Story of the day

SLB’s Strong International Oil, Natural Gas Business Overcomes Softer North American Activity

Energy Transition

Natural Gas Buyers Gaining AI Edge with Nitty Gritty Carbon Intensity Data

Creating credible, transparent emissions profiles to differentiate natural gas supply has come a long way from the “responsibly sourced” days, as decarbonization as a service, or DaaS, moves beyond a nice-to-have for operators to a must-have to gain customers, according to experts. Natural gas heavies EQT Corp. and Williams have been at the forefront of…

April 23, 2024Energy Transition

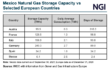

Natural Gas Generation Dominates in PJM as Emissions Fall to Record Lows

PJM Interconnection, the largest U.S. regional transmission organization (RTO), recorded all-time lows for various greenhouse gas emissions last year while natural gas-fired generation continued to grow as the Mid-Atlantic region’s primary power source. PJM, the RTO managing the electric grid for 13 Mid-Atlantic states and Washington, DC, said carbon dioxide (CO2) emissions in 2023 tumbled…

April 23, 2024Markets

May Natural Gas Futures Slightly Lower as Mild Forecast Pressures Prices

With the market continuing to balance near-term oversupply against longer term bullishness, natural gas futures moved slightly lower at the front of the curve in early trading Tuesday. The May Nymex contract was down 1.7 cents to $1.774/MMBtu at around 8:45 a.m. ET. June was off 1.7 cents to $2.048. A recently updated outlook from…

April 23, 2024Markets

Natural Gas Futures Get Boost from Freeport Restart, Cool Weather-Driven Demand

Natural gas futures resumed their climb on Monday, buoyed by a recovery in Gulf Coast LNG feed gas demand above 12 Bcf/d and Lower 48 gas production staying subdued. A jump in Henry Hub cash prices also added support. At A Glance: NGI estimates 86 Bcf injection Freeport restarts LNG exports Production at 98.2 Bcf/d …

April 22, 2024Trending News

Energy Transition

Natural Gas Buyers Gaining AI Edge with Nitty Gritty Carbon Intensity Data

Apr 23, 2024

Energy Transition

Natural Gas Generation Dominates in PJM as Emissions Fall to Record Lows

Apr 23, 2024

Markets

Natural Gas Futures Get Boost from Freeport Restart, Cool Weather-Driven Demand

Apr 22, 2024

Natural Gas Prices