NGI Mexico GPI | Markets | NGI All News Access

Bearish EIA Storage Miss Fails to Shake Up Natural Gas Futures; Gains for West Texas Cash

The natural gas futures market shrugged off bearish government storage data Thursday, with the front month managing to hold on to the lion’s share of gains from a furious rally during the previous session. In the spot market, East Coast points moderated as a number of locations in the Rockies and California continued to trade at elevated prices; the NGI Spot Gas National Avg. climbed 6.5 cents to $4.530/MMBtu.

January Nymex futures settled at $4.646, down 5.3 cents on the day after rallying 40.7 cents during Wednesday’s session. The February contract settled at $4.482, down 5.6 cents, while March slid 6.3 cents to settle at $4.156.

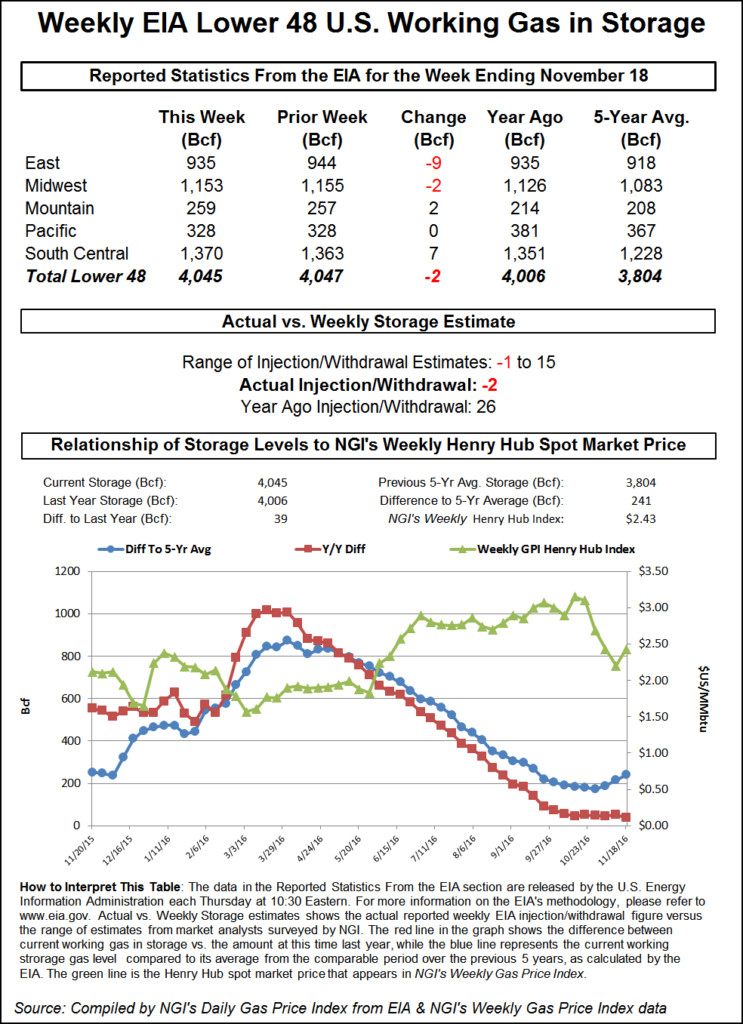

The Energy Information Administration (EIA) reported a 59 Bcf withdrawal from U.S. natural gas stocks that missed well to the bearish side of expectations.

The 59 Bcf withdrawal for the week ended Nov. 23 compares to a year-ago pull of 35 Bcf and a five-year average withdrawal of 49 Bcf. While larger than average for the period, the 59 Bcf pull came in well below estimates that had clustered in the upper 60s to mid 80s range, potentially signaling a greater-than-expected impact on demand from last week’s Thanksgiving holiday.

The looser-than-expected withdrawal also counters last week’s bullish 134 Bcf pull, which topped most estimates by a similarly large margin.

January natural gas futures were already trading lower Thursday morning in the lead-up to EIA’s report, giving back some of the gains posted during Wednesday’s December expiry. When the final number crossed traders’ screens at 10:30 a.m. ET, the January contract quickly dropped a little over 10.0 cents, going from $4.560 down to as low as $4.453. But by 11 a.m. ET, the front month had recovered to trade around $4.522, down a few pennies from the pre-report trading.

“This helps cancel out some of the massive draw the prior week, and we see much of this as being weekly EIA noise in a market that is seeing wild demand, weather and price gyrations,” Bespoke Weather Services said. “This far looser print can be rather easily discounted due to the Thanksgiving impact that we saw as very significant, though it still reflects that we need to keep” heating degree days “near record levels to maximize nonlinear weather demand.

“Later in winter this will become easier, and this print certainly does not erase storage concerns. However, it indicates that on average weather prices can fall back very quickly with current balances, increasing downside back towards the $4 level should we see a week or two of mild weather in mid-December, as seems fairly likely still.”

Total Lower 48 working gas in underground storage stood at 3,054 Bcf as of Nov. 23, according to EIA, down 644 Bcf (17.4%) from a year-ago and 720 Bcf (19.1%) below the five-year average.

By region, the East posted the largest withdrawal for the week at 25 Bcf, followed by a 21 Bcf pull recorded in the Midwest. The Pacific withdrew 4 Bcf, while the Mountain region withdrew 3 Bcf on the week. In the South Central, 5 Bcf was withdrawn, with a 14 Bcf pull from nonsalt offsetting an 8 Bcf injection into salt stocks, according to EIA.

Thursday’s bearish report “didn’t seem to bring the bears out of hibernation,” noted Societe Generale analyst Breanne Dougherty, who said Thursday’s declines did “barely anything” to offset Wednesday’s rally.

“We expect prices to average $3.50-3.75 over the next couple of months, but the front of the curve is very much exposed to sustained upside volatility…We remain bearish to the curve, but over the next eight weeks we do see more upside than downside risk to our current price view.”

As for the latest weather data Thursday, NatGasWeather said the models provided “mixed messages” as the Global Forecast System (GFS) trended milder and the European model trended colder.

“The latest midday GFS was slightly milder for the middle of next week, but flipped back colder Dec. 8-12, seeing a stronger cold shot across the Great Lakes and East,” the forecaster said. “…There’s no change to the timing with a milder break Friday through the weekend for much of the U.S. besides the West, followed by strong cold shots next week into the following weekend.

“…Mild high pressure is still expected to gain in coverage and strength Dec. 12-14 in all datasets, but with uncertainty over how long it will ultimately last,” a likely point of focus for markets heading into the weekend, NatGasWeather said. “We expect colder air will try to make an attempt to weaken the ridge around Dec. 16-17, but that’s quite far out and with more to prove.”

Meanwhile, dry gas production has increased to 85.0 Bcf/d month-to-date in November, up about 1.0 Bcf/d sequentially and up 8.3 Bcf/d year/year (y/y), according to analysts with Jefferies LLC, who added that production reached a new daily high of more than 86 Bcf/d for the first time over the past week.

“Supply growth continues to be driven by Appalachia (up 630 MMcf/d sequentially) and the Haynesville Shale (up 230 MMcf/d), while the Permian was roughly flat versus October,” the Jefferies analysts said. “Haynesville production of 10.8 Bcf/d in November marks a new monthly high for the play, just ahead of the prior peak of 10.7 Bcf/d in November 2011. Our recent conversations with a private Haynesville operator indicated that growth out of the basin was likely to continue into 2019 as numerous private equity-backed entities continue to invest in the basin.”

Demand growth for November has also been strong, according to the Jefferies team, with demand up 11.3 Bcf/d y/y, driven by colder weather and strong power burns despite the spike in gas prices. Demand from liquefied natural gas reached a new high in November, up 1.3 Bcf/d y/y, and industrial demand increased 1.4 Bcf/d y/y, according to the firm.

Elevated Prices in the West

Points throughout the Rockies and California continued to trade at an elevated basis in the day-ahead market Thursday amid forecasts for wintry precipitation across those regions, as well as ongoing constraints on imports from Western Canada into the Pacific Northwest.

As the Oct. 9 explosion on Enbridge Inc.’s Westcoast system continues to hinder southbound flows through British Columbia into Washington state, Northwest Sumas prices tacked on another 86.0 cents to average $17.915. Other Rockies locations strengthened as well, with a number of points trading above $6. Opal added 10.5 cents to $6.220.

In California, Malin picked up 15.5 cents to average $6.215.

“A wet, active pattern is expected to continue through the weekend for the Western U.S., particularly in California and also areas downstream across the Rockies,” the National Weather Service (NWS) said Thursday. “A vigorous upper low and associated frontal system is currently bringing heavy rainfall with embedded thunderstorms across California, along with heavy snow over the higher terrain of the Sierra Nevada.”

That was expected to continue through Thursday night with lighter precipitation across the Pacific Northwest, according to the forecaster.

“However, as the aforementioned upper low and front move farther inland going through Friday, precipitation will increase across the Great Basin and also the central Rockies while still persisting across central and Southern California,” the NWS said. Another system is then expected to arrive across the Pacific Northwest, bringing “another round of heavier precipitation to especially southwest Oregon and northern California Friday night and Saturday.

“A new round of heavy snowfall is expected over the Sierra Nevada and also portions of the Cascades. In fact, multi-day snowfall totals through Saturday are expected to be in excess of 2 feet locally.”

In Southern California, SoCal Citygate shed 33.0 cents to $7.005.

A force majeure event on the Mojave system briefly cut flows from Arizona into California this week, according to Genscape Inc. analyst Joe Bernardi.

“Mechanical failures of Compressor Units 1 and 2 at the Topock Compressor Station reduced operational capacity at the ”MOJTHRU’ meter to 191 MMcf/d for only several cycles,” Bernardi said. “This reduction was in place from the Intraday 1 cycle for Wednesday (Nov. 28) through the Timely cycle for Thursday (Nov. 29).

“The past 30-day average flow was 381 MMcf/d, but this has been the second unplanned maintenance affecting these flows in the past week.” On Nov. 21 another force majeure was declared due to mechanical issues affecting only the Compressor Unit 1, with that event ending with the Timely cycle for Tuesday (Nov. 27), according to Bernardi.

After posting handful of negative trades earlier in the week, averages at a number of West Texas points increased Thursday, though prices in the region generally traded well below Henry Hub. Waha added 13.5 cents to average just 59.0 cents on the day, while El Paso Permian climbed 40.5 cents to average 93.5 cents.

In the Northeast, prices pulled back as more moderate temperatures are forecast to move in over the weekend. Algonquin Citygate fell 65.0 cents to $5.330.

A mild ridge bringing highs in the 50s to 70s across the central and southern United States Thursday was expected to “expand to include the Great Lakes, Ohio Valley and East this weekend where highs will warm into the 50s and 60s while remaining comfortable with 70s and 80s across the southern U.S. for much lighter national demand,” NatGasWeather said.

“Early next week, frigid air will pour across the West and Plains, then spreading into the southern and eastern U.S. Tuesday and Wednesday with widespread lows of -10s to 20s across the northern two thirds of the country, with freezes again into Texas and the South.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2577-9966 |