Appalachian Takeaway, Haynesville Resurgence Tied to Overwhelming NatGas Supply Post-2017, Says Raymond James

A “massive” supply surge in U.S. dry natural gas production should overwhelm domestic demand by 5 Bcf/d-plus beginning in 2018 from increased Marcellus/Utica shale pipeline takeaway capacity, growing associated supply mostly from the Permian Basin, and a modest recovery in the Haynesville Shale, Raymond James and Associates Inc. said Monday.

Add to that growth in renewables for power generation, increasingly cost competitive with gas, and gas prices are set to decelerate instead of strengthen beyond 2017, said the analyst team led by J. Marshall Adkins, John Freeman and Pavel Molchanov.

Gas prices look weaker than had been forecast by the firm in early January, when Adkins and his colleagues said prices were poised for the best prices since 2014. While Raymond James is maintaining a 2017 forecast of $3.25/Bcf, the 2018 estimate has been slashed to $2.75 from $3.50 and the long-term forecast reduced to $2.75 from $3.00.

“All told, we now expect the 2018 U.S. gas market to be 1.1 Bcf/d looser (more bearish) than our previous outlook,” said analysts.

Burgeoning domestic gas supply growth beginning in the back half of 2017 and into 2018, is going to impact Henry Hub price forecasts — and not in a good way.

Mexican exports are lower and Canadian imports are higher this year, but the surge in renewable power “is likely to crush gas demand growth,” Adkins said. The three variables make the 2018 gas model almost 2 Bcf/d more bearish than originally forecast.

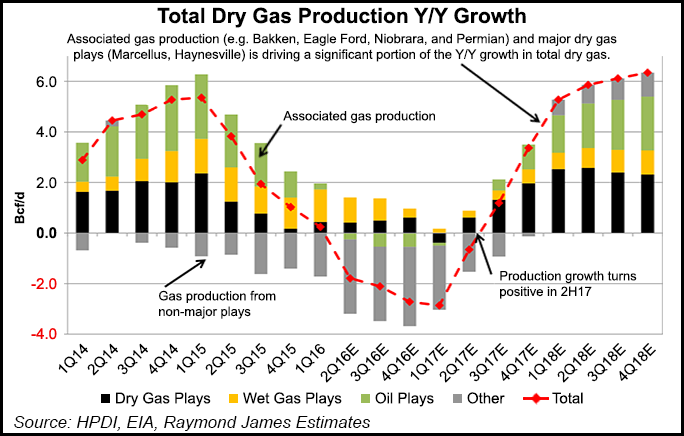

By the second half of 2017, U.S. gas supply should begin to accelerate. Compared with the its forecast early this year, the investment firm now expects U.S. dry gas production growth to be about 900 MMcf/d higher in 2017 year/year (y/y), based in part on revisions by the Energy Information Agency (EIA).

U.S. onshore gas production, which had been on a downward trend for more than a year, returned to the upside in January and was set to continuing moving higher into April, according to EIA.

Until the second half of this year, output from Raymond James’ modeled dry gas plays, the Marcellus, Haynesville, Fayetteville and Barnett shales, along with the wet gas Utica and Midcontinent, should remain muted, with slight y/y declines from associated gas in the Eagle Ford and Bakken shales, Niobrara formation and Permian Basin.

Beyond June, look for gas growth to pick up the pace, first in dry gas, followed by associated gas from oil wells.

The mighty Marcellus will carry the day in growth, up overall y/y at 1 Bcf/d “in anticipation of a plethora of midstream capacity planned for 2018,” followed by the Haynesville Shale rising by 0.2 Bcf/d.

“Taken together, dry gas production should be up 2 Bcf/d y/y by the end of 2017,” analysts said.

Associated gas growth should be roughly flat y/y because of minor declines in 1Q2017, but expect growth on that end into the second half of this year too, rising 1 Bcf/d y/y.

The Raymond James team anticipates declines in the other gas plays mostly to subside by year’s end, with growth relatively flat entering 2018.

Next year expect to see massive growth, led by the Marcellus, Utica, Haynesville and associated gas.

“Looking to 2018, we anticipate a pronounced recovery in dry gas production, particularly as a result of increased volumes from the Marcellus/Utica, a continued resurgence in the Haynesville, and growing associated gas production from increased activity in major oil plays (e.g., Permian, Eagle Ford, Niobrara),” Adkins said.

Planned pipeline capacity expansions underway should lead to meaningful growth from the Marcellus and Utica in 2018. In addition, threshold breakevens in the Marcellus and some areas of the Utica have fallen below $2.00/MMBtu, which has incentivized increased drilling and completion activity, as takeaway is accessible.

In the Marcellus alone, Raymond James model indicates 2.2 Bcf/d of y/y (November-November) growth in 2018, contributing 42% of overall dry gas growth for the year. About 6.5 Bcf/d of planned unrisked 2018 gas pipeline takeaway capacity also is expected to come online in Appalachia, further accelerating growth.

In addition, analysts advised to not underestimate the Haynesville’s gas supply contribution. A resurgence in the North Louisiana/East Texas play should drive “respectable” y/y dry gas volumes in 2018.

“The rig count bottomed at 12 rigs in April 2016, but in 2018, we anticipate the rig count to average 42 rigs, up 3.5x times from the trough,” Adkins said. Enhanced completions, mostly because of increased proppant loads, have led to a revival in single well economics.

“In 2018, we anticipate dry gas volumes in the Haynesville to increase 0.5 Bcf/d y/y to 6.3 Bcf/d,” analysts said.

Meanwhile, associated gas growth from oily basins should be the final straw, with more than 1.5 Bcf/d of growth in 2018 y/y, with nearly all of it (1 Bcf/d) from the Permian.

As the Eagle Ford also begins to awaken, dry gas output should be up 0.5 Bcf/d y/y in 2018, making up a “sizable” share of associated growth.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2158-8023 |