Markets | NGI All News Access | NGI Data

Traders Ignore Weather, Send September Natural Gas Lower as Expirations Nears; Spot Gas Mixed

September natural gas prices moved decidedly lower Friday despite weather patterns once again favoring intense heat in the long range. The Nymex September gas futures contract settled at $2.917, down 4.7 cents on the day.

Spot gas prices were mixed, however, as mild temperatures were expected to make way for hot high pressure set to arrive in the eastern United States late in the weekend, sending temperatures soaring back to well above-average levels. The NGI National Spot Gas Avg. dropped 4 cents to $2.69.

On the futures front, the Nymex September contract opened slightly higher and continued to gain modest strength early Friday, but traders gave more weight to factors other than weather later in the session, eventually sending the contract to its lowest level in more than a week.

Since weather patterns have added back several cooling degree days/Bcf Thursday night and so far Friday, “we see selling being more likely being due to other factors such as record production, positioning ahead of the weekend or the coming expiration” of September contracts,” NatGasWeather said.

Prices on the soon-to-be front month October contract have now provided some decent distance between $3, “giving bears some momentum before the break,” the forecaster said. Indeed, the Nymex October contract settled at $2.913, down 4 cents on the day, while the winter 2018-2019 strip (November-March) settled at $3.04, also a decline of 4 cents on the day.

Midday weather data confirmed cooler trends for late in the Aug. 27-31 week as weather systems with showers and minor cooling were forecast to track across the northern United States, weakening the ridge for the loss of demand. The latest Global Forecasting System model, however, was further hotter trending for the first several days of September and hotter trending overall, according to NatGasWeather.

It suggested Friday’s selling “has more to do with other factors besides medium-range weather patterns since they are still quite warm by late-summer standards,” the forecaster said.

The firm expects the hot upper ridge to steadily weaken Sept. 5-10, with late summer heat fizzling as the coverage of 90-degree temperatures rapidly decreases. “Essentially, the door is quickly closing on the opportunity for widespread summer heat after Sept. 8-10,” it said.

Still, even with summer weather quickly fading and production continuing to set new records, natural gas storage inventories remain at historic lows, a fact traders seem to largely ignore. The Energy Information Administration (EIA) on Thursday reported a 48 Bcf injection into gas stocks for the week ending Aug. 17, lifting inventories to 2,435 Bcf. Storage is now 684 Bcf below year-ago levels and 599 Bcf below the five-year average of 3,034 Bcf, EIA said. The deficit to year-ago storage levels shrank by 3 Bcf, while the deficit to the five-year average grew by 4 Bcf.

“Weather-adjusted, the market returned to being undersupplied (1.0 Bcf/d) despite U.S. production ramping 600 MMcf/d week/week,” analysts with Tudor, Pickering, Holt & Co. (TPH) said of the latest storage report. “Undersupply is set to persist as warmer-than-normal temperatures remain in the forecast.” Liquefied natural gas exports “remain volatile and the outlook is unclear as U.S.-China trade war chatter continues.

“The storage trajectory implies exiting injection season near five-year minimums,” but approval Thursday by the Federal Energy Regulatory Commission for “in-service of the Rover supply laterals raises the potential for a ramp in U.S. production that “may somewhat mitigate thoughts of a winter pricing spike,” TPH analysts said.

But as the market continues to shrug at large inventory deficits, it could be setting itself up for volatility during cold weather events this winter, Genscape Inc. senior natural gas analyst Rick Margolin said.

“Around mid-July, current-year inventories began setting the low mark for the five-year range, and now stand at their lowest levels for this date since at least 2009,” Margolin said. “Yet, despite the series of small injections reports and persistently low inventories, forward curves for the winter continue to struggle to print even a $3 handle as the market is placing higher confidence on supply growth picking up the slack.”

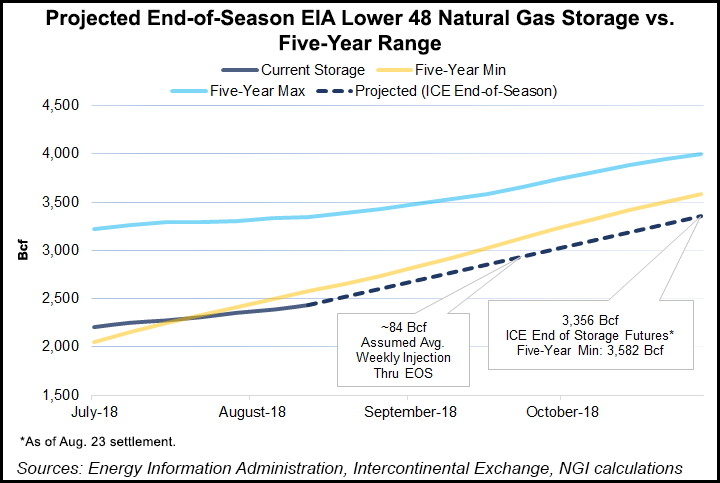

With 11 weeks remaining in the traditional injection season, it would take a weekly build of 88 Bcf in order to break the 3.4 Tcf barrier, a level which was considered the lower bound of market expectations a few months back, according to Mobius Risk Group. Intercontinental Exchange futures showed end-of-season storage inventories sitting at 3,356 Bcf, more than 200 Bcf below the five-year minimum of 3,582 Bcf. To achieve even this level, weekly injections would need to average 84 Bcf through the end of October.

Average injections during the peak summer months (June to thus far in August) have been about 7 Bcf larger than the corresponding weeks last year. Using that same trend through the end of October would lead to a pre-winter inventory level of less than 3.2 Tcf, Mobius said.

Weather will certainly have a great deal to do with pre-winter inventory levels. Heat intensity through Sept. 6 is forecast to be centered on a Southwest to Northeast path from the Texas Panhandle through the Great lakes region, Mobius analysts said. Although this geographic area historically has been dominated by coal-fired power generation, this summer has seen “parabolic gains” in natural gas consumption when temperatures have verified significantly warmer than normal.

“Over the next six to seven weeks, above-normal temperatures will drive bullish natural gas demand and for the final four to five weeks of injection season, colder-than-normal temperatures will begin to carry the torch for market bulls,” Mobius said.

Meanwhile, Genscape’s SpringRock production forecast is calling for production this winter to add more than 3 Bcf/d above summer’s levels, and more than 6.2 Bcf/d above last winter, Margolin said. “But individual region and field inventories running deficits increases volatility exposure during cold weather events that spike demand and/or trigger upstream supply disruptions like freeze-offs.”

Inventories in the East and Midwest, two of the coldest regions during the winter season, are tracking well below historical levels. As of Aug. 17, stocks were more than 100 Bcf below the five-year average in the East and more than 150 Bcf below the five-year average in the Midwest, EIA data show. The hefty deficits set the stage for increased injection activity in the coming weeks as local distribution companies work to assure adequate supplies ahead of the winter, according to EBW Analytics. This “may help support spot market prices, helping to limit the extent of likely declines in Nymex natural gas futures over the next six to 10 weeks,” CEO Andy Weissman said.

Sea Of Red For Spot Gas Prices

Spot gas prices across most of the country continued to lose ground Friday even as hotter weather was in store for parts of the United States in the days ahead. Strong high pressure remained on track to rapidly expand across the eastern half of the country beginning late in the weekend as high temperatures in the mid-80s to 90s were forecast to combine with humidity to return national demand to stronger-than-normal levels, according to NatGasWeather.

Where the data has been cooler is late in the Aug. 27-31 week, in particular across the northern United States, as the forecaster sees the ridge weaken on weather systems tracking across with showers and cooling. The hot ridge is then favored to spring back across most of the country except the West for the first several days of September; this is where the data has reverted back hotter Thursday night and so far Friday.

“We continue to expect the hot upper ridge should rapidly shrink in coverage Sept. 5-10 as shorter days make a more obvious impact,” NatGasWeather said.

While most pricing locations across the United States saw a retreat in prices before the weekend, some Northeast markets posted solid increases due to the incoming heat. Algonquin Citygate jumped 23 cents to $3.12, while Iroquois zone 2 moved up 12 cents to $3.09. Tennessee zone 5 200L was up 5 cents to $2.94, and Tennessee zone 6 200L was up 15 cents to $3.03. On the flip side, Transco zone NY and non-NY prices fell more than a nickel.

Meanwhile, Millennium Pipeline updated its maintenance scheduled yet again, pushing back the start date of its planned Wagoner East work to Wednesday (Aug. 29), one day later than its previously revised schedule. All flow estimates remain the same.

Also on Friday, Transcontinental Gas Pipe Line (aka Transco) told shippers that based on its schedule and forecasted progress, it is targeting full in-service for the 1.7 Bcf/d Atlantic Sunrise project to begin as early as Sept. 10. “The in-service date is based upon current contractor schedules and may further be affected by potential weather,” Transco said in a website posting. It plans to provide an additional update on Sept. 5.

Spot gas prices in Appalachia were generally lower, with the largest day/day losses seen at Columbia Gas, which fell 13 cents to $2.66. Dominion South slid 8 cents to $2.56, and Transco-Leidy Line dropped 7 cents to $2.54.

Regarding FERC’s authorization for Rover to place into service the Burgettstown and Majorsville laterals, it added no additional date requirements to the approvals, which means that the laterals can be expected to come online at Rover’s convenience, which may be as early as Friday (Aug. 24) or rolled out to a convenient contract start date of Sept. 1, according to Genscape natural gas analyst Collette Breshears.

The Burgettstown Lateral begins in southwestern Pennsylvania, where the 400 MMcf/d Energy Transfer Partners LP Revolution (ready for operation) and 200 MMcf/d MPLX Harmon Creek (due in 4Q2018) processing plants are located, “and runs almost due west to a connection with the beginning of the dual Rover mainline,” Breshears said.

Initial expectations for gas volumes on this line are low because of the startup of new processing systems, Genscape said. “While production in the area may improve, our regional production forecast accounts for this growth along with the less-constrained areas to the south and west, and doesn’t predict a sudden increase to overall regional production levels,” Breshears said.

The Majorsville Lateral will connect the 1 Bcf/d Majorsville processing plant in West Virginia to Rover just north of Clarington, Ohio, providing a competing route to Majorsville gas currently delivered to Texas Eastern Transmission and Columbia Gas Transmission. The proposed Iron Bank receipt point would potentially add incremental production onto the line later this year, Breshears said.

In the country’s midsection, Midwestern Gas Transmission (MGT) was scheduled Monday-Thursday (Aug. 27-30) to replace pipe on the mainline north of Carlisle in Sullivan County, IN, that would fully restrict southbound flow through Compressor Station (CS) 2113.

Average flow through CS 2113 has been around 235 MMcf/d for the past 30 days, however, more recently has averaged just 161 MMcf/d, Genscape natural gas analyst Vanessa Witte said. Total demand south of the outage area has averaged 294 MMcf/d during the past 30 days, excluding nominations beginning on Aug. 20 when the outage at Simpson began.

MGT has minimal receipt points south of Carlisle with the exception of Tennessee Gas Pipeline at Portland, which could increase deliveries to MGT to fulfill demand south of the outage area, according to Witte.

This event could also cause nomination reductions at the Scotland Rockies Express Pipeline (REX) interconnect farther north on the mainline, “as this is where MGT sources the majority of its gas,” Witte said.

The REX interconnect experienced a drop of roughly 171 MMcf/d on average during the Simpson outage from Aug. 20-23, according to Genscape.

Midwest and Midcontinent spot gas prices were a sea of red Friday, with losses of less than a nickel at most points in the Midwest and then steeper, double-digit declines in some areas of the Midcontinent. NGPL-Midcontinent was down 25 cents to $1.98.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |