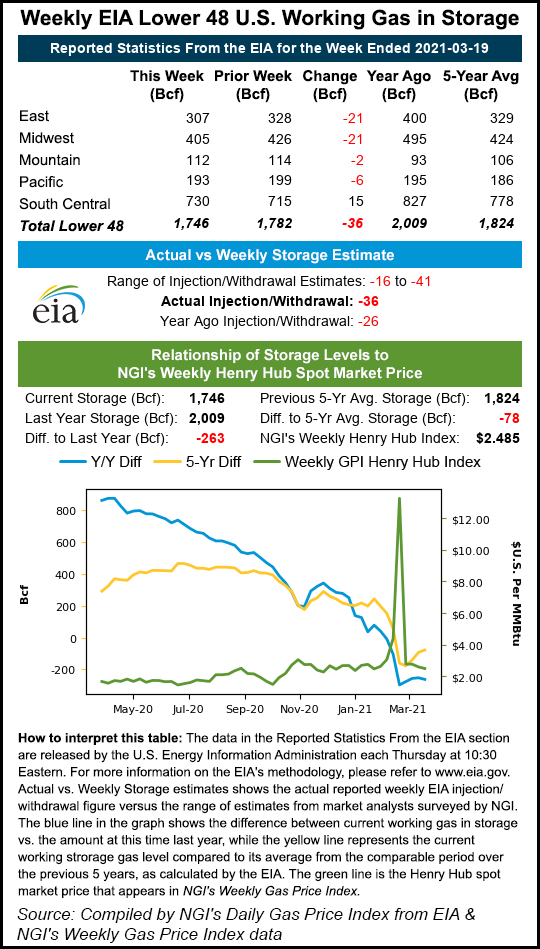

The U.S. Energy Information Administration (EIA) on Thursday reported a withdrawal of 36 Bcf from natural gas storage for the week ending March 19. The pull was steeper than market expectations, boosting Nymex futures.

“It was cooler than normal over areas of the West, Plains and New England” during the EIA report period, according to NatGasWeather, which had forecast a 28 Bcf pull.

Power burns strengthened and liquefied natural gas export levels were also solid during the week.

Ahead of the EIA report, the April contract was up 1.1 cents to $2.529/MMBtu, and the prompt month jumped to around $2.559 when the EIA data was released at 10:30 ET. About 30 minutes later, the April contract was up to $2.566, ahead 4.8 cents day/day.

The latest draw marked the first EIA...