Markets | NGI The Weekly Gas Market Report

NatGas Forwards Make it Four Weeks Higher on Heat, Storage

Intense heat and a below-average storage injection lifted natural gas forwards for a fourth straight week, according to NGI’s Forward Look.

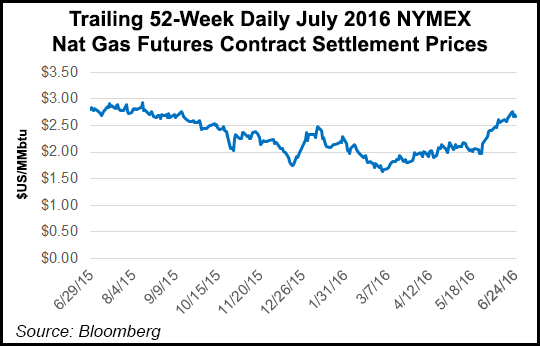

The Nymex July contract rose 7.6 cents from June 17 to June 23, capping a volatile week that included a sharp sell-off the day before the U.S. Energy Information Administration released its weekly storage report.

The reported 62 Bcf injection was slightly more than what was expected by the market, but once again came in well below the five-year average of 88 Bcf, a trend likely to continue as cooling demand strengthens.

The July contract has risen more than 55 cents over the last four weeks.

Nevertheless, it’s hard to ignore the fact that inventories are still 618 Bcf higher than last year at this time and 678 Bcf more than the five-year average.

“I think the price strength is partly a reflection of the injections continuing to come in lower than expected. It is creating ambiguity about whether market expectations of supply are being overstated or whether there are demand components being missed,” said Genscape’s Rick Margolin, senior natural gas analyst.

Genscape, based in Louisville, KY, is a real-time data and intelligence provider for energy and commodity markets.

Indeed, much of the U.S. saw above-average temperatures last week that lifted power burn to a new all-time high for June.

U.S. demand notched up nearly 2 Bcf/d week over week, reaching 68.9 Bcf/d on June 20, according to Bentek Energy.

The high power burn will likely set a record average for June given Bentek’s seven-day projection of 66.3 Bcf/d and the current month-to-date average of 64.6 Bcf/d, the company said.

Indeed, power burn so far this summer has been notable, Margolin said.

“This has been impressive because of the growth of renewables, mild weather relative to the past two summers-to-date [up until this week], and the inability of price gains to sap momentum from gas pricing coal out of ISO stacks,” Margolin said.

The market’s increased structural reliance on natural gas for power generation has become increasingly evident.

“It would appear that the recent retirement of peak-shaving coal units combined with lower priced gas has created a ”spring board’ for electric power demand as heavier cooling load brought less efficient gas units into service,” said Teri Viswanath, managing director of natural gas at PIRA Energy Group.

She cautioned, however, there are factors that could limit the build in cooling demand this season.

“For example, high levels of soil moisture in Texas will probably continue to result in cooler anomalies in that state.

“Moreover, heightened tropical storm activity might limit the periods of extended warmth in the Gulf,” Viswanath said.

The latest weather forecasts don’t offer a clear picture either.

While hot temperatures that have dominated the southern two-thirds of the U.S. expanded into the Northeast this past weekend, this week is expected to bring heavy showers and cooler temperatures.

What will be important to the markets during the weekend is what sets up the second week of July, said forecasters at NatGasWeather.

“If the same pattern that sets up late next week is able to continue past July 7,where cooling filters into the East and hot temperatures remain focused on the west-central U.S., the markets could be disappointed it’s not hot enough,” NatGasWeather said.

The agency, however, believes there’s a decent chance the ridge rebounds to include the east-central U.S. with temperatures in the upper 80s to 100s again becoming widespread across much of the country and a return to fairly strong natural gas demand.

“Of course, bigger picture, weekly builds will continue to underperform versus five-year averages due to tighter S/D balances. This should allow surpluses to continue their steady decline in the weeks ahead,” NatGasWeather said.

But given that season-to-date contraction in the stock build has been driven in part by transient factors, namely weather and price-induced fuel switching, the price recovery seen in the natural gas market will continue to require an assist from supply losses, Viswanath said.

“In the event that the deterioration in supply does not occur fast enough or the weather begins to moderate, prices will likely begin to soften to ensure that the transient factors in play so far this season pick up the slack,” Viswanath said.

Production was reported to have slipped to just under 70 Bcf/d Friday.

Prices were up across the forward curve.

The Nymex August contract rose 7 cents from June 17 to June 23, while the balance of summer (August-October) was up 6 cents, the prompt 2016-2017 winter was up 7 cents and the winter 2017-2018 strip was up 3 cents.

Nationally, NGI’s forward prices posted similar gains.

Prices climbed an average 7.5 cents for July, 8 cents for August and 6.8 cents for the balance of summer, according to Forward Look.

The prompt winter, meanwhile, rose an average 8 cents, and the winter 2017-2018 moved up 5 cents.

Interestingly, New York put up far more substantial increases at the back of the curve.

Transco zone 6-New York winter 2016-2017 jumped 33 cents from June 17 to 23, while the winter 2017-2018 shot up 27 cents, Forward Look data shows.

Other Northeast points, including New England’s Algonquin Gas Transmission city-gates, did not see the same strength.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 1532-1266 |