NGI Data | NGI All News Access

Short Trading Week Breathes Life Into The Bulls

For the holiday-shortened trading week, bulls managed to gain the upper hand and prices rose by double digits at most locations. Only one market point outside the typically volatile Northeast endured a loss, and the NGI Weekly Spot Gas Average rose a robust 36 cents to $2.96.

Of the actively traded points, Algonquin Citygates stood a top the leader board with a $3.77 rise to $6.76 followed by Dracut with a gain of $2.65 to $6.11. At the other end of the scale another northeast point, Texas Eastern M2 30 Delivery, fell the most, giving up 38 cents to $2.43. Not far behind were Tennessee Zone 4 Marcellus dropping 21 cents to 90 cents and Transco Leidy shedding 20 cents to 93 cents. Regionally, the Midwest was seen with the smallest gain, adding 13 cents to $3.12, and the Northeast piled up the greatest yardage with a rise of 73 cents to $2.74.

South Louisiana gained 14 cents to $2.95 and South Texas, East Texas and California all posted 20 cent advances to $2.91, $2.92, and $3.21, respectively.

The Rocky Mountains added 29 cents to $3.07 and the Midcontinent rose by 32 cents to $3.07 as well.

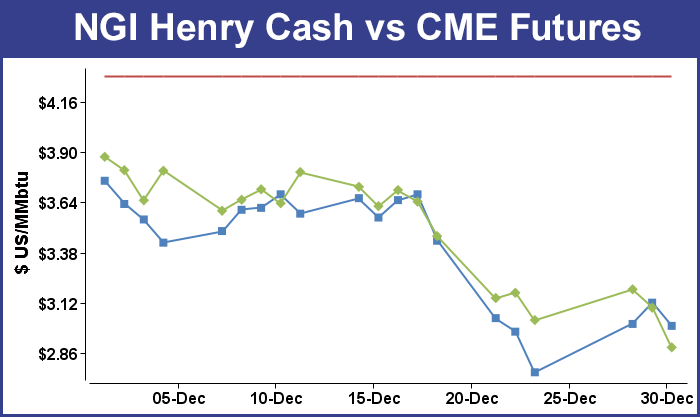

February Futures were off by 9.1 cents to $3.003 and futures bulls took a broadside Wednesday in the form of an inventory report that showed a much leaner withdrawal than what traders were expecting. The Energy Information Administration (EIA) reported a decrease of 26 Bcf in its 12:00 p.m. EST release, about 14 Bcf less than estimates. February sank to a low of $2.987 after the number was released and by 12:15 a.m. February was trading at $3.032, down 6.2 cents from Tuesday’s settlement. Things only got worse from there. At the close, February had dropped 20.5 cents to $2.889, and March was off 20.0 cents to $2.896.

Prior to the release of the data, analysts were looking for a decrease of about 40 Bcf. IAF Advisors analysts calculated a 30 Bcf decline, and Citi Futures Perspective analysts figured on a 43 Bcf pull. Ritterbusch and Associates was looking for a 48 Bcf withdrawal.

The price tumble was expected, but “a close below $3 is going to be necessary for a new price regime to stick,” a New York floor trader said shortly after the storage report.

Tim Evans of Citi Futures Perspective said the reported “suggest[ed] either a further increase in production or a larger-than-anticipated drop in demand related to the Christmas holiday. It certainly reinforces the dominant bearish sentiment.”

Others saw the undersized storage report Wednesday as sending the bulls into the new year battered and beleaguered. “Although the EIA storage report prompted a brief downward response, it has been easily overshadowed by some ongoing shifts in the short-term temperature views,” said Jim Ritterbusch of Ritterbusch and Associates in closing comments Wednesday.

“Outlooks are becoming mixed but generally suggestive of smaller cold deviations from normal than had been anticipated at the beginning of this week. Short of a significant shift in the weather forecasts over the holiday, this market appears poised for slippage back to a $2 handle by week’s end with eventual declines likely to the $2.75 area.

Ritterbusch commented that the “26 Bcf withdrawal compared with average industry ideas for about a 41 Bcf decline. Although the figure was unable to maintain value south of the $3 mark [initially], the much smaller than expected decline continued to underscore strong supply side dynamics in the form of near record production and easing import availability. Overall, we are suggesting a bearish trading stance, but given the vagaries of the weather views at this time of the year, we will suggest awaiting price advances in March futures to the $3.25 area before establishing short holdings.”

Inventories now stand at 3,220 Bcf and are 232 Bcf greater than last year and 81 Bcf below the five-year average. In the East Region 29 Bcf was withdrawn and the West Region saw inventories stay flat. Stocks in the Producing Region rose by 3 Bcf.

In Friday’s trading physical gas for weekend and Monday delivery was largely mixed as strength at New England, Gulf and Midcontinent locations was able to outmuscle weakness in the Marcellus and Rockies. The overall market gain was 10 cents.

Futures made a counter intuitive advance as traders covered short positions after the market exhibited opening strength. At the close, February had added 11.4 cents to $3.003 and March was higher by 10.3 cents to $2.999.

Weekend and Monday gas in the Midcontinent posted gains well above the national average as peak power rose sharply and weather forecasts called for temperatures well below average. Forecaster Wunderground.com predicted the high Friday in Oklahoma City of 37 degrees would hold Saturday before easing to 35 by Monday, 14 degrees below normal. Dallas was expected to see its Friday high of 39 reach 50 on Saturday before falling to 41 on Monday. The normal early January high in Dallas is 56.

Gas on Northern Natural Ventura added 43 cents to $3.49, and deliveries to OGT gained 11 cents to $3.00. Gas on Panhandle Eastern added 18 cents to $3.04, and packages on NGPL Midcontinent Pool rose by 8 cents to $3.00.

The National Weather Service (NWS) in Fort Worth, TX, predicted that the early weekend warmth for North Texas would quickly recede in front of cold air. “The warmer temperatures will be short-lived as a strong cold front moves into the region Saturday night in the wake of the departing upper-level low. Winds will increase to 15 to 25 miles per hour with temperatures falling in the 20s and 30s by daybreak Sunday,” NWS said.

“This will put wind chills in the teens and 20s Sunday morning. Highs Sunday will only reach the middle 30s northwest to middle 40s southeast…despite clearing skies and afternoon sunshine. Winds diminish after sunset…and clear skies and dry air will allow temperatures to plummet into the middle teens in the typically cooler outlying locations to the middle 20s in urban areas.”

IntercontinentalExchange reported that Monday peak power at ERCOT N rose $10.58 to $39.50/MWh.

Gulf prices were modestly higher. Gas on Transco Zone 3 fell a penny to $2.99, and deliveries to the Henry Hub were down a penny at $2.99. Parcels on ANR SE gained 4 cents to $2.97, and deliveries on Tennessee 500 L added a penny to $2.96. Gas at Katy came in 5 cents higher at $3.02.

Gas at eastern points was mixed to higher. Weekend and Monday deliveries to the Algonquin Citygates rose $1.80 to $7.66, and deliveries to Iroquois Waddington added 44 cents to $3.97. Gas on Millennium was down a penny at $1.21.

Gas on its way to New York City on Transco Zone 6 retreated 5 cents to $3.11, but parcels on Tetco M-3 added 24 cents to $1.97.

The 11-cent rise in futures caught a number of traders off guard. “A lot of guys went home short from Wednesday and the market settled way below $3 at $2.889. Volume in the February contract [Friday] was over 91,000 [109,000], and that is pretty good for the day after New Years,” said a New York floor trader.

“Everybody was confused as to why this market was up so much today since we are supposed to have highs here in the 60s by Sunday. This market opened higher this morning, and a lot of guys may have decided to cover. There’s always something going on in this market.”

Weather forecasts turned colder overnight Thursday for major population centers. WSI Corp. in its Friday morning report showed the entire eastern half of the country at below or much below normal temperatures with the exception of Florida. “[Friday’s] six-10 day period forecast is colder than previous forecasts over the eastern two-thirds of the nation due in part to model trends and the period shift. Confidence in the forecast is average today as medium-range models are in reasonably good agreement with the large-scale pattern most of the period.”

Risks to the forecast include greater cold “across the eastern two-thirds of the nation, especially early in the period. SoCal and the Southwest may run a bit warmer.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |