NGI Weekly Gas Price Index | NGI Data

Southeast, Northeast Lead The Pack Higher In Weekly Natural Gas Trading

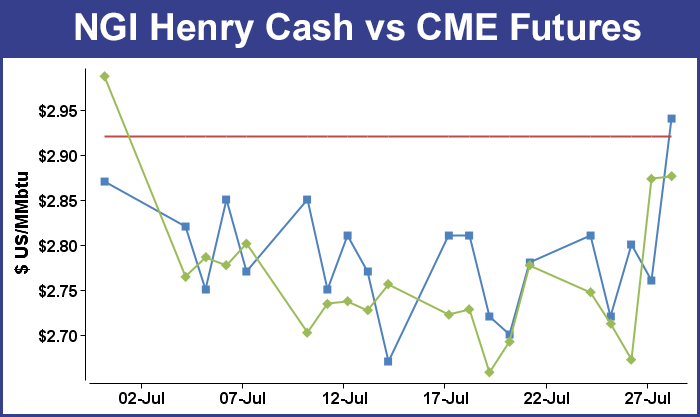

Last week attention was focused on California and the fractious weekly trading that had that state posting a stout 17-cent weekly gain to $2.91, but this week’s short four-day trading week highlighted price moves in the Southeast and Northeast.

The NGI Weekly Spot Gas Average rose a minuscule 2 cents to $2.59, but the Southeast added 14 cents to $2.97 and the Northeast gained 13 cents to $2.68. The week’s market point with the biggest move was Florida Gas Transmission with a gain of 97 cents to $4.19 and the largest loss was Empress with a 14-cent decline to $C2.34.

Regionally the Midwest was weakest with a 4-cent decline to $2.68 and both the Midcontinent and Rocky Mountains were set back a penny to $2.61 and $2.57, respectively.

All other regions were either flat or in the black. Appalachia and South Louisiana were unchanged at $2.71 and $1.52, respectively.

South Texas and East Texas mirrored each other with a penny rise to $2.70, and California added 7 cents to $2.98.

August futures expired Wednesday at $2.672, 24.5 cents less than the July contract settlement.

September futures for the four-day trading week gained 9.6 cents to $2.873.

In Thursday’s trading physical gas for Friday delivery and futures markets parted company. Physical traders, especially in the Northeast, only had to look at Friday’s temperature forecasts and next-day power prices to see little incentive for incremental purchases. The NGI National spot gas average dropped 8 cents to $2.53, but declines in the Northeast averaged more than a half dollar. Relative strength in Texas, the Midwest, Midcontinent and South Louisiana were no match for the lower quotes posted in New England and the Mid-Atlantic.

Futures bulls responded gleefully to an Energy Information Administration (EIA) storage report that showed an anemic storage build of just 17 Bcf, well below market expectations and well below historical averages. By the close, September had tacked on 21.3 cents to $2.873 and October was higher by 20.0 cents to $2.909.

The main price driver Thursday was the EIA storage report and traders expected to get an idea of just how much recent widespread heat had affected supplies with the 10:30 a.m. EDT release of inventory statistics from the EIA. Current thinking was that the build would be less than 30 Bcf, and perhaps the lowest July build since 2010.

When EIA reported a 17-Bcf storage injection, about 9 Bcf less than what traders and analysts were calculating, September futures bounded higher and reached a high of $2.816 immediately after the figures were released and by 10:45 a.m. September was trading at $2.811 up 13.9 cents from Wednesday’s settlement.

“We were hearing a number from 24 to 28 Bcf and 26 Bcf was kind of the average,” a New York floor trader told NGI. “That number coming out so low gave confidence to anybody who was long, and anybody who got caught short got burned.”

Analysts were pointing at a miscalculation of power burn. “The smaller than expected 17 Bcf net injection for last week was less than expected and bullish compared with the 52-Bcf five-year average for the date,” said Tim Evans of Citi Futures Perspective. “It was a second consecutive bullish miss, adding to the likelihood that power sector demand has been more sensitive to summer heat than anticipated, something that will likely carry over into the data for the next few weeks.”

Others were more animated. “Are you kidding me?” said John Sodergreen, editor of The Desk weekly storage survey. “There was some serious activity going on in South Central, but Midwest was about par. The South Central was a greater draw than anyone expected and it’s a situation where there is a lack of transparency and nobody knows what the hell is going on.”

Inventories now stand at 3,294 Bcf and are 436 Bcf greater than last year and 524 Bcf more than the five-year average. In the East Region 18 Bcf was injected and the Midwest Region saw inventories increase by 14 Bcf. Stocks in the Mountain Region rose 3 Bcf, and the Pacific Region was unchanged. The South Central Region, however, fell 18 Bcf.

Friday temperature forecasts at major market centers were all sellers needed to keep prices submerged. Forecaster Wunderground.com predicted that Boston’s Thursday high of 92 degrees would plunge to 76 Friday before recovering to 82 by Saturday, the seasonal average. New York City’s high of 92 Thursday was expected to be followed by Friday’s high of 80 before making it back to 84 on Saturday, the seasonal average.

Friday gas at the Algonquin Citygate fell 74 cents to $2.21, and deliveries to Iroquois, Waddington skidded 14 cents to $2.64. Gas on Tenn Zone 6 200L lost 77 cents to $2.16.

Packages destined for New York City on Transco Zone 6 dumped 73 cents to $1.66, and gas on Tetco M-3 changed hands 9 cents lower at $1.35.

Next-day power prices were also lower. Intercontinental Exchange reported that on-peak power for delivery to ISO New England’s Massachusetts Hub Friday fell $17.01 to $35.10/MWh and on-peak power at the PJM West Terminal dropped $5.45 to $33.93/bbl.

At some point, lower prices will be colliding with lower production. “Lower 48 dry gas production is off more than 0.5 Bcf/d DOD with large declines in the Gulf of Mexico, Texas and the Rockies,” said industry consultant Genscape in a Thursday report. “Spring Rock’s Daily Pipe Production estimate has today’s volume at 71.8 Bcf/d. GOM production is down more than 0.2 Bcf/d DOD due to offshore losses. Destin receipts from Delta House are down to 74 MMcf/d, a 132 MMcf/d drop from yesterday and the prior 30-day average.

“Evening noms to Transco from Tubular Bells are also off, coming in at 9 MMcf/d after having averaged 47 MMcf/d in the past 14 days. Elsewhere, Texas estimated production is down 148 MMcf/d DOD, and Rockies volumes are off 103 MMcf/d DOD with declines showing in every basin but the Uinta.”

Tom Saal, vice president at FCStone Latin America LLC, in his work with Market Profile identified trading targets based on certain levels of price action. The first trading objective is for the market to test Wednesday’s value area at $2.713 to $2.679, but beyond that Saal identifies the initial balance at $2.713 to $2.679. The week’s storage report often provides a catalyst for prices to break out of the initial balance and reach trading targets both higher and lower. An upward breakout from the initial balance would look for an objective of $2.767 and a downward break has an objective of $2.584.

Looking at national average natural gas cash prices for next-day gas deliveries Wednesday might make one think summer doldrums have set in, but nothing could be further from the truth. Sharp weather-driven surges in West Coast power prices, and a Flex Alert called by the electric grid operator, had California prices posting stout double digit gains. On the East Coast, major market centers showed double-digit losses, but the NGI National Spot Gas Average rose a lackluster 3 cents to $2.61.

The expired August futures limped across the finish line. August settled at $2.672, down 4.0 cents, and September ended at $2.660, down 1.7 cents. September crude oil continued to unravel losing $1.00 to $41.92/bbl.

Next-day power in California jumped as major markets were expected to see temperatures 10 degrees or more than normal. Forecaster Wunderground.com said the high Wednesday in Los Angeles of 91 degrees would “ease” to 85 Thursday before rebounding to 88 Friday. The seasonal norm for Los Angeles is 76. Sacramento’s 106 max Wednesday was expected to be 105 Thursday and 104 Friday. The normal high in Sacramento this time of year is 93.

Gas at Malin added 7 cents to $2.73, and deliveries to the PG&E Citygate added a nickel to $3.15. Packages at the SoCal Citygate jumped 25 cents to $3.42, and gas priced at the SoCal Border Avg. Average rose 33 cents to $3.26.

Inbound gas on El Paso S. Mainline/N. Baja vaulted 51 cents to $3.61 and gas at Kern Delivery rose 43 cents to $3.46.

“Gas nominations at Opal were down sharply, and that passed through to Kern Delivery,” said EnergyGPS principal Jeff Richter. “Also, gas on El Paso just got diverted back east to satisfy heat-related requirements in Las Vegas and other points. With Kern and El Paso so much higher than SoCal Border and SoCal Citygate, those points now have to rely on storage gas.”

The California Independent System Operator (CAISO) forecast Wednesday’s peak load of a hefty 45,786 MW would increase to an even heftier 46,888 MW Thursday.

CAISO issued a Flex Alert for Wednesday from 2-9 p.m. and urged residents to conserve electricity to avoid power disruptions (see related story).

CAISO also said it was declaring restricted maintenance on grid generation operations for the period from Wednesday from 6 a.m. to 10 p.m. and declared that the grid operator “anticipates generation resources may be inadequate for the period covered by this notice.”

Eastern market center prices went in the other direction. Gas bound for New York City on Transco Zone 6 fell 23 cents to $2.39, and packages at the Algonquin Citygate shed 22 cents to $2.95. Gas on Tennessee Zone 6 200 L was quoted 15 cents lower at $2.93.

Tim Evans of Citi Futures Perspective sees the market eventually moving lower as cooling demand subsides and storage injections increase.

“While hot summer temperatures remain a current support for the market, we continue to see the seasonal cooling trend that will follow as a bearish factor, at least relative to the prevailing price level,” Evans said. Expectations for Thursday’s Energy Information Administration storage report “for the week ended July 22 are still being compiled by the major newswires, but estimates we’ve seen so far suggest a consensus running in the vicinity of 30 Bcf in net injections. This would be a modest decline from the 30 Bcf refill in the prior week and a supportive contrast with the 52 Bcf five-year average gain.”

Evans estimated a 24 Bcf build, and he suggested this sets the market up for a bullish surprise. His figures show that by Aug. 12, the year-on-five-year storage surplus could fall from its current 559 Bcf to 428 Bcf.

Other estimates of Thursday’s storage build are somewhat higher. Raymond James estimates an increase of 30 Bcf, and a Reuters survey of 18 traders and analysts showed an average 26 Bcf with a range of 22 Bcf to 33 Bcf. Last year 52 Bcf was injected, and the five-year average is also a 52 Bcf build.

Evans said he wouldn’t “rule out” a continuation of this trend, although he doesn’t have a specific forecast. “This declining surplus confirms that the market is becoming tighter on a seasonally adjusted basis, which most often translates into rising prices over the intermediate term.”

Once cooler temperatures set in, power sector demand is likely to decline.

“We think this weakening of current demand may allow the market to fall to the $2.40-2.50 range in the weeks ahead, which we view as a more appropriate discount to last year’s valuation given what was still a 471 Bcf year-on-year storage surplus as of July 15,” Evans said.

He is currently on the sidelines awaiting a new, limited-risk trade entry.

Weather-wise, look for brief respite from eastern heat followed by a return of warmth by next week.

“Fresh midday weather data continues streaming in, and again no major changes in the latest weather data, although there remain important differences between some of the major weather models on just how hot the first half of August will play out,” said Natgasweather.com in an update.

“To our view, regardless, it will be very warm to hot with stronger than normal nat gas demand. Until then, after a hot start to the week, cooler temperatures will spill across the Great Lakes and Mid-Atlantic over the next several days due to a weather systems with showers and thunderstorms tracking through. This cooler period will last through the coming weekend, easing natgas demand from recent very high levels to just slightly above normal even though it remains quite hot and humid with 90s and 100s over the western, central, and eastern U.S.

“However, as expected, early next week the hot upper ridge will bounce back with increasing strength, while also expanding back across much of the northern and eastern U.S. to bring another several day period of very strong nat gas demand around Tuesday through Friday of next week.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1258 |