$3 Prompt Month Natural Gas Nice While It Lasted; Futures Reverse as Forecasts Seen Milder

Milder forecasts and the prospect of larger storage injections in the coming weeks helped sink natural gas futures ahead of the October contract’s expiration Wednesday, as a sustained rally going back to last week found a top — at least in the near-term. Spot prices were mixed as a few Appalachian points rebounded following recent declines; the NGI National Spot Gas Average finished flat at $2.74/MMBtu.

The October Nymex futures contract rolled off the board at $3.021 Wednesday, down 6.1 cents after trading as low as $2.981. The more heavily traded November contract gave up 7.8 cents to settle below the $3 mark at $2.980. Further along the strip, January dropped 6.4 cents to $3.145.

Bespoke Weather Services pointed to indications of looser supply/demand balance and afternoon guidance that continued recent warmer long-range trends as key factors driving the selling observed on the October contract throughout the afternoon Wednesday.

“These warmer long-range forecasts have fit our October expectations almost perfectly; any cold looks to be fleeting and focused across the Midwest, with ridging likely to dominate across the East and keep heating demand slightly below average for the month,” the firm said. “Meanwhile, we continue to see production near record highs, and power burns have loosened markedly this week even as nuclear outages have not come down much.”

If weather patterns through the first half of October produce below-average gas-weighted degree days, “we would expect to accordingly see larger storage builds that would unwind a significant amount of the narrowing at the front of the natural gas curve in the last few weeks,” Bespoke added. “Of course, that will not come overnight, and we do note some lingering demand side tightness as well as firm cash prices.”

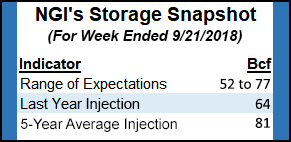

Estimates ahead of Thursday’s Energy Information Administration (EIA) storage report showed the market looking for an injection well below the five-year average, an expectation that likely factored into the sustained price gains going back to last week.

A Bloomberg survey of traders and analysts produced a range of 52-77 Bcf, with the median prediction for a net build of 61 Bcf for the week ended Sept. 21. That compares to a five-year average build of 81 Bcf and a 64 Bcf build recorded a year ago. Kyle Cooper of IAF Advisors called for a 52 Bcf injection, while Intercontinental Exchange EIA financial weekly index futures settled Wednesday at an injection of 54 Bcf.

Last week, EIA reported an 86 Bcf injection into working U.S. natural gas stocks for the week ended Sept. 14, putting stockpiles at roughly an 18% deficit to the five-year average.

Recent growth in power demand for natural gas in the summers, which has helped keep storage deficits from shrinking even as production has depressed prices, is likely to place more burden on the shoulder seasons to refill inventories moving forward, according to Morningstar Commodities Research analyst Dan Grunwald.

“While this year has so far seen near-month contracts struggle to break above the $3 ceiling, historically low storage levels are finally taking their toll as we get closer to winter,” Grunwald said. “This phenomenon is likely to be short-lived since there has been some willingness to postpone injections until now given a low summer/winter spread and higher summer demand. As a result, we should see prices drop off again this fall until winter demand shows up.

“…Longer term, we see a clear signal that production is growing and should be able to meet demand,” the analyst said. “If reserve numbers hold, natural gas production will keep prices low and the forward curve backwardated for years out for the time being. Demand, though, still has plenty to say in near- and short-term price volatility…Winter demand is not going anywhere, but summer demand looks to be a growing trend” that could limit the opportunity to refill storage primarily to the spring and fall as higher cooling demand flattens summer/winter spreads.

Turning to the spot market, prices fell across a number of East Coast points as forecasts called for warm temperatures in the region to moderate by Thursday. Radiant Solutions was calling for Boston, New York and Washington, DC, to see highs in the low 70s Thursday, well off of highs in the 80s Wednesday.

Genscape Inc. demand estimates showed demand in Appalachia (including New York and New Jersey) dropping from 9.68 Bcf/d Wednesday to just above 6 Bcf/d Thursday and Friday. Southeast and Mid-Atlantic demand was expected to drop from 17.67 Bcf/d Wednesday to a little under 13 Bcf/d by Thursday, according to the firm.

The National Weather Service (NWS) was calling for “widespread showers and thunderstorms” to coincide with a cold front moving into the eastern United States Wednesday.

“The southern portion of this boundary is forecast to stall from the Mid-Atlantic to the central Gulf Coast, which should keep showers and storms in the forecast for Thursday too across this region. Heavy to possibly excessive rainfall is possible, especially from the Tennessee Valley to the southern Appalachians,” the NWS said.

Transco Zone 6 New York shed 17 cents to $2.85, while Transco Zone 5 gave up 5 cents to $3.14. Further upstream in Appalachia, Dominion South recovered 9 cents to average $2.16 Wednesday after dropping 16 cents in trading Tuesday. Meanwhile, Millennium East Pool dropped 6 cents to $1.78, furthering a 16-cent decline from the day before.

Starting Thursday and continuing until Oct. 19, Millennium Pipeline Co. is scheduled to perform maintenance on its MPC Huguenot loop tie-ins, according to Genscape analyst Josh Garcia.

Capacity through the Wagoner East throughput meter in Orange County, NY, will be reduced to 546 MMcf/d for the first two days of the event, then to 586 MMcf/d for the remainder, Garcia said.

“This represents cuts of 157 MMcf/d and 118 MMcf/d, respectively,” Garcia said. “This will add bullish pressure on Algonquin Citygate prices,” with Algonquin Gas Transmission already starting maintenance between its Stony Point and Oxford compressors, affecting 0.5 Bcf/d of mainline flows, the analyst said.

Spot prices were steady throughout much of the Midwest, Gulf Coast and Texas Wednesday as next-day Henry Hub deliveries traded flat at $3.13.

“Another cold front dips into the northern tier states by Thursday, with scattered showers expected along the boundary from the Upper Great Lakes to the Northern Rockies,” the NWS said. “This front also brings in a reinforcing shot of cold Canadian air, which may allow for snow to mix in across the higher elevations…Meanwhile out west, upper level ridging holds strong through Friday, which means conditions remain warm and dry.”

In California, SoCal Citygate gave up 9 cents to $3.70, while SoCal Border Average dropped 2 cents to $2.55.

Southern California Gas (SoCalGas) is running out of storage capacity, the utility said in a notice to shippers Tuesday. As a result, SoCalGas said it will be limiting injections to 65 MMcf/d starting next Monday (Oct. 1).

“The entire injection capacity of 65 MMcf/d will be reserved for system balancing, and there will be no capacity available for injection nominations,” SoCalGas said.

RBN Energy LLC analyst Jason Ferguson recently said a reduction in SoCalGas injection demand is likely to place downward pressure on West Texas spot prices this shoulder season as constrained Permian Basin producers lose an important destination for the region’s associated gas.

In West Texas, Waha dropped 3 cents Wednesday to average $1.36 after recovering from even more depressed pricing earlier in the week. Transwestern fell 24 cents to $1.36.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |