Marcellus | E&P | NGI All News Access | Utica Shale

Antero’s Sweet Spot — Appalachia — Big Draw on Opening Day

Antero Resources Inc., which today is an Appalachian Basin-only operator, made a stunning debut Thursday on the New York Stock Exchange, with the share price up 18.2% from the opening of $44.00 to end the day at $52.01. More than 28.4 million shares traded hands, with “AR” the most-traded stock on the day.

The valuation of the company on Thursday was estimated at about $11 billion, based on investor interest.

The initial public offering (IPO) had been launched last week, with book runners setting a price of $38.00-42.00 (see Shale Daily, Oct. 3). However, investors were more interested than the exploration and production (E&P) company had expected. Antero instead opened a day early at $44.00/share.

Antero’s initial $1.5 billion deal value is the largest U.S.-listed E&P IPO since Statoil ASA’s $2.9 billion opening in June 2001, according to Dealogic.

The Denver-based E&P has become a “must-own” name because of its dominance in the Marcellus and Utica shales, said Miller Tabak & Co. analyst Adam Michael. “This is one of the highest-quality E&P companies I’ve seen, as far as the acreage position, in a while,” said Westwood Holdings Group Inc. analyst Bill Costello. “They seem to be right in the sweet spot.”

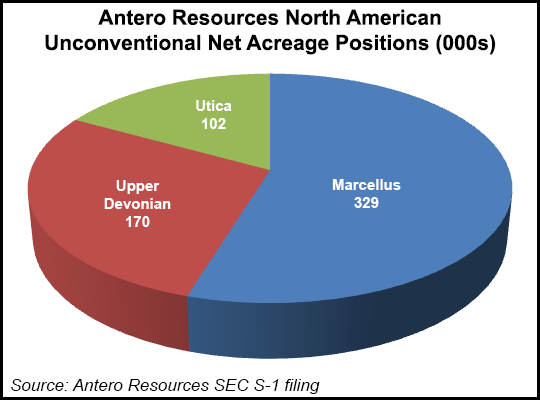

Over the past year Antero has become a pure-play operator in the Appalachia only, with about 329,000 net acres in the Marcellus, 102,000 in the Utica and around 170,000 in the Upper Devonian. It once held considerable assets in the Rockies, as well as the Woodford and Barnett shales, but no more.

With Warburg Pincus LLC’s private equity, Antero was launched in early 2003, helmed by CEO and Chairman Paul Rady and President and CFO Glen Warren Jr. The original company was sold to XTO Energy Inc. in April 2005. (XTO now is the U.S. E&P arm of ExxonMobil Corp.)

Less than two years later, the second Antero was launched, again with Warburg’s backing and again with Rady and Warren at the helm. Rady, a former Barrett Resources executive, had helped to create and then run Pennaco Energy Inc. beginning in 1998 until it was sold three years later to a Marathon Oil Corp. predecessor. Warren had been CFO at Pennaco.

Over the past five years Antero has taken a sharp turn north and east, with Appalachian E&P now its primary focus. Funds to expand the drilling program initially in the Marcellus came by selling off the Arkoma Basin assets, Piceance Basin properties and its midstream operations in Appalachia (see Shale Daily, Nov. 7, 2012; June 5, 2012; Feb. 28, 2012).

Antero now has 15 rigs operating today in West Virginia, with Marcellus output averaging 555 MMcfe/d net. Of the 199 horizontals drilled in the Marcellus, 197 are online. It also is going back into the midstream business by building gathering facilities in West Virginia’s Doddridge and Ritchie counties. It also has several contracts with MarkWest Energy Partners LP and affiliates to process its rich gas.

In the Utica, four rigs are operating and producing on average 85 MMcfe/d net. Eleven horizontal wells in Ohio are online.

This year the Appalachia portfolio has provided a huge increase in year/year production, with net output in 1Q2013 up by 114% (see Shale Daily, May 14). Net production in 2Q2013 rose 115% from a year earlier, and proved reserves by midyear were 47% higher than in the first half of 2012 (see Shale Daily, July 30).

Earlier this year, Antero increased its capital expenditures for this year by $500 million to $2.45 billion, which included $1.45 billion for drilling and well completion. At the end of June Antero had spent about $1.2 billion for exploration and completions. Proved reserves totaled around 6.3 Tcfe at the end of June, a 47% increase from the end of 2012. Net production jumped 115% in 2Q2013 year/year.

Private equity will continue to exert a lot of control over Antero, with Warburg affiliated funds holding more than 38% of the voting interests in Antero Resources Investment LLC, which owns 87% of the producer. Yorktown Partners LLC and Trilantic Capital Partners also own stakes.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |