Markets | NGI All News Access | NGI Data

NatGas Cash, Futures Inch Higher Even as Storage Makes Historic Move

Physical gas for delivery Wednesday rose modestly in Tuesday’s trading as strong performances in the Midwest, Texas and Gulf Coast overshadowed weaker pricing in the Rockies, California and East.

The NGI Daily Spot Gas Average rose 1 cent to $2.59, but most points traded either side of unchanged. Futures continued their march higher, with July trading at a new high for the move to $2.768 before settling at $2.768, up 2.1 cents. August finished at $2.798, up 2.1 cents as well. July crude oil shed 52 cents to $48.85/bbl.

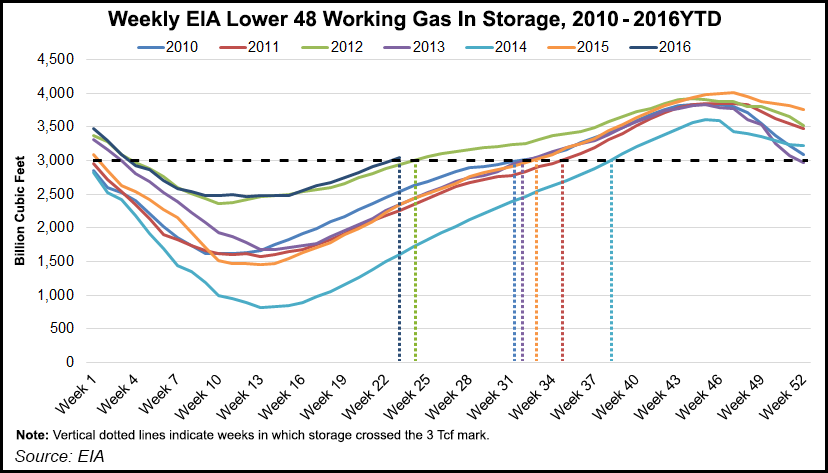

Last Thursday’s Energy Information Administration storage report for the week ending June 10 signaled the earliest point in an injection season where working gas exceeded 3 Tcf at 3.041 Tcf. The only other time that came close in the 23 years of record-keeping was in 2012, when 3,006 Tcf was reached for the week ending June 15.

Such an early breach of 3 Tcf could spell storage difficulties down the road as abundant supplies compete for limited storage, or not. “The levels are really high, there is no question about it,” Tom Saal, vice president at FCStone Latin America LLC in Miami, told NGI. “But the amount going in on a weekly basis is below what people are looking for. They are definitely below any recent historical averages.

“There is either more demand or less supply or both, and I think the numbers that are below historical averages are pretty significant. The cure for low prices is low prices, and I think we are seeing the results of that.

“Lower prices lowers supply and raises demand,” Saal added. “Weather demand is more instantaneous than longer term industrial demand, but anyone looking at natural gas as a fuel is looking at historically low prices.”

Market bulls may want to take note. If 2012 is any guide, prices may be in for further advances. Spot futures following the move past 3 Tcf in 2012 were at a low of $2.17 on June 14, but by October 30 2012 spot futures had risen to $3.82.

In physical market trading next-day gas in New England slumped as next-day power eased. Intercontinental Exchange reported that on-peak power at the ISO New England’s Massachusetts Hub fell $3.11 to $33.06/MWh and power at PJM West slumped $9.63 to $32.05/MWh.

Quotes at the Algonquin Citygate fell 39 cents to $2.68, and gas at Iroquois, Waddington shed 11 cents to $2.74. Deliveries to Tennessee Zone 6 200 L fell 52 cents to $2.69.

In the Mid-Atlantic prices firmed. Gas on Tetco M-3 came in 3 cents higher at $2.02, and gas headed for New York City on Transco Zone 6 gained 6 cents to $2.25.

Quotes in California suffered a similar demise as next-day power tumbled also. Intercontinental Exchange reported that on-peak power at NP-15 for Wednesday delivery fell $1.51 to $34.58/MWh and power at SP-15 tumbled $9.95 to $36.44/MWh.

Gas at the PG&E Citygate added 3 cents to $3.01, but parcels at the SoCal Citygate fell 7 cents to $3.07. Gas priced at the SoCal Border Average was quoted 4 cents lower at $2.91, and deliveries to El Paso S Mainline skidded 12 cents to $2.93.

Midwest quotes were firm. Gas on Alliance rose 7 cents to $2.73, and gas at the Chicago Citygate added 7 cents to $2.74. Gas on Consumers rose 8 cents to $2.75 and gas on Michigan Consolidated changed hands up 7 cents to $2.74.

Analysts see weather as the primary price driver and anticipate that extended heat is capable of carrying the market higher.

“Hot weather remains as the primary bullish force that has driven this month’s dramatic gains, and until the forecasts begin to normalize or show a sustainable cooldown, line of least price resistance could remain to the upside,” said Jim Ritterbusch of Ritterbusch and Associates in a Tuesday morning note to clients.

“While we approached the short side briefly before virtually scratching the trade, we have shifted off of a negative view as updates to the short-term temperature outlooks continue to advise much above normal temperature trends that spread across a broad portion of the U.S. While deviations from normal within the heavily populated northeast quadrant don’t appear sizable, there does appear to be enough heat on the horizon into the 4th of July holiday weekend to keep weekly EIA injections sharply downsized relative to both last year and the five-year averages.

“Our expected supply increase on Thursday would cut the surplus further by around 30 Bcf while reducing the overhang against last year by 20 Bcf. This dynamic of a sizable contraction in the large supply overhang will continue to be prioritized over the fact that the stock surplus will remain at around 670 Bcf following Thursday’s EIA report.”

Weather models warmed incrementally overnight. “Widespread above average period anomalies are expected during the six-10 day period. The most anomalous heat will continue to be found over the southwestern U.S,” said WSI Corp. in its Tuesday morning report. “Today’s forecast is warmer over the East. The Northwest and south-central U.S. are cooler. CONUS PWCDDs are up 1.7 to 63.8 for the period.”

Technical analysts and students of seasonality see the $1.611 low of March as a long-term cycle low, and typically natural gas will make a seasonal advance into May and then decline into summer. That dynamic, however, is under study. “My working assumption has been that the $1.611 low and its 11% bulls (Market Vane) was the 15-year cycle low for natgas,” said Walter Zimmermann, vice president at United ICAP. “The issue right now is whether we get a spring to fall decline.

“My pivotal resistance for a spring peaking range consists of two numbers. The $2.865 is <A> = <C> for an ABC up off the $1.611 low. And $3.480 is the resistance line down off the $13.694 high,” he said in closing comments Monday.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 1532-1231 | ISSN © 2577-9877 |