Weekly NatGas Prices Mixed After Deep Losses at SoCal, Heat-Induced Gains Elsewhere

Weekly prices were mixed after weather forecasts trended hotter for the coming days after heavy rains doused demand in key markets earlier in the week. Solid gains in the futures market also lent support to cash prices late in the week, lifting weekly prices at the majority of points. Still, a dramatic plunge off record highs in southern California sent NGI’s Weekly National Spot Gas Average down 6 cents to $2.87/MMBtu.

SoCal Citygate posted the largest weekly decline as prices plunged $5.67 despite some late-week support from looming hot weather and pipeline maintenance. SoCal Citygate prices climbed as high as $27 in Friday’s trading session as work on the Southern California Gas (SoCalGas) system is expected to take a big chunk out of pipeline imports early in the week, when hot weather is forecast to return. Still, the weekly average of $13.74 was $5.67 lower on the week.

SoCalGas is scheduled to begin maintenance Tuesday that could cut nearly 300 MMcf/d of its imports, according to Genscape Inc. Pipeline operators will be performing a valve replacement at its T401 compressor station, which will cut operational capacity through the North Wheeler Ridge Zone by 420 MMcf/d.

That zone consists of the pipeline’s interconnects with Pacific Gas & Electric and Elk Hills, which together have averaged 393 MMcf/d during the past month. Only 100 MMcf/d will be able to flow as a result of this maintenance on Tuesday and Wednesday, Genscape said.

A note to customers posted Thursday by SoCalGas warned of the hot weather expected Monday through Wednesday and urged customers to schedule volumes accordingly, especially for Tuesday and Wednesday (the two days that this maintenance will be effective).

“Should this maintenance event proceed as planned — it has already been rescheduled once — SoCal will likely need to rely heavily on storage withdrawals to meet demand, given that its import capacity is already severely restricted due to the ongoing maintenance on L235-2 and L3000,” Genscape natural gas analyst Joe Bernardi said.

SoCal Border Avg. weekly prices also declined, plunging $2.91 to $4.42.

Outside of California, a return of hot weather lifted prices in the Northeast and Appalachia region. Weekly prices at the Algonquin Citygate rose 18 cents to $3.01, while Transco-Leidy Line jumped 16 cents to $2.50.

In the supply basin of West Texas, weekly prices at El Paso-Permian shot up 24 cents to $2.19, while Waha was up 33 cents to $2.22.

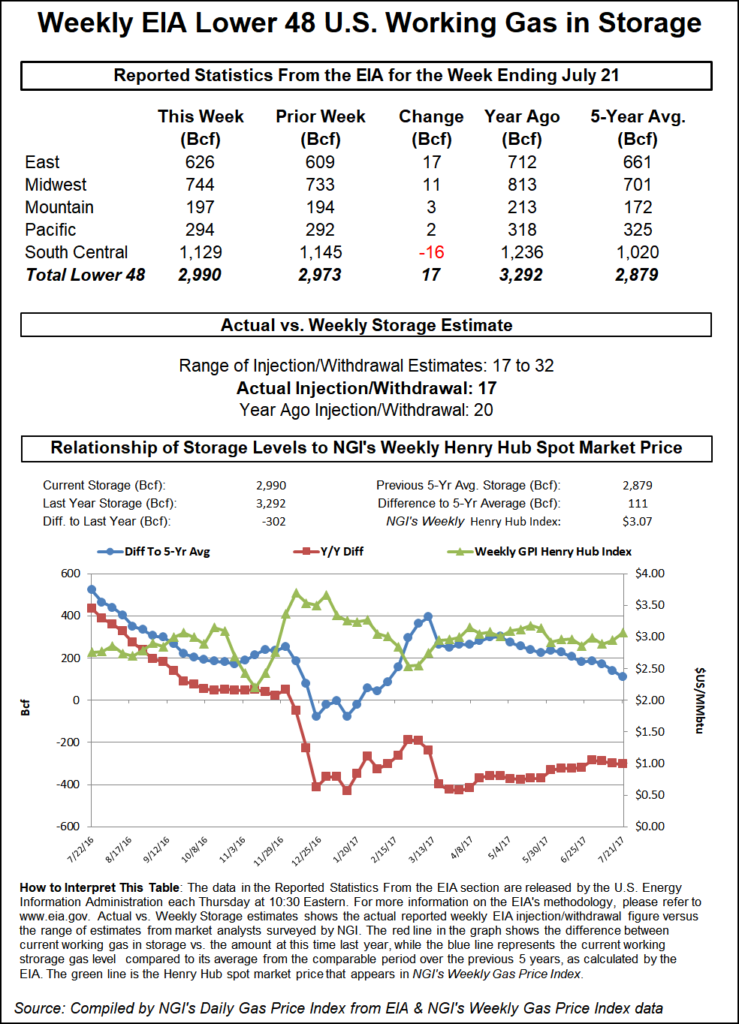

As for futures action, the Nymex September contract continued to rally Friday as traders appeared to be coming to terms with low storage inventories after the Energy Information Administration on Thursday reported another below-average injection. The prompt month climbed 3.7 cents to settle at $2.853; two-day gains totaled just shy of 10 cents.

It was a “surprising” turn of events compared with recent weeks, Bespoke Weather Service Chief Meteorologist Jacob Meisel said. After all, Thursday’s report was the third consecutive report in which the reported storage build fell below market expectations, but futures barely blipped in response.

Prior to the report, consensus had settled around a build in the low 40 Bcf range, in line with the five-year average. Kyle Cooper of IAF Advisors had projected a 40 Bcf build, while Genscape Inc. expected a 45 Bcf injection. A Bloomberg survey had a range between 25 Bcf and 58 Bcf, with the median response of survey participants coming in at 43 Bcf. Intercontinental Exchange settled at 43 Bcf.

Last year, some 18 Bcf was injected into storage inventories for the similar week, and the five-year average stands at 42 Bcf. Working gas in storage stood at 2,307 Bcf as of July 27, 688 Bcf below year-ago levels and 565 Bcf below the five-year average.

By region, the East injected 25 Bcf into inventories, the Midwest injected 28 Bcf and the South Central withdrew 12 Bcf. The Pacific also posted a withdrawal of 7 Bcf.

Meisel said Friday’s action was indeed a sign that persistently low storage inventories are finally causing a bit of concern in the market. While Thursday’s strength was concentrated at the front of the futures curve, Friday’s action saw much more participation through the winter strip, which rose 4 cents to $2.99, indicating a more sustained concern about low storage levels.

“Part of this move may be helping to price out scenarios where we walk into winter with less than 3.3 Tcf in storage,” Meisel told NGI. Bespoke’s end-of-season estimate remains at 3.39 Tcf, and given recent demand-side loosening, “we may be revising back slightly higher in the coming week if it continues,” he said. Every move lower in storage from that, however, poses a larger risk for a storage blowout this winter.

Still, Friday’s gains seem to represent a change in market dynamics; for the first time, the strip does seem to be pricing in storage concern, as can be seen in the slow, methodical move higher as well as the better participation by fall/winter contracts, he said. Yet with cooler risks later in August, storage injections seasonally beginning to increase. Early indications point to some weather-adjusted demand loosening, and it is this tight weather-adjusted demand that seemed to account for much of the bullish EIA misses the last few weeks. So it does not look like the overall fundamental picture outside of the storage deficit is about to become all that more bullish.

“The market can bounce on storage concerns, especially if next week’s number misses bullish to estimates yet again too, but it’s hard to see this as the beginning of a major rally given weak August seasonality,” Meisel said.

Meanwhile, production is expected to rebound this week following some minor maintenance and the typical beginning-of-month dip. Although the market may not see extraordinary growth in August, production should at least set new highs. “We aren’t hearing anything about any major slowdowns at this point that would really change our view,” Meisel said.

Analysts at Tudor, Pickering, Holt & Company (TPH) acknowledged that the market undershot liquefied natural gas demand, which was up more than 300 MMcf/d w/w. In addition, after being rebenchmarked to the latest monthly EIA data, Mexican exports are trending upward as data suggests incremental flows of about 100 MMcf/d on the El Encino-Topolobampo pipeline. Still, analysts “expect the market to be oversupplied entering withdrawal season (via a Northeast production ramp), but acknowledge short-term dynamics are getting increasingly more bullish with each passing week.”

For its part, Genscape Inc. said compared to degree days and normal seasonality, the EIA’s reported 35 Bcf injection is about 0.8 Bcf/d tight versus the five-year average. Relative to the previous week, total power generation was down about 12 average gigawatt hours (AGWH). Collectively, nuclear and renewable generation were up about 2 AGWH w/w as wind was up a little more than 2 AGWH and other renewables were close to flat w/w. Coal was down an estimated 8 AGWH w/w, and gas generation was down about 6 AGWH for an estimated -1.2 Bcf/d less gas burn w/w.

Meanwhile, Friday’s Baker Hughes Inc. Drilling Rig Count Report (for the week ending Aug. 3) showed the total number of U.S. rigs in unconventional basins falling to 867, down from 870 w/w but still up 105 over the year-ago level. The number of gas rigs fell by 3 rigs w/w, down to 183. Last year, there were 189 gas rigs running during the similar week.

Turning to the spot gas markets, prices continued to follow futures higher, with nearly 60 pricing hubs posting monthly highs as hot weather was expected to return to key demand regions in the days ahead.

In addition to SoCal Citygate, other western pricing hubs also posted increases, with PG&E Citygate edging up a couple of cents to $3.30, a new 30-day high. Malin jumped a dime to $2.69, also a fresh 30-day high.

Elsewhere across the country, heavy rains and weather systems that have battered the central-eastern United States are expected to continue weakening Friday as strong high pressure continues to build across the East Coast, according to NatGasWeather. This hot ridge is expected to expand to include most of the country during the Aug. 4-5 weekend and into the week, with widespread highs expected in the upper 80s to 100s, resulting in a return to strong national demand.

The cooler exception will be over the Northwest into California as a cool front arrives to bring brief relief from recent extreme heat. Demand will remain strong early in the week but will wane mid-week as weather systems track across the central, southern and eastern United States, with highs only reaching the 70s and 80s, the forecaster said.

“We’re expecting a very warm pattern to return across most of the country Aug 12-17 as upper high pressure restrengthens to dominate most of the country, with highs forecast to reach the mid-80s to 100s in most areas aside from the far northern United States.

In the country’s midsection, Consumers Energy spot gas shot up 9 cents to a new 30-day high of $2.89, as did Chicago Citygate, which jumped to $2.83, also a fresh high. Dawn jumped 11 cents to $2.99.

As previously mentioned by NGI, gas demand has been strong across Canada, and storage inventories continue to lag historical levels. As of Thursday, Dawn inventories sat 13% below the five-year average. Western Canadian storage stocks are currently 11% below the five-year average.

On July 27, intra-Alberta demand hit 5.3 Bcf, a record number for summer demand, according to TPH. Thus far, summer demand has averaged 4.7 Bcf/d, which is 5% ahead of last year’s peak day of 4.46 Bcf. In fact, so far this summer only two days have been below last summer’s best day and, overall, gas demand is up 11%, analysts said.

“It’s this demand growth that is primarily responsible for driving below-average injections, and while it has yet to cause a material pricing response, we continue to feel it’s only a matter of time before the AECO basis begins to close,” TPH said.

NOVA/AECO C spot gas plunged 41 cents to Cdn$84 cents/GJ.

Back in the U.S. Northeast, spot gas prices increased as temperatures in the premium demand markets like New York City were expected to climb back into the 90s by Monday. Transco zone 6 NY rose nearly 10 cents to $2.97, while Tennessee zone 6 200L picked up a nickel to reach $2.96.

Farther north, Algonquin Citygate spot gas reached a new 30-day high after climbing more than 13 cents to $3.09.

Over in Appalachia, Dominion South picked up a penny to hit $2.56 while Columbia Gas rose a nickel to $2.69.

Genscape reported that Columbia Gas Transmission will conduct work on Line 1983 South of Smithfield in West Virginia from Aug. 7 to 14, which will require operating capacity at Sherwood-1 to be reduced to 165 MMcf/d for the duration of the event, as well as possible reductions in firm capacity through Clenwayn and LoneOakA.

The current 30-day average at Sherwood is 623 MMcf/d with a high of 748 MMcf/d, while Clenwayn is flowing an average of about 920 MMcf/d southbound, Genscape analyst Vanessa Witte said. A similar restriction took place on June 19-20 due to modernization work on L-1983, though operational capacity at Sherwood was not reduced to a specified amount, she said.

“For that event, nominations at Sherwood decreased from an average of 665 MMcf/d to 270 MMcf/d, a 395 MMcf/d decrease. Flow through Clenwayn decreased less so, from an average of 980 MMcf/d to 780 MMcf/d,” Witte said.

Texas Eastern M-2, 30 Receipt spot gas moved against the grain as prices slipped a few cents to $2.56 after the pipeline experienced an unplanned outage on its Somerset, OH, compressor station on the westbound 24” Line.

Flows from the Sarahsville compressor station to the Lebanon compressor station have fallen by 161 MMcf/d compared to the previous 30-day average, Genscape natural gas analyst Josh Garcia said. Net flows further downstream on the 24-inch line up to the Batesville compressor station in east Indiana reversed as Midcontinent gas flowed into the Midwest to make up the difference.

“This outage creates bearish pressure on M2 prices as one of the outlets of Marcellus production is constrained,” Garcia said, noting that Tetco expects the outage to last three to four days.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |