NGI Data | NGI All News Access

Darkest Just Before Dawn? Weekly NatGas Up 19 Cents

For a market mired in layoffs, bankruptcies and diminishing capital expenditures, weekly natural gas prices provided something of a breath of fresh air. For the week ended March 18, theNGI Weekly Spot Gas Average rose a solid 19 cents from last week’s dismal $1.46 to $1.65, and every U.S. point followed by NGI gained at least a dime.

Points in the Northeast proved to be the week’s biggest gainers, with deliveries to Algonquin Citygate rising 84 cents to $2.03, followed closely by Tennessee Zone 6 200 L with an advance of 71 cents to $1.98. The location showing the smallest gain was Texas Eastern M-2 Delivery with an improvement of 10 cents to $1.80.

Regionally, the Northeast proved to be the biggest winner, with an average gain of 32 cents to $1.44 and California points found themselves in the caboose with average gains of 12 cents to $1.74.

The Rocky Mountains and Midcontinent were able to rise 15 cents on average to $1.54 and $1.65, respectively. South Texas added 16 cents to $1.73.

South Louisiana and the Midwest mustered gains of 17 cents to $1.74 and $1.83, respectively. East Texas rose 19 cents to $1.75.

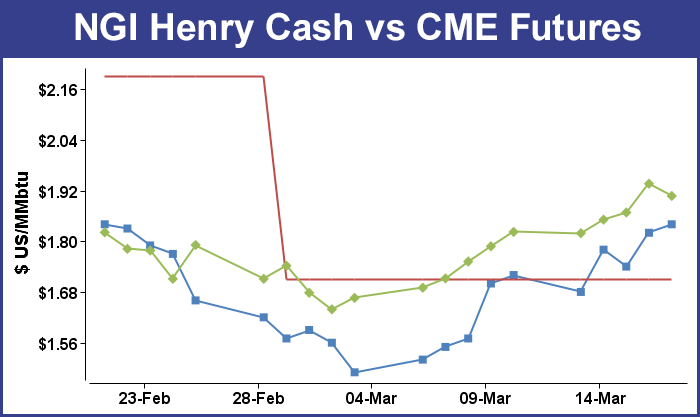

April futures rose 8.5 cents for the week to $1.907 and much of that came from the Energy Information Administration (EIA) inventory report Thursday showing a withdrawal of 1 Bcf, slightly less than what traders were expecting. When EIA released its number, futures prices initially slipped. At the close, however, April had managed to add 6.8 cents to $1.936 and May gained 5.6 cents to $2.011.

The release of storage data wasn’t much of a surprise. The 1 Bcf withdrawal was about with traders were expecting. The market dropped to a low of $1.855 following the release of the data. and by 10:45 a.m. April was trading at $1.857, down 1.1 cents from Wednesday’s settlement.

“We were looking anywhere from a +6 Bcf to a -2 Bcf number said a New York floor trader. “We’ll see if the market can hold the $1.83 to $1.84 area.”

“The 1 Bcf net withdrawal was slightly less than the consensus expectation and so modestly bearish in terms of its immediate pressure on prices,” said Tim Evans of Citi Futures Perspective. “We see it as significantly more bearish versus the 82-Bcf five-year average, with the year-on-five-year average storage surplus a new high of 807 Bcf.”

Drew Wozniak of ICAP Energy characterized the report as “bearish.”

Inventories now stand at 2,478 Bcf and are a stout 998 Bcf greater than last year and 807 Bcf more than the five-year average. In the East Region 12 Bcf was pulled, and the Midwest Region saw inventories fall by 10 Bcf. Stocks in the Mountain Region rose 1 Bcf, and the Pacific Region was higher by 1 Bcf. The South Central Region added 19 Bcf.

During Friday’s trading, natural gas for weekend and Monday delivery was in demand as a late-winter cold blast ignited buying interest along with higher power prices and hefty increases in expected power loads.

All but two points followed by NGI recorded gains ranging from a few pennies to a nickel or more, but several eastern locations went deep into double-digit gains. The NGI National Spot Gas Average gained 6 cents to $1.77, and eastern points, on average, jumped more than 30 cents. Futures ended on a weak note, with April giving up 2.9 cents to $1.907 and May retreating 2.2 cents to $1.989.

A trifecta of higher power prices, below-normal temperatures, and forecast higher power loads all combined to send weekend and Monday packages sharply higher. Intercontinental Exchange reported that Monday on-peak power at ISO New England’s Massachusetts Hub jumped $12.97 to $36.97/MWh, and at the PJM West terminal on-peak power Monday rose by $11.74 to $37.43/MWh.

Gas for weekend and Monday delivery at the Algonquin Citygate jumped 85 cents to $3.10, and deliveries to Iroquois, Waddington gained 20 cents to $2.19. Parcels on Tenn Zone 6 200L also added 78 cents to $2.95.

In the Mid-Atlantic buyers were also active. Gas on Tetco M-3 delivery rose by 11 cents to $1.38, and gas bound for southeastern-most Pennsylvania as well as southern New Jersey and Trenton on Transco non New York North posted a stout 64 cent gain to $2.05.

Major hubs sported steady to higher quotes also. Gas at the Chicago Citygate added 4 cents to $1.95, and gas at the Henry Hub rose 2 cents to $1.84. Gas on El Paso Permian changed hands up a penny at $1.65, and packages priced at the SoCal Border Avg. Average were quoted 3 cents higher at $1.70.

Temperatures over the weekend in the East and Midwest were forecast to visit below-normal levels not seen in close to two weeks. AccuWeather.com predicted that the high in New York City Friday of 59 would drop to 36 Sunday before reaching 44 Monday, 7 degrees below normal. Chicago’s 43 Friday high was seen easing to 41 Sunday before adding a degree to 42 Monday, still 6 degrees below normal.

Sunday power loads were also predicted to rise above Friday loads. ISO New England forecast peak power load Friday of 14,480 MW would rise to 15,330 MW Sunday. PJM Interconnection expected peak load Friday of 29,748 MW to climb to 33,820 MW Sunday.

Jim Ritterbusch of Ritterbusch and Associates sees an improving supply-demand balance. “The ability of this market to advance in the face of a seemingly neutral EIA storage report attests to some significant chart improvement that was accommodated by some apparent bullish spillover from yesterday’s upside acceleration in the oil futures,” he said in a Friday note to clients. “As the US economy could expect additional improvement off of what appears to be a continued low rate environment through the rest of this year, some improvement in the industrial segment of the natural gas consumption pie is likely being priced in.

“With the weather factor driving much of the weekly shifts in gas prices, the gas market’s status as an industrial commodity is often ignored. But with the arrival of the shoulder period, non-weather related factors will be acquiring greater focus. In addition to a potential lift in industrial offtake, it would appear that production will be exhibiting some long awaited response to a sub $2 pricing environment. Along with this development, ongoing shifts on the demand side are also likely sustainable as coal usage by the utilities continues to get displaced by the comparatively low priced gas market.

For the moment, Ritterbusch is keeping a close eye on technical factors. “[P]iecing together additional price gains in April futures to above the $2 mark during the next week and half will prove challenging. Nonetheless, we will defer to yesterday’s down trend line violation that could accommodate a test of the $2 mark with only limited assistance from cooler temperature views that are now being generally expected across the final week of this month.”

Gas buyers for power generation across the MISO footprint will likely have to be on their toes as significant wind generation may not be in the cards until early next week. “A pair of weak disturbances and a deepening upper-level trough will allow seasonably cool conditions to become more widespread by the end of the week through the weekend,” said WSI Corp. in a Friday morning report.

“Widely scattered snow and rain showers are possible. High temps will retreat into the 30s and 40s north; 50s and 60s south. A south-southwest flow will develop early next week around fleeting high pressure and a wave of low pressure along the Canadian border. This will lead to a sharp warming trend and the return of above-average spring warmth by Tuesday. Highs may generally warm in the 50s, 60s and 70s.

“Relatively light wind generation is expected today into the weekend. A southerly wind will cause wind gen to ramp up early next week with the potential for output to exceed 10 GW.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |