NGI Weekly Gas Price Index | Markets | NGI All News Access | NGI Data

Mild Temps Keep NatGas Bulls from Getting in the Spirit as Weekly Prices Tumble

Milder temperatures prompted widespread selling across the Lower 48 during the week ended Friday (Dec. 21), leaving no doubts about the direction of natural gas spot prices heading into the Christmas holiday break; the NGI Weekly Spot Gas National Avg. dropped 75.5 cents to $3.495/MMBtu.

A prolonged stretch of warmer temperatures leading up to the holidays weakened national demand and helped ease the storage concerns that had driven Henry Hub prices north of $4 earlier in the heating season. For the week, the Louisiana benchmark pulled back 64.5 cents to $3.620.

Prices in the Northeast posted some of the heaviest losses as temperatures along the Interstate 95 corridor climbed into the 50s and 60s late in the week. Algonquin Citygate shed $1.655 to average $4.990 on the week, while further south Transco Zone 6 NY gave up 78.5 cents to $3.715.

Locations out West saw weaker prices as well, with declines of 60-70 cents or more across much of the Rockies and California. Opal tumbled 64.0 cents to $3.880, while the import-constrained SoCal Citygate slid 74.5 cents to $6.200.

Natural gas futures bulls put a bow on another wild week Friday, rallying as forecasts showing a potentially chilly start to the new year provided support The January Nymex futures contract settled 23.3 cents higher at $3.816 Friday after trading as high as $3.829 and as low as $3.595. With plenty of ups and downs along the way, the front month finished the week nearly 20 cents higher after opening Monday at $3.620.

The midday Global Forecast System (GFS) guidance Friday held onto colder trends that showed up in its early morning run, according to NatGasWeather.

“Timing-wise, a mostly mild U.S. pattern is still expected through Dec. 29, then with stronger cooling across the northern and eastern U.S. Dec. 30-Jan. 3 and where it will play out either neutral or slightly bullish depending on just how much cold air arrives across the East. Most of the data sees mild conditions returning across the eastern half of the country Jan. 4-7, but that’s not guaranteed as there’s a way reinforcing cold shots continue,” and recent GFS data had “teased increasing potential for this.”

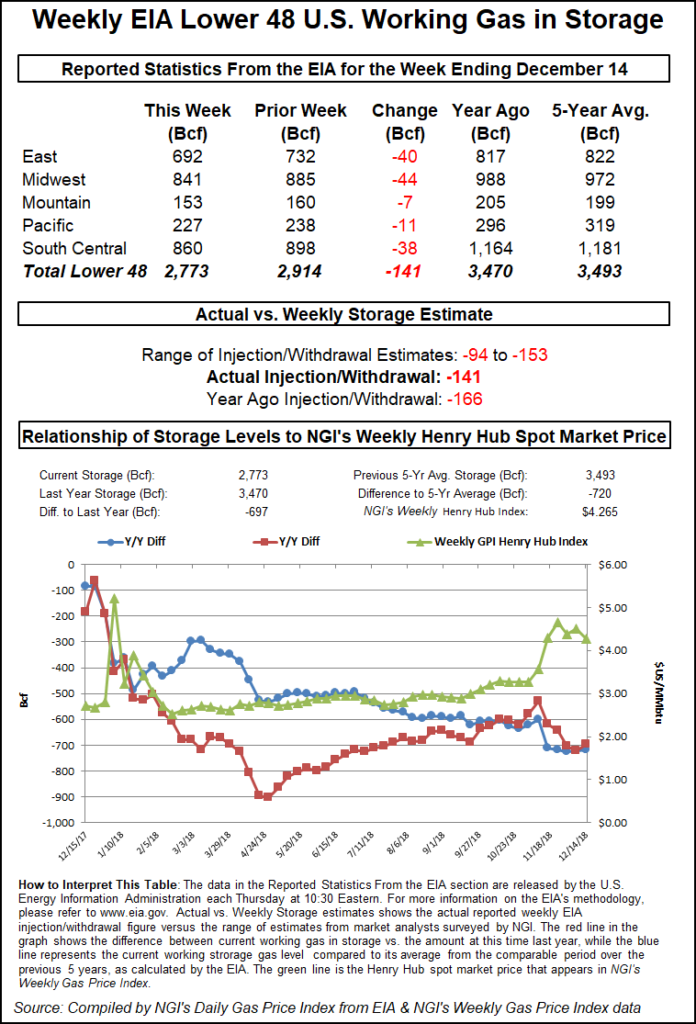

Meanwhile, the Energy Information Administration (EIA) on Thursday reported a 141 Bcf withdrawal from U.S. natural gas stocks, but despite coming in on the higher side of estimates the figure failed to impress a jumpy natural gas futures market.

Nymex futures, trading higher along the winter strip when the report came out, initially gained slightly on the somewhat larger-than-expected withdrawal before dropping below pre-trade levels as a stretch of mild temperatures figures to ease storage concerns heading into the new year.

The 141 Bcf withdrawal for the week ended Dec. 14 compares to a year-ago withdrawal of 166 Bcf and a five-year average pull of 144 Bcf. Prior to Thursday’s report, estimates had been pointing to a withdrawal in the low to mid-130 Bcf range, with responses to major surveys coming in as low as 94 Bcf and as high as 153 Bcf.

As the number crossed trading screens at 10:30 a.m. ET, the January Nymex contract, already up about 6-8 cents from Wednesday’s settle, added another 4 cents or so, trading as high as $3.837 before pulling back into the $3.810-3.820 area.

But bulls couldn’t sustain any momentum on the EIA report, as prices reversed in short order to trade as low as $3.700 less than a half hour later. By 11 a.m. ET, the January contract was trading around $3.775, up about a nickel from the previous settle.

“This week we saw an impressive nonsalt draw in the South Central, though the salt draw was less impressive,” said Bespoke Weather Services, who had been looking for a 133 Bcf withdrawal for Thursday’s report. “This is a tight enough print to indicate that there could be a return of significant storage concerns on any sustained, major cold later in January into February.

“However, we are looking for a far looser print next week that will eat quite a bit into the storage deficit, which seems to be lessening the impact of this tighter print,” Bespoke said. “Overall, we see the impact on the market as neutral; it was not the bearish 133 Bcf withdrawal we saw as possible, but is not so tight as to overwhelm next week.”

Total Lower 48 working gas in underground storage as of Dec. 14 stood at 2,773 Bcf, 697 Bcf (20.1%) below last year’s stocks and 720 Bcf (20.6%) below the five-year average, according to EIA.

By region, the Midwest posted a 44 Bcf withdrawal for the week, while 40 Bcf was withdrawn in the East. The Pacific saw an 11 Bcf pull, with 7 Bcf withdrawn in the Mountain region. In the South Central, 29 Bcf was pulled from nonsalt for the week, while 9 Bcf was pulled from salt stocks, according to EIA.

The 141 Bcf withdrawal implied the market was about 2.3 Bcf/d loose versus the five-year average for the report week when factoring in degree days and normal seasonality, according to Genscape Inc. analyst Margaret Jones.

Tudor, Pickering Holt & Co. analysts said weather-adjusted, “the market was 1.5 Bcf oversupplied (versus the adjusted trailing four-week average of 3.0 Bcf/d oversupplied). Lower production is driving the oversupply pullback, as production in the past two weeks has fallen 1.2 Bcf/d from early December flows, 88.5 Bcf/d.

“Despite Thursday’s production cresting at 88.0 Bcf/d, it remains to be seen if U.S. supply can hold up to heightened winter demand, especially as colder temperature masses migrate to the Northeast. The U.S. natural gas balance continues to be a weather-driven story, despite flashier headlines concerning anemic Mexican exports and untapped liquefied natural gas (LNG) export capacity.”

Analysts with Raymond James & Associates said the 141 Bcf pull “implies that the market was 3.4 Bcf/d looser than last year on a weather-adjusted basis, and it has averaged 4.2 Bcf/d looser over the past four weeks.

“…Longer term, we expect 2019 should prove to be a positive year for natural gas demand as both exports to Mexico and outbound LNG tanker activity ramp up,” the Raymond James analysts said. “On the supply side, more associated gas supply is expected. However, we believe an increasing domestic gas supply and growth in renewables that are increasingly becoming more cost competitive with gas are putting further pressure on Henry Hub gas prices.”

Analysts with Jefferies LLC on Friday said U.S. gas production was showing a 0.3 Bcf/d sequential decline month-to-date for December versus November output.

“If production holds at these levels, it will mark the first supply decline since April,” the Jefferies team said. “Over the past five months, the U.S. has added an average of 1.4 Bcf/d each month. Additionally, Appalachia production spiked in early December to 31.7 Bcf/d and has fallen by around 900 MMcf/d over the past two weeks.

“Natural gas storage currently sits about 21% below average and about 12% below the 10-year low in 2008, a time when total U.S. gas demand was almost 20 Bcf/d lower,” the analysts said. “In November/December, the storage deficit has widened further as demand has been strong and LNG flows have continued to increase. In a normal weather scenario for January/February, we find it increasingly difficult to envisage storage volumes normalizing this winter, leaving us headed into the summer well below average with a ramp in LNG exports on the horizon.”

Still, according to Genscape’s daily pipe production estimates, Lower 48 output was showing signs of rebounding heading into the holiday weekend. As of Thursday and Friday, production had topped the 86 Bcf/d mark for the first time in 10 days, according to the firm’s senior natural gas analyst Rick Margolin.

“Production this month-to-date is averaging 85.93 Bcf/d, but had been slipping in the past two weeks on a smorgasbord of maintenance events, falling as low as 84.39 Bcf/d on Dec. 14,” Margolin said. “Since that time, however, every basin we track has posted increased output, with the largest gains coming out of the Northeast (up 562 MMcf/d since Dec. 14), the Gulf Coast (up 539 MMcf/d), Texas (up 305 MMcf/d) and the Rockies (up 253 MMcf/d).”

Spot Slides Ahead Of Christmas Break

Physical markets weakened across most of the Lower 48 Friday as buyers showed limited interest in deals for delivery over the Christmas holiday weekend. Benchmark Henry Hub tumbled 16.5 cents to $3.530. Locations throughout the Midwest, Midcontinent, Texas and Southeast posted similar declines of around 15-25 cents.

Points in the Northeast and Appalachia bucked the broader downtrend, with Algonquin Citygate surging 93.5 cents to average $4.575, while Texas Eastern M-3, Delivery added 10.5 cents to $3.335.

A strong weather system was expected to move up the East Coast Friday and into Saturday, bringing “mostly rain but with some snow into the coldest air on the back side of the system, just not widespread,” according to NatGasWeather.

“The rest of the country will be mild with above normal temperatures, aiding lighter than normal national demand,” the forecaster said. “There’s still expected to be a modest cold shot sweeping across the Great Lakes and Northeast Christmas Eve/Christmas, but not cold or widespread enough to increase national demand above normal. Colder systems are expected into the West” for the upcoming week, “although at the consequence of mild high pressure strengthening over the eastern U.S. Dec. 26-29 to keep lighter than normal national demand going.”

Prices in constrained West Texas came under more intense downward pressure than the rest of the country, coinciding with reports of maintenance-related restrictions on flows out of the region. El Paso Permian tumbled 49.0 cents to $1.585, while Waha shed 52.5 cents to average $1.240.

NGPL earlier this month said it would be restricting flows through Compressor Station 168 in Bailey County, TX, another in a series of forces majeure declared by the operator, according to Genscape analyst Matthew McDowell.

“Prior mechanical and horsepower issues beginning in September and continuing sporadically through the months have limited flow from NGPL’s Permian Zone to the Amarillo Mainline. The most recent event, lasting a full month, saw flows through the station fill the restricted operational capacity of 282 MMcf/d for the duration of the event,” McDowell said.

“Compressor Station 168 was upgraded from an operational capacity of 268 MMcf/d to 365 MMcf/d in early August this year. For all times that the station has not been directly impacted by maintenance, flows have averaged only 311 MMcf/d…compared to the maintenance restricted operational capacity of 282 MMcf/d. It is unlikely that similar events at Compressor Station 168 will prove to be significant constraints for NGPL’s Permian Zone.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |