Permian Natural Gas Supply Can Support Two Gulf Coast Delivery Pipes, Boardwalk Says

With the Gulf Coast Express project officially moving forward, Boardwalk Pipeline Partners LP continues to pursue additional plans to transport Permian Basin natural gas to the Gulf Coast, but a final investment decision (FID) has yet to be made, management said earlier this week.

During a conference call to discuss fourth quarter and full-year financial results, Boardwalk CEO Stanley Horton said the Houston-based master limited partnership (MLP) is “progressing in discussions” with potential shippers for its proposed Permian-to-Katy (P2K) pipeline, a joint venture with Sempra Energy.

In December backers of Gulf Coast Express, a joint venture of Kinder Morgan Texas Pipeline LLC, DCP Midstream LP and an affiliate of Targa Resources Corp., pulled the trigger on an FID for the 1.92 Bcf/d Waha to Agua Dulce natural gas transportation project.

Horton said Boardwalk management continues “to believe there will be demand for at least two natural gas pipelines from the Permian to the Texas Gulf Coast area and that demand for the second pipeline will be for deliveries into the Katy/Houston Ship Channel market, like our P2K project, which we anticipate will also feed into our Coastal Bend Header.

“Based on our conversations with producers and end-use customers, we remain optimistic about the project.”

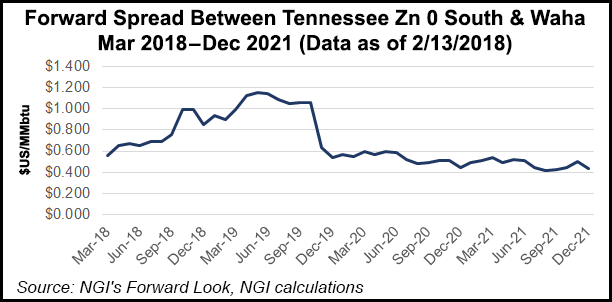

Negative basis differentials for Permian natural gas trading hubs have been an ongoing concern because of associated gas production growth from oil wells is butting up against limited pipeline takeaway capacity.

Analysts with Tudor, Pickering, Holt & Co. (TPH) said Tuesday the region “has a fighting chance to become the worst gas market in the U.S. in 2018…as supply growth outstrips near-term pipeline expansions.

“Based on the forward curve, 2018 realized prices are set to average $1.70/Mcf, while 2019 looks even worse at $1.56/Mcf (both years are down around 70-75 cents over the last three months),” analysts wrote in a note to clients. “This collapse has been a market concern since early 2017, as industry was quicker to prioritize liquids transport solutions…while counting on Mexico to bail out the regional gas market.”

However, “limited intra-county connectivity in Mexico has held exports roughly flat,” according to the TPH team, “and though we expect a modest uptick by year-end 2018, the current production forecast necessitates flows to Mexico reach about 2 Bcf/d by 3Q2019 prior to the expected in-service of Gulf Coast Express. About 2 Bcf/d of pipeline capacity to the Gulf Coast offers breathing room, but the Permian is likely in need of an additional greenfield project by the end of 2020.”

When asked what it might take for Boardwalk to move forward with the P2K project, Horton said, “We haven’t established an absolute firm guideline date for the FID,” he said. Pipeline capacity “could be from 1.7 Bcf/d all the way up to 2.2 Bcf/d, and you’d like to see firm commitments on that for the majority of the capacity before you would authorize the FID.”

Meanwhile, Boardwalk placed into service on Feb. 1 the first phase of the liquefied natural gas (LNG) focused Coastal Bend Header project, according to Horton. The project consists of 66 miles of 36-inch diameter pipe and is designed to deliver up to 1.4 Bcf/d to serve the Freeport LNG terminal on the Texas Gulf Coast.

“The first phase provides interim service for our customers that have contracted for Train 1 of the Freeport LNG facility until service under their long-term transportation contracts with us commences no later than Feb. 1, 2019,” Horton said.

The Freeport contracts total roughly 700 MMcf/d, he said. The project’s second phase, which includes interim service corresponding to Train 2 at Freeport LNG, is slated to begin commercial service by Nov. 1. Long-term contracts for Train 2, also totaling about 700 MMcf/d, are scheduled to begin May 1, 2019.

Horton also said facility construction remained on schedule and within budget “despite delays caused by Hurricane Harvey” and the devastating flooding it brought to the region in late August.

Boardwalk reported fourth quarter net income of $84.2 million (33 cents/unit), versus year-ago net income of $88.2 million (35 cents). Full-year 2017 net income totaled $297 million ($1.16/unit), versus 2016 net income of $302.2 million ($1.18). Distributable cash flow (DCF) in 4Q2017 was $110.6 million from $128.3 million in 4Q2016. Full-year 2017 DCF totaled $600.5 million, versus $507.3 million in 2016.

Boardwalk said its 4Q2017 results “were unfavorably impacted” by restructuring transportation contracts with Southwestern Energy Co. on the MLP’s Fayetteville and Greenville laterals. Last fall Southwestern secured an agreement with Boardwalk to restructure some firm transportation agreements and add others on the Texas Gas Transmission system to reduce excess capacity in the Fayetteville Shale and build in more flexibility to serve future production.

Boardwalk said results in the final quarter also was impacted by “decreases in storage and parking and lending revenues, partly offset from revenues from recently completed growth projects.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9966 |