Bears Seize Natural Gas Momentum on EIA Surprise, Mixed Forecasts

A large bearish miss in the latest government inventory data and forecasts showing underwhelming levels of June cooling demand had natural gas futures bulls in retreat Thursday.

In the spot market, Midcontinent and West Texas prices clawed their way higher as much of the eastern two thirds of the Lower 48 saw modest declines; the NGI Spot Gas National Avg. added 2.0 cents to $2.080/MMBtu.

The Nymex July futures contract settled at $2.547, down 7.7 cents after venturing as low as $2.534. Selling was of a similar magnitude further along the strip. August dropped 7.5 cents to settle at $2.557, while September settled at $2.549, off 7.4 cents.

The bears may have been waiting for the June contract’s expiration Wednesday, as they “quickly pounced right at expiration time and haven’t looked back,” observed NatGasWeather.

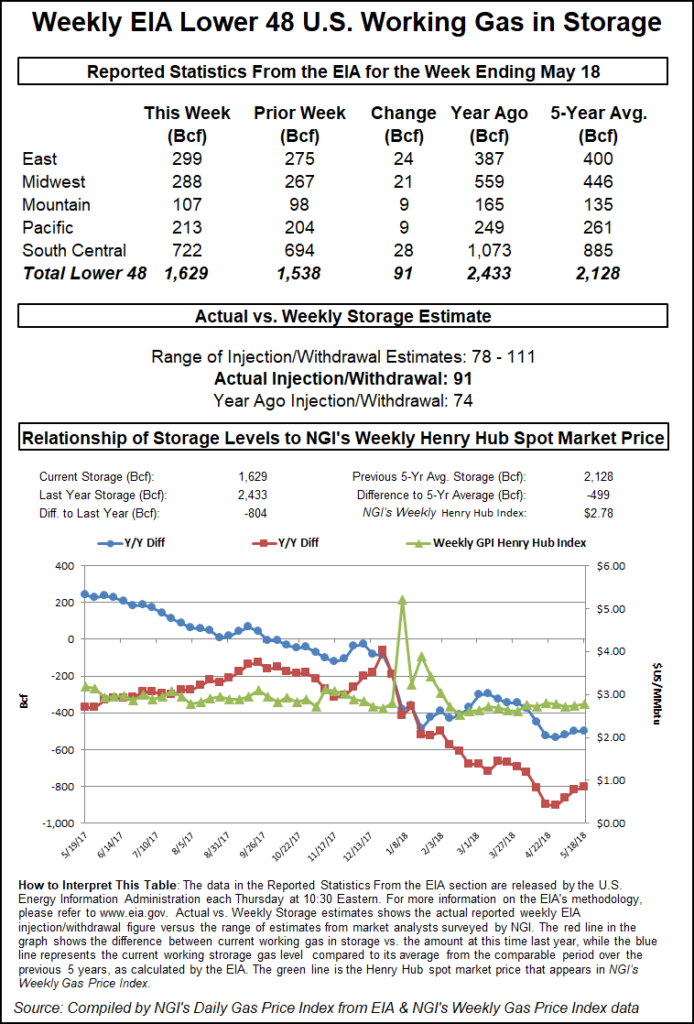

Adding to the bearish momentum that had developed in the market overnight, the Energy Information Administration (EIA) on Thursday reported a much larger-than-expected 114 Bcf injection into U.S. natural gas stocks.

The 114 Bcf build, reported for the week ended May 24, overshot estimates by a wide margin, and the number easily tops both the 95 Bcf build recorded in the year-ago period and the five-year average 97 Bcf injection.

Prior to the EIA report, consensus had formed around a build in the high 90s to low 100s Bcf. A Bloomberg survey had pointed to a median prediction of 98 Bcf, based on estimates ranging from 94 Bcf to 104 Bcf. The 114 Bcf figure topped even the highest estimate submitted to this week’s Reuters survey, which had called for a 101 Bcf injection based on a range from 91 Bcf to 110 Bcf. Intercontinental Exchange EIA Financial Weekly Index futures settled Wednesday at 100 Bcf, while NGI’s model predicted a 98 Bcf build.

During a weekly natural gas storage chat on Enelyst, Het Shah, managing director for the platform, called it “quite the bearish print. Next week is bound to be a mess as well with the long weekend.”

Shah pointed to the Midwest and South Central regions as the areas where estimates missed the mark this week.

“I think it’s the timing of the heat that threw off the number,” Shah wrote. “This late-May heat resembled something we’d see in late June.”

Total Lower 48 working gas in underground storage stood at 1,867 Bcf as of May 24, 156 Bcf (9.1%) higher than year-ago levels but 257 Bcf (minus 12.1%) below the five-year average, according to EIA.

By region, EIA recorded a 35 Bcf build in the Midwest and a 30 Bcf injection in the East. Further west, the Mountain region refilled 4 Bcf for the week, while 12 Bcf was injected in the Pacific.

The South Central region posted a 31 Bcf weekly build, including 27 Bcf injected into nonsalt and 4 Bcf into salt stocks, according to EIA.

As for the latest forecasts Thursday, the midday Global Forecast System added some demand for early next week but was mixed on the outlook for the second week of June, with some days gaining demand and others losing demand, according to NatGasWeather. Overall, national daily cooling degree day totals are on track to come in near to below normal for the next 15 days, the forecaster said.

“Most importantly, the South and Southeast won’t be nearly as hot for the first week of June compared to this week, a primary reason national cooling demand just won’t be strong enough to impress,” NatGasWeather said. “There will still be bouts of stronger cooling demand over the southern U.S. in the weeks ahead, just not sustained.

“The net result is builds will continue to run larger than normal for further improvements in deficits and rapid refilling of storage. Even if there were to be hotter trends, it still might not be enough to override the negative sentiment caused by what was a rather sizable bearish miss” in Thursday’s report, along with more triple-digit injections potentially in the offing.

Perhaps getting a lift from the expected conclusion of maintenance work that’s been limiting northbound flows on the Natural Gas Pipeline Co. of America (NGPL) system, prices strengthened in the Midcontinent and further south in the Permian Basin Thursday.

Coming off record-low negative prices late last week and earlier this week, NGPL Midcontinent rebounded sharply in trading Thursday, adding $1.160 to average $1.170.

To explain the extreme weakness observed in NGPL Midcontinent prices the past few days, Genscape Inc. analyst Matthew McDowell pointed to “inter-basin competition between associated gas volumes from NGPL’s Anadarko basin molecules and NGPL’s Permian receipts fighting for limited space on the pipe.”

The force majeure declared last week at Compressor Station (CS) 194 in Ellsworth County, KS, has cut about 600 MMcf/d of flows bound for Midwest markets via NGPL’s Amarillo Mainline, McDowell said.

“The 1.3 Bcf/d Amarillo Mainline has been the primary source of takeaway capacity from the Permian and Anadarko basins since a pipeline remediation force majeure separated NGPL’s TexOK zone from the Midcontinent zone,” the analyst said. “This reduced east-bound Midcon flow toward the Gulf Coast Mainline to zero since the beginning of April and routed NGPL Midcon production toward the Amarillo Mainline to the west.”

The CS 194 force majeure was expected to conclude by Friday, according to a notice issued earlier in the week by NGPL.

“…There is the possibility of more maintenance-restricted price volatility if the force majeure-prone Amarillo Mainline compressors continue to have issues,” McDowell said.

As for the force majeure separating the Midcontinent and TexOK zones, NGPL said it now expects the restriction to continue through June 5, instead of through Friday as previously stated. The operator cited “extreme weather-related conditions, including severe flooding in the repair area.”

In West Texas, the recent epicenter of negative spot prices in the U.S. market, locations continued to see improvement Thursday following another foray deep into the red coinciding with the NGPL CS 194 disruption. El Paso Permian averaged minus 2.0 cents, up 65.5 cents day/day.

Elsewhere, prices mostly saw discounts throughout the Gulf Coast, Midwest, East Coast and Appalachia Thursday. Benchmark Henry Hub slid 10.0 cents to $2.525.

“Record-breaking heat across the Southeast will ease over the coming days as upper high pressure weakens and shifts toward Texas,” according to NatGasWeather. “Much of the rest of the country will be mostly comfortable with highs of upper 60s to 80s, although still with areas of heavy showers and thunderstorms for local cooling, especially across the northern U.S.”

In Appalachia, Tennessee Zn 4 313 Pool dropped 2.5 cents to $2.250.

Starting Saturday, scheduled remediation work on Tennessee Gas Pipeline (TGP) could restrict 337 MMcf/d of flows out of Northern Pennsylvania, according to Genscape analyst Dominic Eggerman. The work, at CS 307 in Forest County, PA, is scheduled to wrap up June 5.

“This maintenance will restrict westward gas flows out of Northern Pennsylvania on TGP,” Eggerman said. “Some production will have to look for reroutes as eastward flow along the 300 Line is at line capacity. Flows through CS 307 have averaged 1,045 MMcf/d over the past 30 days, and this restriction will reduce operational capacity to 708 MMcf/d.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |