Forward Look

charting natural gas forward prices at 70+ key North American trading locations

Forward Look

Related services:

NGI's Forward Look delivers robust natural gas forward curve pricing and market coverage.

Why subscribe:

- Daily forward curves expressed as both fixed prices and basis differentials to the Henry Hub

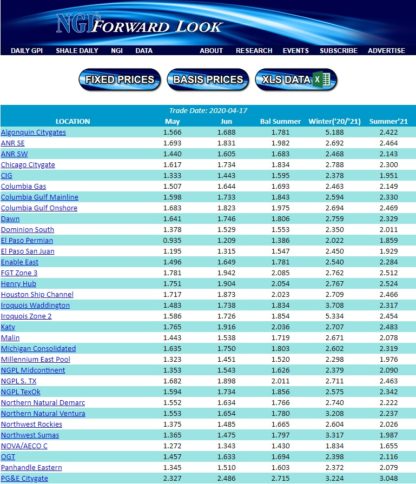

- Forward curves going out 10 years at 70+ key North American trading locations

- Forward curves published as both individual months and seasonal strips

- Regional basis outlooks

- Deep and robust historical data

- Weekly forward markets analysis and insights

- Access to price analysts and exceptional customer service

- Accessible via web and email

- Datafeed file, NGI Data Services API, and via Excel Add-in

- NGI delivery platform partners

- Enterprise subscriptions and corporate trials are available

- Información en español

Who should subscribe:

- Natural gas analysts and traders

- Natural gas buyers and sellers

- Accounting, settlement, compliance and risk professionals

- Investment professionals

- Valuation experts

Sample Download

cloud_download

Sample Download

cloud_download