July Natural Gas Rocked By Pipe Explosion, Sub-100 Bcf Storage Build; Spot Gas Climbs on Returning Heat

Nymex July natural gas prices found some support on Thursday as an early-morning pipeline explosion combined with another sub-100 Bcf reported storage injection from the Energy Information Administration’s (EIA) storage report to lift the prompt month some 3.4 cents to $2.93.

Spot gas prices also rose amid some returning heat to high demand centers. The NGI National Spot Gas Average rose 3 cents to $2.61/MMBtu.

Trading action was swift Thursday morning as news broke that Columbia Gas Transmission LLC’s (TCO) Leach Xpress Pipeline in West Virginia had exploded. TCO said about 1.3 Bcf/d of firm service could be disrupted indefinitely after the explosion and fire occurred on the line in Marshall County, WV, prompting the company to issue a force majeure.

TCO said that until further notice, capacity on the segment would be cut to zero. A spokesperson for TransCanada Corp., which owns the TCO system, said the incident occurred at 4:15 a.m. ET. The cause of the blast remains unclear and the impacted area has been isolated, the company said.

The Nymex July futures contract was up a nickel before the start of trading as news of the explosion spread, and support remained strong just before the storage report from the EIA.

“With supply growth being so critical to the health of summer fundamentals, it is no surprise that this morning’s Columbia Gas incident” in West Virginia was met with price upside, Societe Generale (SocGen) natural gas analyst Breanne Dougherty said. “Until the storage deficit softens, ALL bullish news is expected to get a pronounced market response.”

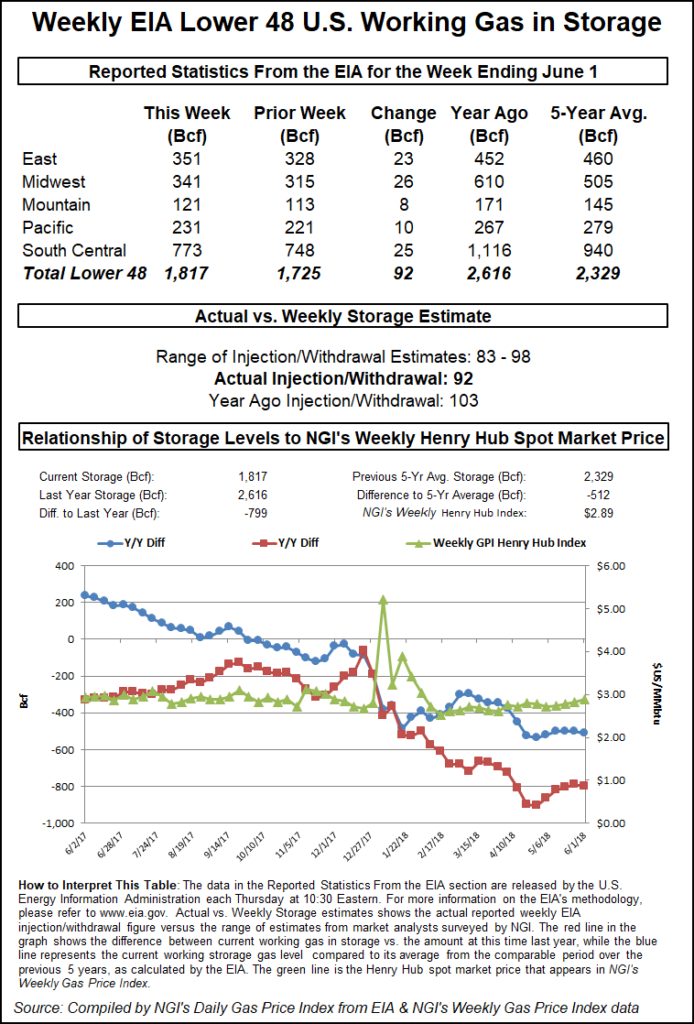

The prompt month jumped as high as $2.987 before the EIA storage report’s 10:30 a.m. ET release, but fell back to $2.96 as the reported figure — a 92 Bcf injection — crossed trading desks. The prompt-month eventually ended the day at $2.93, up just 3.4 cents.

The net 92 Bcf storage build compared with a 103 Bcf injection for the same week last year and the five-year average build of 104 Bcf. There were 71 cooling degree days (CDD) last week compared with 44 CDDs at the same time last year and a 30-year normal of 42 CDDs. In the week ended May 25, 96 Bcf was added to storage.

At 1,817 Bcf, stocks are 799 Bcf below year-ago levels and 512 Bcf below the five-year average of 2,329 Bcf.

Before the data’s release, market estimates were wide ranging, between 77 Bcf and 98 Bcf, and far short of the triple-digit injection some would expect from a holiday weekend.

INTL FCStone Financial Inc. Senior Vice President Tom Saal told NGI that the story was the Memorial Day weekend. “If we got over 100 Bcf, I wouldn’t be surprised. That weekend should produce a big number.” His official estimate, however, was for a 97 Bcf injection.

ION Energy’s Kyle Cooper projected a 97 Bcf injection, while a preliminary Bloomberg survey had a median estimate of an 89 Bcf build. A Reuters poll pointed to a 90 Bcf injection, and the Intercontinental Exchange EIA Financial Weekly Index settled Wednesday at an injection of 94 Bcf.

“This print is significantly looser from last week, indicating a slightly smaller injection despite very significant heat,” Bespoke Weather Services said. “However, Memorial Day holiday demand destruction likely played a large role, keeping us from reading too much into this.”

The forecaster was right on target with its 92 Bcf storage injection estimate. Bespoke’s Jacob Meisel said the EIA print indicated that the market is not tightening, something its daily power burn tracking had shown.

Given’s Thursday’s rally, SocGen’s Dougherty said market bulls have finally found confidence. While she was quick to note that the investment firm was not prepared to call the recent rise of the front to average just under $3/MMBtu a run, “it does bring the market almost in line with our base-case balance 2018 price view.”

Still, SocGen holds its bullish bias and emphasizes that “we see potential for core summer prices to surge over $3.15/MMBtu under the right scenario,” Dougherty said. Hot weather could provide such a scenario, but so could any type of supply disruption or even slowed production growth pace.

“We reiterate that our base-case requires production to grow to 79 Bcf/d by the end of June and to 82 Bcf/d by end-2018 in order to meet summer market demand and this year’s storage refill requirement,” she said.

With storage inventories now trailing year-ago levels by more than 30%, storage is below 2 Tcf after the first June injection for only the second time in the last decade, Jefferies analysts noted. The last time storage was sub-2.0 Tcf at this point was in 2014, when storage was much lower (~1.5 Tcf).

During that time, pricing averaged ~$4/MMBtu for much of the 2014 refill season, although production levels were substantially lower at that time (summer 2014 production of 69.7 Bcf/d versus 78.2 Bcf/d in May 2018). Given higher prices, gas power demand averaged only 27 Bcf/d from June-September 2014 versus the June-September average in 2017 of 31.3 Bcf/d, Jefferies said.

As for this year, gas power burn was 3.1 Bcf/d higher year/year in May and continues to maintain a ~2.4 Bcf/d higher year/year rate through the first week of June. While gas prices did average ~13% lower in May year/year, the higher burn likely shows some of the shift in the U.S. power generation mix (more gas/less coal), Jefferies analysts said.

Additionally, the National Oceanic and Atmospheric Administration weather outlook for the next two weeks, next month and the next three months all predict warmer-than-average weather over much of the United States, “which could further increase power burn versus last year. We estimate that if power burn averages 2 Bcf/d higher year/year through the summer, while gas continues to run at ~7 Bcf/d higher year/year, then storage will end the refill season at 3.4-3.5 Tcf (below the five-year average of 3.8 Tcf),” Jefferies said.

Turning to the spot markets, TCO’s pipeline explosion led to an unsurprising upswing at the Columbia Gas price point, even as next-day gas traded in a tight range of a nickel. Prices averaged $2.77, up 11 cents on the day.

Elsewhere in the Appalachia supply region, Dominion South moved sharply lower, plunging a quarter to $2.11. Tennessee Zone 4 Marcellus was down 18 cents to $1.91.

Spot gas prices in the Northeast got some uplift from warmer weather moving into the northern and eastern United States the next few days, with daytime temperatures in the 70s and 80s gaining ground, according to NatGasWeather. Meanwhile, very warm to hot conditions continue over the central and southern U.S. with 90s to 100s, including the Southeast, where a majority of the nation’s demand will be driven through the weekend.

Looking ahead, the forecaster said mostly comfortable temperatures are expected to return across the northern and eastern U.S. next week for light demand, while the southern U.S. remains very warm to hot.

Transco Zone 6-NY next-day gas averaged $2.77, a jump of 10 cents on the day, but trades ranged as low as $2.64 and as high as $2.87. Transco non-NY prices were up 17 cents to $2.77, while Tennessee Zone 6 200 leg prices were up just 2 cents to $2.59.

There was an exception to the overall gains in the Northeast. In New England, next-day gas took a dip as Genscape reported that a liquefied natural gas (LNG) cargo on the BW Boston was en route from Atlantic LNG in Trinidad and Tobago and was expected to arrive today. Algonquin City-gate traded at $2.34, down 17 cents.

Assuming a full cargo, this LNG shipment will fill most of Everett’s inventory, which Genscape estimates has only 396 MMCf out of 3.35 remaining. Everett is the primary fuel source for Exelon’s Mystic Generation Station, but the power plant has not cleared a day-ahead generation schedule since June 1 and has not shown significant generation since the morning of June 3, Genscape said. The maximum estimated burn it has observed is ~290 MMcf/d, “but Mystic has not run a full daily output schedule from CC units 8 & 9 (the two units fueled by Everett) since April 9. A now-operational Salem Harbor plant in the same zone reduces the power transmission risk of Mystic not running,” analyst Josh Garcia said.

Over in the Midwest and Midcontinent, spot prices were also on the rise, but gains were generally limited to less than a nickel. At the Chicago Citygate, next-day gas climbed 4 cents to $2.71, while Northern Natural Ventura inched up a penny to $2.60. NGPL-Midcontinent was slid 4 cents to $2.36, while Panhandle Eastern rose 4 cents to $2.39.

In the South, Henry Hub spot gas rose 8 cents to $2.93 and Columbia Gulf Mainline shot up 12 cents to $2.82.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2577-9966 |