Natural Gas Futures Steady as Forecasts Mixed; Northwest Sumas Spikes Further

Natural gas futures couldn’t build momentum in either direction Wednesday as forecasts offered mixed signals on what comes next once the season’s first stretch of winter heating demand arrives this week. In the spot market, prices in the Midwest and East remained strong with cold temperatures in the forecast, while higher heating demand wreaked havoc given constraints in the Pacific Northwest; the NGI Spot Gas National Avg. gained 5.5 cents to $3.380/MMBtu.

December Nymex futures traded as high as $3.560 and as low as $3.486 before settling at $3.555, unchanged day/day. January shed 1.4 cents to $3.569, while February eased 0.8 cents to $3.428.

As the market tries to get a read on what will follow the cold pattern forecast for this week and next, all weather models trended colder for the Nov. 17-22 period Wednesday save for the European model, according to NatGasWeather. The Global Forecast System (GFS) remained the coldest in showing wintry temperatures lingering in the Great Lakes and East.

“The European model continues to see a milder pattern setting up across most of the country Nov. 17-22,” the forecaster said. “This makes the overnight data very important to see if the GFS backs off…to better match the European model or if the European model trends colder to fall better in line with the already quite cold GFS.”

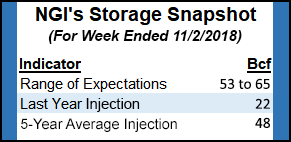

With the market left to wait another two weeks to get a good handle on how the season’s first blast of winter cold will impact balances, estimates for this week’s Energy Information Administration (EIA) storage report have been pointing to a somewhat larger-than-average build.

A Reuters survey of 18 market participants showed respondents anticipating a 58 Bcf build into U.S. gas stocks for the week ended Nov. 2, with predictions ranging from 53 Bcf to 65 Bcf. A Bloomberg survey produced a median build of 59 Bcf, with a range of 53 Bcf to 65 Bcf. Intercontinental Exchange EIA financial weekly index futures settled Tuesday at 61 Bcf.

Last year, EIA recorded a 22 Bcf build for the period, and the five-year average is an injection of 48 Bcf.

The greater intensity now forecast for the upcoming cold pattern has made any further recovery for low storage inventories unlikely and defies previous expectations that winter might arrive late this year, noted Morningstar analyst Dan Grunwald.

“The power grid’s increasing reliance on natural gas is worth reiterating and explains a large part of how the market finds itself in such short supply today,” Grunwald said, pointing to not only natural gas-fired capacity additions and coal retirements but also to changes in usage patterns. “…As natural gas capacity has shifted over the past few years demand has increased more rapidly than expected. That’s because new capacity has gravitated away from the old peaking plant model toward taking over the intermediate portion of the stack. The result is an increase in both running time and usage.”

This comes as the western Pacific has caused weather models to “whip back and forth,” putting a wide range of outcomes in play for storage by the end of the withdrawal season and leading to the risk premiums evident in recent pricing.

“Weather continues to drive volatility in the natural gas market. With generation demand sensitive to nuclear outages and encroaching ever deeper into the baseload stack, we expect a drop in power burn, starting with this week’s storage number, as the nukes return from maintenance,” Grunwald said. “A decent injection this week could see prices retreating again. Such a reversal is even more likely if models revert to showing a bit more warmth in coming weeks.

“Longer term, winter weather models continue to frustrate,” the analyst said. “This year’s market has been banking on a moderate winter, but that scenario has become less likely. As models still don’t want to provide clear direction it is unlikely that prices will provide a sizable retreat at this point, but they should see a small to moderate correction after this week’s overreaction.”

Analysts with Barclays Research on Wednesday said they have revised higher their natural gas price forecast for the fourth quarter from $2.95 to $3.15 based on a colder weather scenario for November. Now expecting a further reduction in storage inventories, the analysts said they’re raising their 2019 forecast by 8 cents to $2.80.

Still, the Barclays team said it’s holding to its bearish thesis despite the recent bullish market sentiment as record production looks to remain strong enough to “keep a lid on prices this winter, if temperatures are close to normal.”

The analysts advised clients to “beware the weather-driven risk premium in natural gas markets, as the price support it yields can disappear just as quickly as it emerged. Weather forecasts can be quite unpredictable, and, in our view, once these transient factors revert toward more normal levels, rising prices are likely to curb gas burns.”

Northeast Climbs, Northwest Sumas Spikes

In the spot market, with cold weather pushing into the Lower 48 Midwest prices held steady after big gains earlier in the week, while points across the Northeast and Appalachia continued to strengthen.

Chicago Citygate averaged $3.680, down 3.0 cents on the day, while Transco Zone 6 NY gained 18.0 cents to $3.545.

Colder than normal temperatures were expected to pour out of southern Canada and into the Plains Wednesday before spreading across the Great Lakes and east-central United States Thursday and Friday, NatGasWeather said.

“With lows behind the cold front dropping into the teens to 30s, locally single digits near the Canadian border, national demand will quickly ramp up,” the forecaster said. “Colder air will finally push through the East this weekend, leading to further increases in national demand.”

With the first major cold system of the winter already descending into the northern tier of the Lower 48 Wednesday, heating demand was on the rise, according to Genscape Inc. After pushing demand higher in Alberta, “the cold is now extending southward into the pipeline-constrained Pacific Northwest,” senior natural gas analyst Rick Margolin said. “Demand in the region is at 2.1 Bcf/d and should continue climbing to a high near the 2.4 Bcf/d mark early next week.”

Speaking of the Pacific Northwest, prices at Northwest Sumas continued to blow the roof off Wednesday with cold temperatures compounding constrained conditions following last month’s pipeline rupture on Enbridge Inc.’s Westcoast Transmission system.

Northwest Sumas surged $8.425 to average $18.095 Wednesday, including trades as high as $30. Meanwhile, north of the Canadian border, Westcoast Station 2 prices remained on the negative side of the ledger, inching higher to minus $C1.170.

Genscape reported Tuesday that Westcoast continues to show restrictions on downstream flow capacity through its Huntingdon delivery area. Westcoast declared a new system-wide operational flow order (OFO) Wednesday, updating a previous OFO, lowering pack tolerance requirements for shippers from 2-3% to 0%.

Back in the Midwest, the region is expected to see heating degree days (HDD) continue climbing to a peak of around 36 HDDs by Saturday, 14 more than normal for this time of year, according to Genscape.

“Another cold blast is forecast for early next week,” Margolin said. “Forecast temperatures across that region are expected to remain 7-15 HDDs colder than normal through next Thursday. We have demand in the area increasing from 10.8 Bcf/d Wednesday to a high of 11.2 Bcf/d by the start of next week.”

The risk appears low for potential freeze-offs amid the upcoming cold, according to Margolin. While the Permian Basin producing region is expected to see colder temperatures, it’s not expected to be cold enough to trigger freeze-offs.

Last year’s first freeze-off arrived close to New Year’s Day, “when low temperatures sank into single digits and daytime highs remained below freezing just a day after a high of 70 degrees,” Margolin said. “The event lasted roughly four days and took out about 6 Bcf of production.”

Prices were mixed in West Texas Wednesday as points throughout the region continue to trade at a wide negative differential to benchmark Henry Hub. Waha finished near even at $1.185.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |