational capacity of 1,418,000 Dth/d. This maintenance will likely force AGT [Algonquin Gas Transmission] to restrict interruptible and potentially secondary firm out of path and secondary in-path firm services for about 250,000 Dth/d.”

New England points were also down hard. Deliveries to Algonquin Citygates shed 54 cents to $4.08 and gas into Iroquois Waddington fell 4 cents to $4.63. Gas on Tennessee Zone 6 200 L fell 28 cents to $4.41.

Going into the weekend neither the bulls nor bears had a lot to hang their hats on, weather-wise. Commodity Weather Group in its morning six- to 10-day outlook showed below-normal temperatures across the eastern half of the country, with some above-normal temperatures in the Mountain West, California and Pacific Northwest. Market-wise, there may be some slowing in the rate of injections, but large-scale weather events this time of year are unusual.

“Great agreement continues on next week’s large scale cool to cold outbreak from a macro standpoint, but the various ensembles continue to disagree on the intensity details of the event with the American and Canadian ensembles still cooler than our outlook and the European guidance,” said Matt Rogers, president of the firm. “Given the time of year with bigger limitations on cold air capabilities, we continue to prefer the more cautious route offered by the European guidance.

“Either way, the modeling agrees on moderation in the pattern late next week into the 11-15 day period with still a more variable situation and lower forecast confidence. The best agreement is on continued warmer than normal weather in the Southwest and California. Less agreement is still noted in the East, but the range is mainly between more seasonal or slightly cooler levels yet again.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |