NGI Data | NGI All News Access

Surging Northeast Leads Mixed Weekly Action

On average weekly prices regionally were all over the map, but the national average came in at $3.74, unchanged from a week ago. South Texas saw the week’s biggest losses, dropping a stout 12 cents to $3.61, and the Northeast reveled in the week’s greatest gains, adding 26 cents to $3.66. Of individual market points, Transco Leidy enjoyed the greatest gain, adding $1.13 to $2.84, and two Texas Eastern points suffered the week’s greatest losses, dropping 13 cents at both Texas Eastern S TX ($3.59) and Texas Eastern W LA ($3.60).

South Louisiana was down 8 cents to $3.67 and East Texas fell 7 cents to $3.66, while the Rocky Mountains dropped 3 cents to $3.71 and California dropped 2 cents to average $3.91. Both the Midwest and Midcontinent posted gains of a nickel to $3.94 and $3.77 respectively.

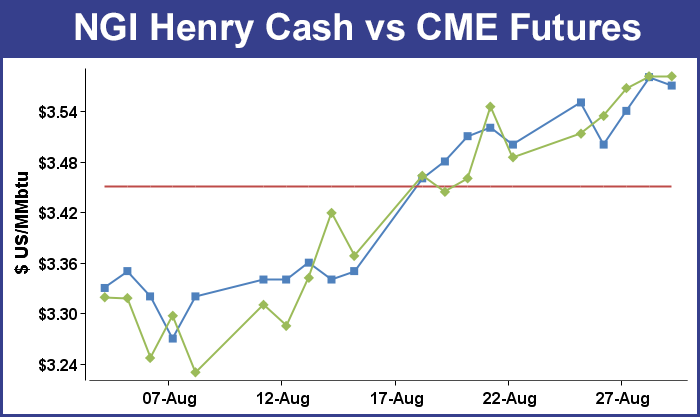

November futures fell 5.7 cents during the week to finish at $3.707.

In Friday’s trading physical natural gas prices overall for weekend and Monday delivery added a penny on average. Prices generally moved within a nickel of unchanged at most points, but Northeast and Eastern Seaboard locations found themselves mostly in the loss column. At the close of futures trading November had added 7.8 cents to $3.707 and December had gained 6.9 cents to $3.812.

Traders see a case for higher winter prices. “There’s been a lot of talk about the diminishing summer-winter time spreads,” said a Chicago-based analyst. “When you look at where the past summer strip [April-October] settled and where the upcoming winter strip [November-March] is trading there is just not a lot of spread there.”

“What I like to do is look back historically and see where the actual summer months settled out. Maybe there wasn’t a spread going into the winter, but did winter prices ultimately rise? There is an outlier where winter prices settled about $4 below the summer on the heels of a very mild winter, but if you take that out of the mix, for 6 out of the last 7 years winter prices have averaged about 46 cents above their preceding summer strip average. November-March over April-October.”

“This past summer strip averaged about $3.79 so if you project that and ask whether there is any likelihood that average holding true, it would argue that the upcoming winter could average in the $4.20s. It certainly isn’t trading that high now. It’s only $3.83 at Friday’s settlement. That suggests that there may be some room for winter prices to move higher,” the analyst said.

Rather than looking at averages, Jim Ritterbusch of Ritterbusch and Associates sees a cold snap necessary if prices are going to rise. “[F]rom here, some renewed cold temperatures will likely be required to lift this market back to above this week’s highs. Imbedded within [Thursday’s] larger than expected supply increase was an uplift in production that we are still viewing as a significant bearish market consideration as this fourth quarter proceeds.”

“Nonetheless, with supply stretched from average levels by only around 2%, any shift back toward a significant or sustainable cold spell next month will still be able to boost values by as much as 7-8% from current levels. So, while our upside price parameter of $4.05 may appear a bit out of reach, it is still achievable some 2-3 weeks down the road should temps cool down again.

Ritterbusch is looking for a place to buy. He feels that “max downside potential exists only to about the $3.60 level as we focus on the December futures contract that will acquire prompt status next Wednesday. We have been advising a $3.60-4.05 trading range in stretching a view out over the next month. But, at the same time, we feel that the low side of these parameters is highly likely to be tested first. We will be looking to approach the long side of December around the $3.60 area.”

Tom Saal, vice president at INTL FC Stone says now may be the time to strike for those with exposure to higher prices. “Hedgers with short side risk: look to buy now for the winter months. [The] trend ain’t your friend.” He also sees buying interest in Cal’14, Cal’16 and Cal’18.

Thursday saw the week’s second dose of storage data within a week. Tuesday’s report for the week ended Oct. 11 showed a build of 77 Bcf, and Thursday’s report was expected to show a slightly higher build. The Energy Information Administration (EIA) reported a build for the week ended Oct. 18 of 87 Bcf, but most analysts were well short of the mark. Tim Evans of Citi Futures Perspective calculated an 80 Bcf increase, and Kyle Cooper of IAF Advisors was looking for a build of 82 Bcf. A Reuters survey of 23 traders and analysts revealed a sample mean of 79 Bcf with a range of 70 Bcf to 87 Bcf. Bentek Energy’s flow model came as close as anyone and predicted a hefty build of 86 Bcf.

Inventories now stand at 3,741 Bcf and are 92 Bcf less than last year’s record-setting build and 77 Bcf above the 5-year average. In the East Region 50 Bcf was injected and in the West Region 4 Bcf was added. Inventories in the Producing Region increased by 33 Bcf.

Weekend temperatures at eastern locations were expected to hover close to seasonal norms. According to AccuWeather.com Friday’s high in Boston of 51 was expected to rise to 58 Saturday before receding to 55 Monday. The normal high in Boston this time of year is 58. Hartford, CT’s Friday high of 52 was seen advancing to 55 Saturday before making it to 56 Monday. The normal high in Hartford is 59. New Haven CT was expected to see a high Friday of 55 before a rise to 56 on Saturday. By Monday the high was predicted to reach 57. The normal high in New Haven for late October is 60.

Forecasters predicted a sunny but cool weekend for New York. “While chilly air and a biting breeze linger in the East, sunshine will nudge temperatures a little by day this weekend around New York City,” said Alex Sosnowski, AccuWeather.com meteorologist. Highs this weekend will be in the middle to upper 50s [and] nighttime lows will be in the mid-30s over the northern and western suburbs and the 40s in Midtown.”

His data shows that “No major storms will affect the region through early next week. However, depending on the track of one or more storms to affect the Rockies, the weather has the potential to get unsettled in the Appalachians and East Coast sometime late next week.”

Monday power prices throughout the region offered little incentive to buy gas for power generation. IntercontinentalExchange reported that power for Monday delivery to the New England Power Pool’s Massachusetts Hub added 46 cents to $42.29/MWh but other New England spots showed declines. Power into the New York Independent System Operator’s Zone A delivery point (western New York) fell $1.84 to $41.16/MWh, and power into Zone G (Eastern New York) slipped $1.16 to $42.98/MWh.

Gas for weekend and Monday delivery at the Algonquin Citygates plunged 31 cents to $4.19 and gas into Iroquois Waddington shed a nickel to $4.04. Gas on Tennessee Zone 6 200 L lost 16 cents to $4.23.

On Dominion gas for weekend and Monday delivery fell 6 cents to $3.50 and packages on Tetco M-3 were off 6 cents as well to $3.71. Gas bound for New York City on Transco Zone 6 added a penny to $3.84.

Major market trading centers were solidly in the black. Gas at the Chicago Citygates rose 3 cents to $3.91 and deliveries to the Henry Hub were up 3 cents to $3.68. Gas at Opal rose 2 cents to $3.68 as well, and packages at PG&E Citygates gained 5 cents to $3.99.

Forecasters are seeing any widespread cold limited to the western US. Commodity Weather Group in its morning 11- to 15-day outlook shows a broad fairway of below normal temperatures from Arizona and New Mexico expanding to Montana and Wisconsin. The remainder of the country, however, is shown as normal.

“[W]e are seeing the models become less and less enthusiastic about intensities for upcoming cool pushes,” said Matt Rogers, president of the firm. “So the 6-10 day has modified to near normal for many areas now partly due to warmer forecast changes and partly to progression of yesterday’s outlook as the coolest weather clumps into the 1-5 day. Despite the warming trends, the modeling still seems to resist developing any sort of major warming. While weakening, the Alaskan ridge does not flip around to a warm-inducing Alaska low. So instead, we just get a mixed pattern with transient, weak warming and cooling events. Risks lean warmer due to the lack of a big cold air connection.”

In Thursday’s trading physical natural gas for Friday delivery overall declined 4 cents as most traders elected to get their deals done prior to the release of often volatility-inducing storage figures. Weakness was widespread, with most points down a few pennies to a nickel. New England points were particularly weak as soft power prices did not encourage strong gas bids. Upper Great Lakes and California were both down about a nickel. The Energy Information Administration (EIA) reported a build of 87 Bcf, and November futures promptly put in the low of the day before staging a modest advance. At the close November was higher by 1.0 cents to $3.629 and December gained 1.0 cents as well to $3.743.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |