NatGas Forwards Slide Third Straight Week Despite Late-Week Uptick

Near-record production and little cold weather to speak of combined to take their toll on natural gas forward markets this week, sending December prices down an average 2 cents between Oct. 27 and Nov. 2, according to NGI’s Forward Look.

It marked the third straight week of declines for natural gas forward markets as Mother Nature has yet to cooperate with market bulls in providing lasting cold weather. In fact, weather data overnight Thursday tracked a little warmer through Nov. 16, according to NatGasWeather forecasters, with some weather systems tracking across the northern United States for only occasional bouts of relatively cool temperatures.

“This will bring minor swings in heating demand every several days, but never exceptionally strong as northern U.S. weather systems fail to adequately tap the frigid cold pool just to the north over Canada. In addition, there will be milder periods between weather systems, so when averaged over weekly time frames, demand will only be near to slightly stronger than normal over the northern U.S., but below normal over the southern half of the US.,” NatGasWeather said.

Meanwhile, what the markets will likely be watching closely going forward will be whether Lower 48 production returns back above 75 Bcf/d, and also which direction northern and eastern U.S. temperatures trend after Nov. 15, with the onus firmly on the cold case gaining momentum if bearish weather headwinds are finally going to end, the forecaster said.

Indeed, it is beyond the mid-November time-frame where things get murky on the weather front. Harrison, NY-based Bespoke Weather Services said it is possible that the anticipated cold holds off until late in the month and into December, which would easily put a near-term cap on natural gas prices.

Regardless, the weather forecaster has added in gas-weighted degree days (GWDD) to its forecast as confidence in strong medium-term cold continues to increase, thereby increasing gas demand.

“We continue to favor the warmer range of long-range guidance too as we see no catalyst for major, sustained cold just yet, keeping our sentiment from being more bullish, but we note that GWDD additions remain more likely than GWDD losses, which should sustain this market a bit,” Bespoke said.

After shedding 3 cents over the week, the Nymex December futures contract was in the black Friday morning and traded as high as $2.986. Thursday’s settle was $2.935.

“The strip appears mildly supportive with gains out along the winter strip matching the front, though backs are lagging as underlying looseness plagues the market,” Bespoke said. “Throw in continued long-range bearish risks on weather models, and we are skeptical that we will be able to break above the $2.98 resistance we are approaching. A break of that could bring $3.02, but for now, we see the market as rather fairly balanced and unlikely to move significantly heading into the weekend.”

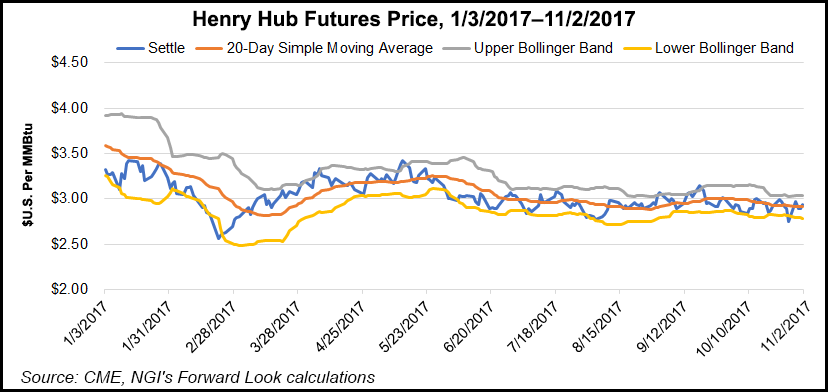

Looking ahead, Patrick Rau, NGI’s director of strategy and commodity research, said technical analysis shows slow stochastics are nearing overbought territory, if they aren’t there already. Major resistance exists in the $3.03-$3.04 area, which is marked by the top of the current Bollinger Band, and by multiple failed attempts to break that level since October.

“I do think there is some technical based activity around the corner, but my guess it will be selling, not buying,” Rau said.

Meanwhile, the recent bounce in futures could be indicative of the market digesting news that oil service costs may be rising a bit more relative to what E&P companies may have been expecting, which could impact 2018 E&P budgets. That’s one of the themes coming out of 3Q17 oil and gas industry conference calls, Rau said.

While precious few producers have given hints to their 2018 capex plans so far, all pressure pumping companies who have reported to date plan to pursue further price increases in the months ahead, Rau said.

“Given that the new mantra of E&P companies is to not outspend their cash flows, any unexpected increase in oil field services costs may curtail what they otherwise would have produced next year somewhat, so perhaps that is impacting the thinking of futures traders. It’s been very much in the news this week,” Rau said.

Taking a closer look at the markets, forward prices for December fell an average 2 cents from Oct. 27 to Nov. 2, while prices for January dropped an average 4 cents. The balance of winter (January-March) also was down an average 4 cents, according to Forward Look.

As has been the case for the last few weeks, Northeast pricing hubs continued to post more substantial losses. The end of a summerlong maintenance event on the Algonquin Gas Transmission system in New England and lackluster demand combined to send prices down by double-digits, in both the forwards and cash markets.

“The floodgates are open as the maintenance season started just before the summer, in June, and the most debilitating de-rate was for the last week in October,” said Stefan Baden, analyst with Energy GPS, a Portland, OR-based gas and power trading and risk management firm.

“The return of capacity was the most pronounced at the Stony Point compressor station where capacity more than doubled. In addition we saw .04 Bcf/d increase and that is the first incremental expansion from the Atlantic Bridge pipeline project. When it’s all said and done, it should be an addition of .13 Bcf/d.”

AGT Citygates December forward prices plunged 25 cents from Oct. 27 to Nov. 2 to reach $5.111, while January and the balance of winter (January-March) each fell a more moderate 10 cents to $8.507 and $7.36, respectively.

Elsewhere in the Northeast, Tennessee Zone 6 200 leg December forward prices were down 20 cents from Oct. 27 to Nov. 2 to reach $5.139, January was down 10 cents to $8.527 and the balance of winter (January-March) was down 10 cents to $7.42, Forward Look data show.

Transco Zone 6 New York December dropped 10 cents during that time to $3.886, while January tumbled a whopping 26 cents to $6.872 and the balance of winter (January-March) fell 17 cents to $5.86.

Across the border in western Canada, AECO forward prices got some uplift from a recent toll restructuring that went into effect Nov. 1 on the main pipeline connecting western supply to eastern demand centers.

TransCanada’s Long-term Fixed Price toll structure was offered to shippers in a successful open season in March that resulted in 27 new long-haul binding contracts from western Canadian gas producers to transport a total of 1.5 Pj/d, or 1.42 Bcf/d.

AECO December forward prices jumped 10 cents from Oct. 27 to Nov. 2 to reach $1.933, January climbed 5 cents to $1.973 and the balance of winter (January-March) rose 4 cents to $1.94, Forward Look shows.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9915 | ISSN © 2577-9877 |