Markets | NGI All News Access | NGI The Weekly Gas Market Report | Permian Basin

Permian Dealmaking Leads 1Q Worldwide Transactions, Led by Concho-RSP Merger

Supported by U.S. dealmaking in the Permian Basin, global upstream transactions hit $32 billion in the first quarter, according to oil and gas information provider 1Derrick.

Merger and acquisition (M&A) deal value in 1Q2018 was less than half the record-setting pace set in 1Q2017, when an estimated $63 billion in transactions were announced.

U.S. deal value has been the beneficiary of recent transactions, rebounding in the first quarter to $22 billion following a weak $19 billion for the second half 2017. In contrast, international deal values excluding the United States reached only $10 billion in the first quarter, down from $38 billion a year ago.

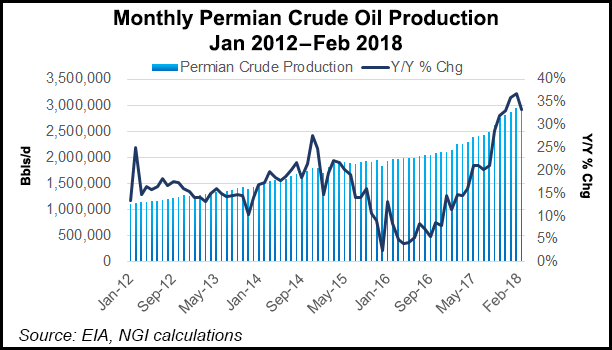

The biggest transaction was at the tail end of the quarter, the $9.5 billion mega-merger announced between Permian pure-plays Concho Resources Inc. and RSP Permian Inc.

The Concho transaction was “the largest U.S. corporate deal since 2012 and the largest-ever Permian transaction,” said 1Derrick COO Mangesh Hirve. “After a three-quarter hiatus following $39 billion in deals in 3Q2016 through 1Q2017, M&A activity is once again heating up in Permian, the premier U.S. resource play. In contrast, international activity slowed down dramatically across all regions, with no single deal exceeding $1 billion.”

Three U.S. transactions between January and March exceeded $1 billion, topped by the blockbuster Concho/RSP deal. The second largest domestic deal was by TPG Pace Energy Holdings Corp., led by former Occidental Petroleum Corp. CEO Stephen Chazen, which in March bought EnerVest Ltd.’s Eagle Ford Shale assets worth $2.66 billion. TPG and EnerVest also have formed South Texas pure-play Magnolia Oil & Gas Corp.

The No. 3 U.S. deal, worth $1.15 billion, was by private equity-backed Admiral Permian Resources LLC, which purchased Permian Delaware sub-basin property from Riverstone-backed Three Rivers Operating III.

“Public companies accounted for 15 divestitures in the top 20 U.S. deals, with private equity funded firms acquiring 40% of these assets,” according to 1Derrick.

Other buyers of domestic assets included two by international firms. South Korea’s SK Innovation Co. Ltd. purchased Oklahoma properties for an estimated $300 million, while Australia-listed Sundance Energy Australia Ltd. spent $222 million to bolt-on Eagle Ford acreage.

“Overall, Permian deals dominated the quarter, with nine transactions accounting for nearly two-thirds of the total top 20 value,” said 1Derrick.

Concho’s purchase of RSP Permian to become the largest unconventional oil and gas producer in the Permian has spurred widespread speculation that the massive deal will trigger a wave of corporate consolidation in the region.

“We believe this is a landmark transaction, where RSP Permian’s acreage, built up through multiple transactions since 2014, is contiguous to Concho’s and will generate an estimated $2 billion net present value in synergies,” Hirve said. “ It is the search for these synergies that will drive further consolidation in the play.”

“Private equity-backed firms and publicly traded companies provide a plethora of Permian consolidation opportunities,” according to 1Derrick. The firm’s private equity database lists 130 firms operating in the Permian, including 72 that have received a total of $13.2 billion in equity commitments from the top eight investment firms.

Oil prices may have stabilized in the $60/bbl range this year, but exploration and production (E&P) valuations have fallen almost 20% from December 2016 highs.

“The lower equity valuations provide opportunities for acquisitions among the more than 35 publicly traded E&Ps which will produce 1 million boe or more in the Permian in 2018,” 1Derrick noted.

The largest international transaction tracked by 1Derrick during 1Q2018 was Mubadala Investment Co.’s $934 million purchase from Eni SpA to acquire a 10% interest in Egypt’s Zohr natural gas field.

The oil majors participated in seven of the top 20 transactions during the first quarter. Included where divestitures by Royal Dutch Shell plc in Thailand, New Zealand and Iraq, which accounted for about $2 billion, or nearly 20% of the quarterly International deal value. Total SA also acquired an interest in the Waha concession in Libya, while selling small interests in Canada and Norway.

The “key driver” in the plunge in international activity was lower Canadian oilsands deal flow, which fell to $1.1 billion from $24.4 billion year/year, and in North Sea, where deals fell to $68 million from $5.3 billion.

“However, we expect international M&A to rebound through 2018, driven by the $10-11 billion in North Sea assets and $6-7 billion in Canadian oilsands assets that are currently on the market,” said Hirve. Already this month, U.S.-based Harbour Energy Ltd., backed by EIG Global Energy Partners, has made a $13 billion bid to acquire Australia’s Santos Ltd.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1266 | ISSN © 2158-8023 |