U.S. Unconventional Sector Said Finally Turning Cash Flow Positive

In what is called a “remarkable turnaround,” the second quarter was the first three-month period on record for Lower 48 explorers overall to achieve positive cash flow from operations after accounting for capital spending.

Energy researcher Rystad Energy studied the financial performance of 40 dedicated U.S. onshore exploration and production (E&P) operators to analyze cash flow from operating activities (CFO). CFO is the cash available to expand the business via capital expenditures (capex), reduce debt or return to shareholders.

During 2Q2019, 35% of the operators in the peer group were found to have balanced spending with CFO, accumulating an estimated $110 million surplus in operating cash flow versus capex.

“That is an industry first,” said senior analyst Alisa Lukash. “The $5 increase in the average West Texas Intermediate oil price from the first quarter to the second quarter of 2019, coupled with operators’ efforts to keep spending within their initial budgets, resulted in a slight surplus of adjusted CFO for total capex.”

Many of the largest E&Ps managed to achieve positive earnings in 2Q2019, although the accumulated profit overall was significantly depressed by Anadarko Petroleum Corp.’s $1 billion merger cancellation fee associated with the scuttled Chevron Corp. merger, Lukash noted. Anadarko now is part of Occidental Petroleum Corp.

The onshore industry has been under increasing pressure from shareholders to balance capex with CFO, while maintaining robust production growth and generating extra cash via stock repurchase and dividend programs.

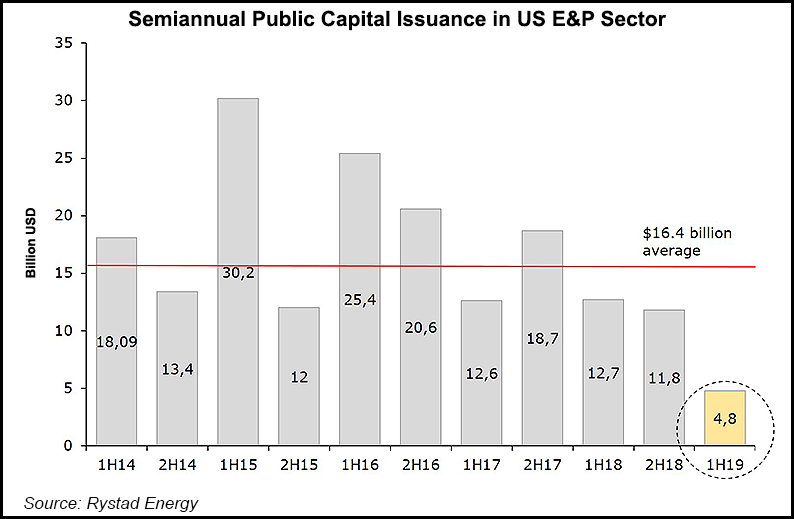

“With negative cash flows, shale companies have historically relied on bond markets to finance their operations,” according to Rystad analysts. “Without additional funding and any debt refinancing, capex would have to be cut.”

In the first half of 2019, U.S. E&Ps raised a record low $4.8 billion, compared to an average semiannual issuance of $16.4 billion since 2014. Rystad said no pure-play Lower 48 operator has made a public offering since Magnolia Oil & Gas Corp. in 2017.

“This leaves the industry with fewer options to boost capital guidance throughout the remainder of 2019, as operators had significantly frontloaded capital budgets this year, leaving 46% of guided capex for the second half of the year,” Lukash said.

The slowdown in spending doesn’t translate directly into eliminating production growth, Rystad noted, as there is a natural gap between budgeting plans, fracturing/completing wells and first oil and gas output.

The top 40 U.S. unconventional E&Ps, which account for nearly half of total domestic shale and tight oil output, have indicated a 3% quarterly increase in their drilling and completion capex as of 2Q2019, and a 7% jump in the number of completed wells over the same period. Horizontal oil completion activity also picked up in the second quarter, analysts noted.

Additional onshore development by many of the largest onshore E&Ps already has “been confirmed for the second half of the year,” Lukash said, so “we do expect robust completion activity to persist in the third quarter, before slowing down in the final quarter of 2019.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |