NGI Weekly Gas Price Index | NGI All News Access | NGI Data

Weekly Prices Post Record Decline; Nearly All Points Take Hard Fall

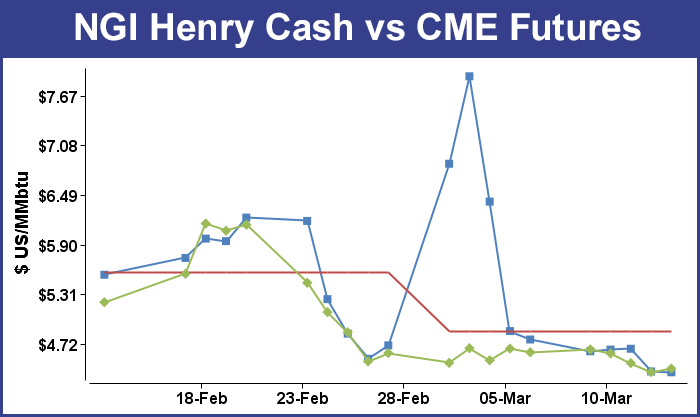

Weekly national spot gas prices suffered the worst drubbing since NGI began keeping score in Sept. 1999 as traders began to eye the finish line of what will go down in the history books as one of the most frigid winters in memory. The NGI National Weekly Spot Gas Average plunged a gut wrenching $3.15 to average $5.03 for the week ended March 14. The previous record was the decline of $1.90 to $7.53 seen Feb. 14, 2014.

Only one Marcellus point dodged the cascade of falling prices, Transco Leidy added 47 cents to average $3.65, and the Northeast was home to the week’s greatest loser as well, Dracut tumbled $13.27 to $16.61.

The Midwest was in a league of its own in terms of regional losses dropping $10.23 to average $6.11. The Midcontinent was the next closest region losing $4.52 to $4.72, and the Northeast fell $3.20 to $5.87.

The weekly Rockies average slumped $1.74 to $4.40 and East Texas shed $1.71 to $4.46.

South Texas and South Louisiana fell $1.61 and $1.60 to $4.44 and $4.51, respectively. Regionally California was the most immune to the tide of red ink losing $1.38 to $4.71.

For the week April futures skidded 19.3 cents to $4.425. The 195 Bcf withdrawal reported by the EIA Thursday for the week ending March 10 has traders and analysts looking ahead to estimate whether the industry can recover from such a brutal winter and fill storage. “The problem, as we see it, is that the market is failing to account for the fact that the rapid system-wide destocking has fundamentally altered the outlook for supply/demand balances,” said Teri Viswanath, commodities strategist at BNP Paribas.

“Looking ahead, we expect conditions will remain tight as production gains fall short of exuberant market expectations. Despite the industry’s best efforts to bring additional supplies to market, we believe that it will take more than a single injection season to swing the market back into equilibrium.”

Inventories now stand at 1,001 Bcf and are 958 Bcf less than last year and 858 Bcf below the five-year average. In the East Region 95 Bcf were withdrawn and in the West Region 21 Bcf were pulled. Inventories in the Producing Region fell by 79 Bcf.

EIA’s Short Term Energy Outlook (STEO) projects relatively high gas production growth and moderate demand growth starting in April, which the agency said will allow for a record storage build through October.

“The forecasted April-to-October storage build of nearly 2,500 Bcf would surpass the previous record injection season net inventory build (April-October, 2001) by more than 90 Bcf, to end the injection season at 3,459 Bcf. While the projected storage build for the upcoming injection season would be a record, total Lower 48 end-October inventories in 2014 would still be at their lowest level since 2008. High injections would not fully erase the deficit in storage volumes caused by this winter’s heavy withdrawals,” STEO said.

A Denver producer is also looking for a robust refill season. “If you reduce the storage deficit relative to last year and the five-year averages, prices are going to come down regardless of what the absolute price is. There is at least 30 years of history to prove that.”

Industry consultant Bentek Energy argues that storage refill is not likely to match the 2.5 Tcf injected in 2003 when storage bottomed at 642 Bcf. According to Bentek, that was the lowest level on record. “During that year, the U.S. set its all-time injection record by putting more than 2.5 Tcf into the ground during the summer,” Bentek said. “To reach 2013’s end-of-season total, the U.S. would have to inject more than 2.8 Tcf [93 Bcf weekly] during the summer. But is that possible?

“A look at average weekly injections by EIA region since 1994 suggests that injecting 2.8 Tcf during the summer is unlikely. Assuming a 30-week injection season, the maximum observed injection rate within the U.S. is 85 Bcf/week, while the country has failed to break the 80 Bcf/week mark since setting the record in 2003. Historically, the East has posted average weekly injections as high as 54 Bcf/week, while the West and Producing [regions] have topped out at 10 Bcf/week and 24 Bcf/week, respectively.”

In Friday’s trading gas for weekend and Monday delivery countered the weekly losses somewhat and posted solid gains. East and Northeast locations were expected to see another round of plunging temperatures towards the end of the weekend and into Monday, and New England points led the day’s advance with double-digit dollar gains.

Those gains along with strength along the Atlantic Seaboard were enough to counter weakness in California and the Rockies. At the close of futures trading April had added 4.2 cents to $4.425 and May was up 4.8 cents to $4.403.

Futures traders are biding their time waiting for favorable buying opportunities. “Since we are not viewing the weather factor as a critical item any more, we are attributing the reversal to some weekend short-covering that could easily be followed by some fresh lows early next week,” said Jim Ritterbusch of Ritterbusch and Associates.

“With the approach of the shoulder season, price volatility is likely to remain compressed and option strategies designed to capture premium should be considered. We see the $4.50 level as a point of gravitation going forward and we have laid out expected price parameters between $4.25 and $4.80 in referencing the May contract and looking over the coming five- to six-week time frame.

“At some point, the market will be forced to focus more intently on an exceptionally low season ending supply that still has the potential of slipping below the 900 Bcf mark in our opinion. However, this is a market that should not be chased on the upside as we feel that this week’s chart deterioration will be offering more favorable buying opportunities to beneath [Friday’s] lows [this] week.”

The EIA report of a 195 Bcf withdrawal had traders back at the drawing board trying to determine new support and resistance levels. “$4.50 was the initial support, but that is now resistance since the high on the day is $4.496, and support underneath is going to be $4.35,” said a New York floor trader.

Others saw speculative longs exiting the market. “The 195 Bcf net withdrawal from storage was somewhat less than the consensus expectation, but was still quite bullish compared with the 93 Bcf five-year average for the date,” said Tim Evans of Citi Futures Perspective. “However, the absence of a bullish surprise seems to be enough to allow the flow of speculative long liquidation to continue.”

In Friday’s cash trading a seemingly never-ending series of temperature swings was forecast for the Mid-Atlantic and Washington, DC, area. AccuWeather.com meteorologist Courtney Spamer said, “The temperature roller-coaster ride will continue into St. Patrick’s Day for the Washington, DC, area. After cloudy skies early Saturday, sunshine breaks through in the afternoon as highs reach the lower 60s.”

That all changes and the second half of the weekend, temperatures will be dropping. Despite the sunshine for the first half of the day, temperatures will struggle to reach the mid 40s in the afternoon. “It’s the typical roller-coaster ride of March,” AccuWeather.com meteorologist Dave Dombek said. “March is notorious for huge temperature swings. The District’s normal temperatures this time of year are highs in the middle 50s during the day and lows in the upper 30s at night.”

AccuWeather.com predicted that the high in Toronto Friday of 46 would slide to 36 Saturday before falling further Monday to 23. The normal high in Toronto in mid-March is 45. New York City’s Friday high of 48 was anticipated to rise to 57 Saturday but plunge to 33 Monday. The seasonal high in the Big Apple is 49. In Arlington, VA, the high Friday of 60 was seen rising to 62 on Saturday before free-falling to 33 on Monday. The normal high in Arlington this time of year is 55.

Quotes for the weekend and Monday at the Algonquin Citygates surged $11.32 to $20.09, and gas at Iroquois Waddington jumped $3.92 to $9.44. Deliveries to Tennessee Zone 6 200 L gained $11.39 to $20.38.

The Marcellus and points west were mixed. On Transco Leidy packages for the weekend and Monday fell 30 cents to $3.14, and on Dominion gas was seen at $4.21, up 14 cents. On Tennessee Zone 4 Marcellus gas changed hands at $2.52, down a dime.

Deliveries to Tetco M-3 added 56 cents to $4.95, and parcels bound for New York City on Transco Zone 6 jumped $2.83 to $8.05.

Observers see active repair and maintenance on pipelines and storage facilities, perhaps hampering an active storage refill. “A lot of pipelines, NGPL being one, have had major issues on their side and everybody’s getting down to the [storage] bottom where we have never been before. It seems like we are venturing into parts unknown. We haven’t been this empty since 2003, but we had lower storage capacity back then. There were fewer fields,” said a Houston industry veteran.

“If you took the starting point and the ending point it might be a bigger difference. I think there will be more issues in New York and other parts of the country as weather will affect the pipe underground. When the thaw comes and water starts rushing through town, things are going to start moving. Everybody would like to be error-free, but you can’t control all aspects. These pipes run 24/7, and things do wear out.”

Prices in the Rockies eased. Weekend and Monday gas on CIG was seen at $4.16, down 9 cents, and deliveries to the Cheyenne Hub fell 3 cents to $4.25. At Opal gas changed hands at $4.24, down a penny, and on Northwest Pipeline Wyoming quotes came in at $4.18, down 2 cents.

Forecasters Friday were still calling for a cool temperature regime in the East and Midwest, but they admit to a high degree of variability in the models. “A potential late-winter storm system for the eastern Midwest and Mid-Atlantic early [this] week is leading to some demand gains in the forecast for next week as precipitation on Monday cools high temperatures and lingering snow pack issues could slow the next warm-up toward the middle of next week,” said Matt Rogers, president of Commodity Weather Group, in the firm’s Friday morning report to clients.

“Otherwise, we are still tracking a challenging mixed flow big picture pattern with both colder and warmer pattern influences still mixing things up over much of the U.S. We saw some warmer changes in the Southwest and California in the six-10 day, but even they still cool down later in the six-10 day and during the 11-15. The models continue to go back and forth on the degree of cooling potential in the 11-15 day. The safest cooler-to-colder areas are still the Midwest to Northeast, but even these areas probably see variability.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |