Shale Daily | E&P | NGI All News Access | NGI The Weekly Gas Market Report

Encana Stacking Up Opportunities in $7.7B Newfield Combination

Encana Corp. has clinched a deal to buy Oklahoma stalwart Newfield Exploration Co. in a stock trade worth an estimated $5.5 billion, as well as assuming $2.2 billion net debt, expanding its four core exploration areas of North America’s onshore to a solid five.

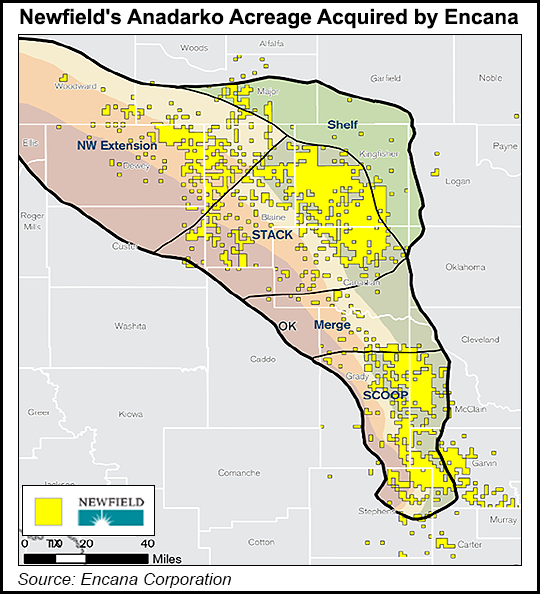

Calgary-based Encana said the deal, announced early Thursday, would add myriad opportunities across Newfield’s 360,000 net acres in two deep regions of the Anadarko Basin better known by their acronyms, the STACK and SCOOP, i.e. the Sooner Trend of the Anadarko Basin, mostly in Canadian and Kingfisher counties, and the South Central Oklahoma Oil Province.

“This strategic combination advances our strategy and is immediately accretive to our five-year plan,” Encana CEO Doug Suttles said. “Our track record of consistent execution gives us confidence to accelerate and increase shareholder returns…When combined with our cube development model, expected synergies and relentless focus on efficiency, we are positioned to deliver highly efficient growth and quality returns.”

Encana in the past few years has streamlined its efforts to focus on only four areas of Texas and Canada, what it has called the “core four,” within the Permian Basin and Eagle Ford Shale of Texas, and Canada’s Montney and Duvernay formations.

With Newfield, Encana expects oil and condensate production to increase by more than 54%, with proved reserves climbing by around 85%. Newfield’s Oklahoma portfolio also contains more than 6,000 gross risked well locations and about 3 billion boe net of unrisked resources. In addition to the SCOOP/STACK, Newfield has holdings in the Arkoma Basin of Oklahoma, Williston Basin of North Dakota, Uinta Basin of Utah and assets offshore China.

The merger would create North America’s second largest unconventional resources producer, with pro forma 3Q2018 production of 577,000 boe/d, including liquids output of around 300,000 b/d, according to Encana.

“This transaction is the best path forward for our company,” Newfield CEO Lee K. Boothby said. “The combination of the two companies provides our investors with the very attributes that should be differentiated in today’s energy sector — operational scale, proven execution in development of large, liquids-rich onshore resource plays, a peer-leading cost structure and an exceptionally strong balance sheet…

“Throughout our 30-year history, Newfield has worked to create a strong portfolio of assets managed by some of the best and brightest people in the business. The merger will accelerate the development of these assets and as a result, capture full value for our owners.”

Encana estimated annual synergies of $250 million through bigger scale, cube development and overhead savings.

Newfield shareholders would trade each share for 2.6719 Encana common shares, which implies that Encana is paying a 35% premium for Newfield, based on closing stock prices Tuesday.

The deal is expected to be completed by the end of March. Encana shareholders would own about 63.5% of the combined company, with Newfield owning 36.5%. Two Newfield directors also would join the Encana board.

Once completed, Encana plans to raise the dividend by 25% and expand share buybacks to $1.5 billion, funded with free cash flow and cash on hand.

“The Encana-Newfield merger marks another significant transaction in the upstream space, but in our view only represents the tip of the merger and acquisition iceberg that will emerge in 2019,” Tudor, Pickering, Holt & Co. (TPH) analysts said. “Our thesis on this topic is fundamentally grounded in the view that shale has matured and as such companies will look to industry consolidation to gain scalable cost synergies and inventory. All of this is a healthy (and necessary) evolution in the upstream space.”

Analysts said they could “easily think of more than 10 additional deals where there should be a strategic asset rationale or cost synergies that would make sense heading into 2019,” representing more than $38 billion in market cap.

“Newfield is a particularly interesting transaction as the name was trading almost on top of current estimated proved, developed producing (PDP) valuation…From an asset consolidation perspective, the Permian will likely be a hotbed of activity next year,” the TPH team said. “Buckle up, as the upstream merger train has left the station and next year will likely be a wild ride.”

Williams Capital Group LP analyst Gabriele Sorbara estimated the deal is worth $11.26/boe of proved reserves, $37,869/flowing boe/d of production and $7,225/undeveloped acre in the STACK/SCOOP.

Wood Mackenzie senior analyst Roy Martin, who handles corporate upstream, said Encana has made “its boldest move yet,” with the Newfield deal.

“Encana has a long track record of ambitious acquisitions, but the Newfield purchase tops its $7.1 billion Permian purchase of Athlon Energy Inc. in 2014. It also makes Encana one of the top five unconventional producers in North America.”

Under Encana’s “back to winning” strategy that it launched in 2013, the company has been moving away from natural gas and realigning its portfolio toward liquids.

“More than $17 billion in acquisitions, in the Eagle Ford, Permian and now the Midcontinent, have been matched with $11 billion in noncore asset sales since launching this strategy.

“The results have been transformative,” Martin said.

Acquiring one of the Anadarko Basin’s top operators “marks an opportunistic purchase for Encana. It will benefit from acquiring an undervalued company, even based on our conservative modelling view. Encana can also afford it…

“There are significant benefits from becoming a larger North American player with multi-basin exposure,” Martin added. “Against the backdrop of Permian headwinds such as takeaway capacity constraints, cost inflation and geological risks related to parent/child wells, the Midcontinent complements the Eagle Ford as an attractive alternative investment option.”

Encana on Thursday also issued its third quarter results, reporting production across the North American onshore was up 33% from a year ago to 378,300 boe/d. Natural gas volumes climbed 27% to 1.197 Bcf/d, and oil output also increased 27% to 95,500 b/d. Natural gas liquids plant condensate was up 47% to 41,000 b/d, while other liquids output was 73% higher at 42,200 b/d.

Net earnings for 3Q2018 totaled $39 million (4 cents/share), down from year-ago profits of $294 million (30 cents), in part on $241 million in derivatives losses. Total operating expenses were higher from a year ago at $1.14 billion from $865 million, with operating income reversing a year-ago loss to $119 million from minus $4 million. Revenue increased year/year to $1.26 billion from $861 million.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1266 | ISSN © 2158-8023 |