Shoulder Season Lull for Weekly Natural Gas Spot Market; Futures Higher on Storage Miss

”Goldilocks’ weather in terms of Lower 48 natural gas demand produced a mix of mostly small spot price moves for the week ended Friday, while futures climbed — but remained range-bound — on a smaller-than-expected storage build; the NGI Weekly National Spot Gas Average fell a penny to $2.31/MMBtu.

Most points throughout Louisiana and Texas finished within a nickel of even, reflecting a week of generally flat trading across large portions of the spot market. Henry Hub tacked on 2 cents to average $2.73.

In Appalachia, restrictions from pipeline maintenance coincided with steep drops at a few points to end the week. Transco Leidy Line fell 15 cents to average $1.62, while Millennium East Pool shed a dime to $2.14.

In the Northeast, New England prices continued to moderate during the week, as Algonquin Citygate gave up 18 cents to average $2.29. In the West, the import- and storage-constrained SoCal Citygate fell 37 cents after producing a few volatile day/day moves during the week

Turning to Western Canada, NOVA/AECO C strengthened C32 cents to average C53 cents/GJ, bouncing back somewhat after setting an all-time low the week before, when maintenance restrictions contributed to negative spot prices there for a couple days.

Natural gas futures pulled back Friday but held onto the lion’s share of the previous day’s rally, with storage concerns supporting prices after a smaller-than-expected injection. The June contract settled at $2.806 Friday, down 0.8 cents on the day but almost a dime higher week/week after June’s $2.711 settlement the Friday before.

“It was a true shoulder season Friday in natural gas, with the prompt month contract trading in a record small 2.5 cent range through the day,” Bespoke Weather Services said. “This fits with expectations following” Thursday’s “large rally, as prices hit strong resistance at $2.82, and we saw few developments that would pull them above that level today.”

Thursday’s Energy Information Administration (EIA) storage report “showed less loosening than expected,” while recent weather data showed patterns developing that “should help keep cooling demand just slightly above average into the long-range,” according to Bespoke. “Though short-term heat is impressive, the latter half of May only has a slightly warmer bias, and it does not look to be anything to really get the market rallying.”

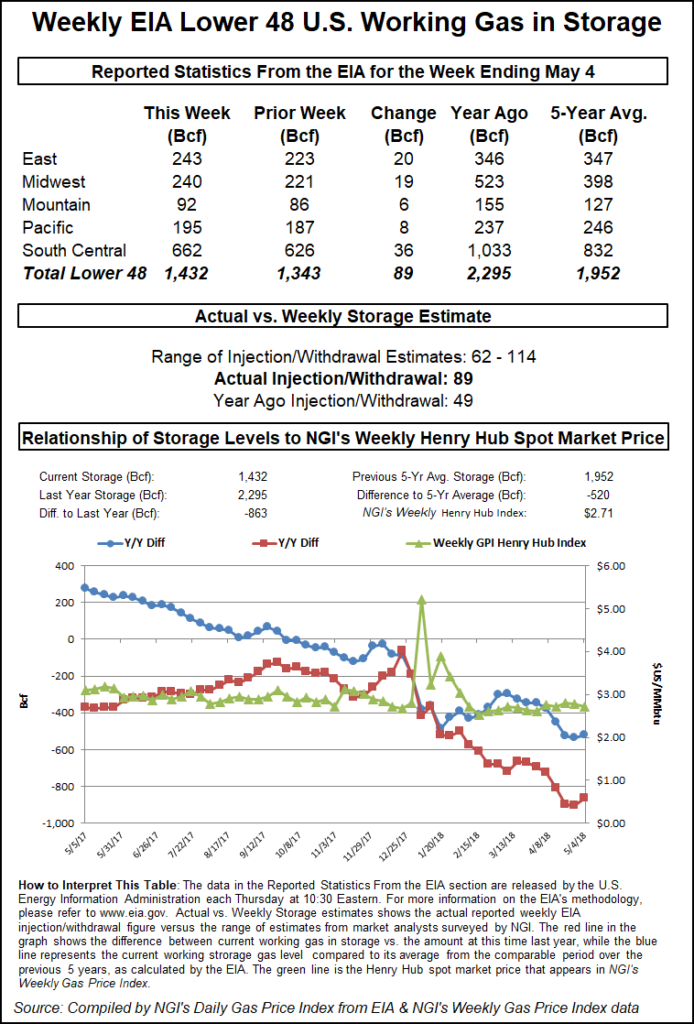

The Energy Information Administration (EIA) on Thursday reported a weekly natural gas storage injection that came in on the low side of expectations, and futures picked up some bullish momentum on the news.

EIA reported an 89 Bcf injection into Lower 48 gas stocks for the week ending May 4, slightly tighter versus consensus estimates for a build in the low- to mid-90s. Last year, EIA recorded a 49 Bcf injection. The five-year average is a build of 75 Bcf.

Prior to Thursday’s report, consensus estimates had the market looking for an injection somewhat larger than the actual figure.

A Reuters survey of traders and analysts on average had predicted a 91 Bcf build, with responses ranging from 75 Bcf to 114 Bcf. A Bloomberg survey had produced a median 90 Bcf injection, with a range of 62 Bcf to 114 Bcf. IAF Advisors analyst Kyle Cooper had called for a 96 Bcf build, while Intercontinental Exchange EIA storage futures settled Wednesday at an injection of 94 Bcf.

Total working gas in underground storage ended the period at 1,432 Bcf, versus 2,295 Bcf a year ago and five-year average inventories of 1,952 Bcf. The year-on-year deficit shrank week/week from minus 903 Bcf to minus 863 Bcf, while the year-on-five-year deficit decreased slightly from minus 534 Bcf to minus 520 Bcf, EIA data show.

By region, the largest injection came in the South Central at 36 Bcf, including 14 Bcf injected into salt and 22 Bcf into nonsalt. The East saw a 20 Bcf build for the week, while 19 Bcf was injected in the Midwest. The Mountain and Pacific regions saw builds of 6 Bcf and 8 Bcf, respectively, according to EIA.

Aided by the bullish surprise, the June contract surged 7.7 cents Thursday to settle at $2.814.

Thursday’s rally “demonstrates that bullish sentiment is not dead yet,” EBW Analytics Group CEO Andy Weissman told clients Friday. “Coming one week after EIA reported an injection 7-8 Bcf higher than expected, a 1-3 Bcf smaller-than-forecast injection is not sufficient, by itself, to explain the renewed rally.

“Traders who focus on the huge current storage deficit, however, interpreted” the week’s storage miss “as an indication that the next several injections might also be smaller than expected,” Weissman said. “This expectation is not likely to be fulfilled. Our storage model indicates that, from a supply/demand standpoint, market expectations for the past two injections were misplaced.”

EBW’s model shows the next several EIA storage injections clocking in north of 100 Bcf, a scenario made more likely if Thursday’s rally is sustained given the potential for higher natural gas prices to reduce coal displacement in the power stack, according to Weissman.

“The market was more than 2.0 Bcf oversupplied on a weather-adjusted basis,” analysts with Tudor, Pickering, Holt & Co. (TPH) said of this week’s storage number. “With U.S. production flat week/week,” liquefied natural gas “exports down about 0.4 Bcf/d and Mexican exports inert at around 4.4 Bcf/d, domestic demand remains strong.

“Initial estimates are predicting more” cooling degree days than heating degree days, “indicating that more demand is on the horizon,” the TPH analysts said. “All-in, the supply deficit is proving to be more resilient than initially expected.”

Genscape Inc. analyst Eric Fell noted that Thursday’s EIA number came in about 9 Bcf below the firm’s estimate, which had been higher than survey averages. The winter months also rallied Thursday “so that a $3 handle is back on CME’s board (January 2019) for the first time in about two weeks.

“This week’s storage report was driven in part by total degree days for the week running close to the five-year average (a rarity so far this year),” Fell said. “When compared to degree days and normal seasonality, the reported 89 Bcf injection appears loose by 0.7 Bcf/d versus the prior five-year average.” After the injection reported the previous week came in larger than expected, “there may have been some truing up this week.”

Meanwhile, days after President Trump’s decision to withdraw the United States from the Iran nuclear deal, analysts with Bank of America Corp. made headlines late in the week with a particularly bullish forecast predicting global crude prices could reach $100/bbl by next year.

June West Texas Intermediate crude oil futures settled above the $70/bbl mark Friday at $70.70/bbl, down 66 cents on the day.

In recent weeks, analysts have pointed to an inverse relationship developing between oil and natural gas given the prospect of higher crude prices driving associated gas growth out of areas like the Permian Basin.

Against this backdrop of rising crude prices, recent oil-driven growth in the U.S. rig count showed no signs of letting up during the week as 13 units returned to action, according to data released Friday by Baker Hughes Inc. (BHI).

The United States added 10 oil-directed rigs and three natural gas-directed rigs to finish the week at 1,045, up 18% from a year-ago tally of 885. Eight directional units were added, along with five horizontal units. Ten rigs were added on land for the week, along with two in the offshore and one in inland waters, according to BHI.

In the spot market Friday, a few Appalachian points sold off sharply amid maintenance-related constraints, while expectations for moderate weekend demand helped sink prices at SoCal Citygate; the NGI National Spot Gas Average fell 5 cents to $2.26/MMBtu.

Transco-Leidy Line tumbled 79 cents to average 97 cents Friday, with Millennium East Pool and Tennessee Zone 4 Marcellus seeing similarly large declines.

Transco told shippers Friday that it was conducting unplanned maintenance at its Compressor Station 520 in Salladasburg, PA, with the work expected to last through May 25. The operator said this would limit availability for non-primary firm transportation through Transco’s Leidy Line.

The Northeast and Appalachia are expected see even more maintenance-related restrictions next week, according to Genscape analyst Molly Rosenstein.

“Millenium will be performing maintenance in southern New York that may cause supply scarcity for the New England markets and shut in up to 1,000 MMcf/d of production” starting Tuesday and extending through May 19, Rosenstein said. “Additionally, the Wagoner West segment will be reduced by 400 MMcf/d from recent seven-day average flows.”

The restrictions could cause some volatility further downstream on Algonquin Gas Transmission and Tennessee Gas Pipeline, according to Rosenstein.

Elsewhere, Columbia Gas Transmission (TCO) is scheduled to conduct a pigging run on its Leach XPress pipeline Tuesday “that necessitates the shut-in of Gibraltar III and Majorsville for 6 hours,” according to Rosenstein. “The Majorsville gas processing plant has the ability to reroute onto Tetco, but Gibraltar III does not have re-route capabilities. The two have cumulatively supplied 688 MMcf/d onto TCO, on average, the past seven days; 233 MMcf/d of this was non-firm capacity” likely to be cut during the pigging run.

Prices weakened across the Midwest Friday as Genscape was calling for demand in the region to ease over the weekend, down to around 10.3-10.4 Bcf/d versus a recent seven-day average of closer to 12 Bcf/d.

Radiant Solutions was calling for temperatures in Chicago to flip from below-normal Saturday — including lows in the upper 40s — to somewhat warmer-than-normal by Monday, with highs in the mid-70s and lows in the mid-50s.

Chicago Citygate shed 6 cents to $2.37.

In California, SoCal Citygate tumbled 66 cents to average $2.21 as moderate demand forecast over the weekend appeared to limit enthusiasm for three-day deals at the volatile trading point.

Southern California Gas was calling for system demand to come in around 2 Bcf/d over the weekend, down slightly from actual demand of just over 2.1 Bcf/d Thursday. Receipts were expected to come in around 2.3 Bcf/d over the weekend, according to the utility.

Over the past few weeks, average spot prices at SoCal Citygate — a point hampered by ongoing import and storage restrictions — have tended to decline heading into the weekend before posting large increases on the following Monday, Daily GPI historical data show.

On May 4, the point shed 8 cents before jumping 44 cents on May 7. The week before that, SoCal Citygate fell 39 cents on April 27 before jumping nearly $1 day/day on April 30. Going back yet another week, SoCal Citygate plummeted 61 cents on April 20 before nearly doubling its average during trading on April 23, spiking $2.13 day/day.

Elsewhere in the region, SoCal Border Average fell 11 cents to $1.76, while El Paso S. Mainline/N. Baja dropped 12 cents to $1.75.

In Canada, a week after trading in negative territory and setting an all-time low at minus C1 cents/GJ, NOVA/AECO C averaged C26 cents/GJ on Friday, down C35 cents on the day.

“Western Canada storage reported a 5 Bcf draw this week, relative to our 4 Bcf forecast, but to us this feels like the opening act with the headliner set to come next week,” analysts with TPH said in a note Friday. “Inventory is reported on a one week lag, meaning” Thursday’s “number primarily captures the tail end of April, before maintenance turned everything on its head. Now that we’re thoroughly in the throngs of maintenance, we’re expecting a Lilliputian build of 0.6 Bcf” for the upcoming week, versus an 8 Bcf norm.

“As maintenance chokes off IT flows, which are required to flow in/out of storage, we expect builds to be sparse over May/June, during which 40% of the injections typically take place. This is where the rubber hits the road on our AECO trade and a sideways inventory trajectory should be the catalyst to get the strip moving higher.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |