E&P | NGI All News Access | NGI The Weekly Gas Market Report | Permian Basin

Permian Pure-Play Concho Cuts 2015 Spending by One-Third

Midland, TX-based Concho Resources Inc. (CXO) cut its 2015 capital spending plans to $2 billion from $3 billion due to low commodity prices and projected 16-20% year-over-year production growth. Analysts following the company gave the news a thumbs-up and praised the Permian Basin producer for its “capital discipline.”

Previous guidance anticipated 2015 production growth of 28-32%. Capital spending last year is estimated at $2.6 billion, generating 20%-plus production growth.

“While this is a meaningful cut to growth, the updated budget does imply a modest improvement in capital efficiency ($38,000 per boe/d versus $45,000 boe/d), which we think is more due to high-grading than assumed service cost reductions…” said BMO Capital Markets analyst Phillip Jungwirth.

“Reducing the capital program while delivering robust growth reflects our commitment to a strong balance sheet and highlights the quality of our assets in the Permian Basin,” said Concho CEO Tim Leach. “In the current environment, we intend to prudently manage our 2015 capital program around anticipated cash flows and retain significant flexibility to scale our activity level up or down depending on service costs and commodity prices.”

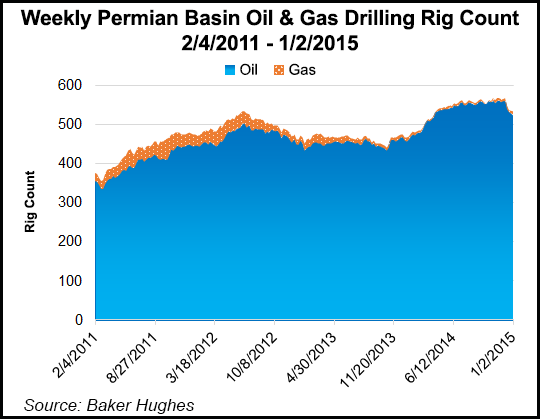

The 2015 program includes about $1.8 billion for drilling and completions and about $200 million for facilities, midstream and other capital. Concho plans to spend $1.3 billion on drilling and completions in the Delaware Basin, about $300 million in the Texas Permian and about $200 million in the New Mexico Shelf. The company is running 36 drilling rigs and expects to average 30 rigs in the first quarter and about 25 rigs beginning in the second quarter through year end. The 2015 capital program excludes acquisitions and could change due to economic and industry conditions, Concho said after the market closed Monday.

BMO has an “outperform” rating on Concho shares. Analysts at Tudor, Pickering, Holt & Co. said they “like the capital discipline” they see at the company. Wells Fargo Securities also has an “outperform” rating on Concho. Analysts Gordon Douthat and David Tameron wrote that they expect Concho to outspend cash flow by about $400 million this year, assuming $60/bbl for West Texas intermediate.

“Relative to the industry and its oilier peers, we believe the 15-20% growth target for $400 million outspend will stack up very favorably,” Douthat and Tameron said in a note Tuesday. “For those wanting exposure to E&P, CXO remains one of our favorites.”

Wunderlich Securities analyst Irene Haas has a “hold” rating on Concho and noted that less spending means lower borrowing this year, with end-of-2015 debt now expected to be $34/share versus Wunderlich’s prior estimate of $42/share. Wunderlich raised its net asset value and price target to $89 from $81 for Concho shares.

According to a just-released investor presentation, Concho has 1.2 million (605,000 net) acres in the Permian Basin with about 22,000 drilling locations and 3 billion boe of resource potential.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1266 | ISSN © 2158-8023 |