Another Nor’Easter Lifts Weekly Natural Gas Prices; Futures Struggle for Upward Momentum

Yet another March nor’easter delivered a late-winter boost to spot prices throughout the Northeast and Mid-Atlantic for the week ended Friday, though results were mixed across other regions. The NGI Weekly Spot Gas Average added 12 cents to $2.68/MMBtu.

Points in New England posted the biggest gains for the week as winter weather swept through the region. A brief electric transmission outage during the week also caused a significant spike in power prices and pushed more burden onto gas-fired generation in the ISO New England market, according to analysts.

Algonquin Citygate surged $2.42 for the week to average $6.11, while Maritimes & Northeast jumped $2.75 to $7.28.

Further south, Transco Zone 5 finished higher on the week, climbing 7 cents to $2.95, while in Appalachia, Tetco M3 Delivery climbed 18 cents to $2.91.

In the West, SoCal Citygate had an up-and-down week. Prices surged early in the week amid expectations for higher demand and an announcement of maintenance affecting imports through Southern California Gas Co.’s (SoCalGas) Southern Zone. Prices later moderated as SoCalGas took steps to ease ongoing constraints on imports and storage.

SoCal Citygate finished 99 cents higher for the week at $3.80. SoCal Border Average finished 3 cents higher at $2.34.

Further upstream, prices fell. In the Rockies, Transwestern San Juan dropped 16 cents to $1.86, while in West Texas El Paso Permian tumbled 19 cents to $1.76.

Natural gas futures inched higher Friday after selling off by more than a dime over the previous two sessions, as a mixed late-winter outlook failed to spark any upward momentum. The April contract settled at $2.688 Friday, a 0.7 cent gain on the day but down from $2.732 the Friday before.

“Natural gas prices traded in an extremely narrow range Friday, with the prompt month trying to break higher on colder risks in the long-term but later contracts holding it back through much of the day,” Bespoke Weather Services said after the close. “Later contracts finally caught a bit of a bid into the final hour of the day, with the prompt month accordingly rallying slightly from there, but overall activity was limited.

“We head into the weekend still seeing prices fairly valued at these levels,” as the week’s Energy Information Administration (EIA) storage data “slightly lowered the ceiling in the range we had been eyeing,” Bespoke said. In the upcoming week, “we would expect a range from generally $2.65-2.75 to win out unless there are significant differences in modeling guidance over the weekend…weather should remain supportive into next week, with a more impressive EIA print eyed.”

NatGasWeather.com said Friday’s midday Global Forecast System data trended colder for a “weather system and cold shot across the east-central U.S.” for the upcoming week, “but still showing a mild ridge over the southern and eastern U.S. March 24-26 for lighter demand.

“Finally, it was milder trending on the amount of cold arriving into the eastern U.S. March 27-30,” likely leading markets to view the run as milder trending overall, according to the firm.

“There are risks over the weekend between colder and milder trends, but the onus is solidly on the colder camp gaining momentum if any sort of sustained rally is to be expected,” NatGasWeather said.

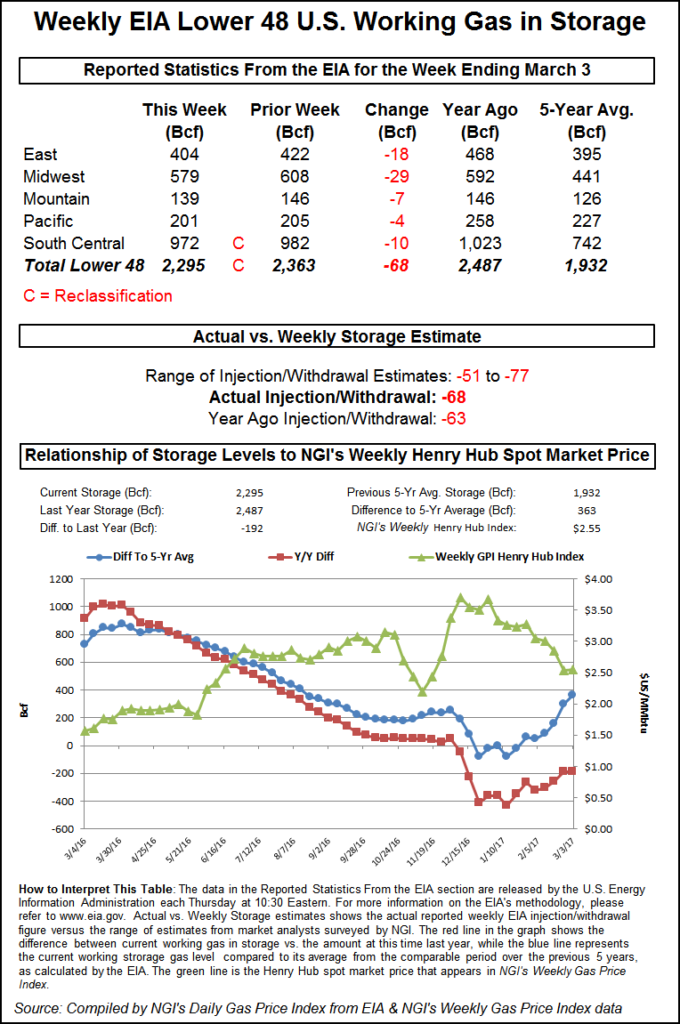

On Thursday EIA reported a 93 Bcf withdrawal from U.S. gas stocks for the week ending March 9, tighter than the 55 Bcf withdrawn a year ago and close to the five-year average withdrawal of 97 Bcf. The number missed to the bearish side of expectations, prompting April to slide 5.0 cents during Thursday’s session.

Prior to Thursday’s report, the market had been looking for a withdrawal slightly tighter than the actual number.

A Reuters survey of traders and analysts had on average predicted a 96 Bcf withdrawal, with responses ranging from -86 Bcf to -107 Bcf. OPIS analysts had predicted a 96 Bcf withdrawal, citing higher demand from the recent winter weather in the Northeast. Stephen Smith Energy Associates had forecast a 99 Bcf draw, while Kyle Cooper of IAF Advisors had called for a 101 Bcf withdrawal.

Total working gas in underground storage in the Lower 48 ended the week at 1,532 Bcf, versus 2,250 Bcf a year ago and five-year average inventories of 1,828 Bcf. The year-on-year storage deficit increased week/week from -680 Bcf to -718 Bcf, while the year-on-five-year deficit narrowed slightly from -300 Bcf to -296 Bcf, EIA data show.

By region, the largest withdrawal came in the East region at 45 Bcf, while 30 Bcf was pulled in the Midwest. The South Central region saw a 6 Bcf withdrawal for the week, 3 Bcf from salt and 3 Bcf from nonsalt. In the Pacific, 8 Bcf was withdrawn, while 4 Bcf was withdrawn in the Mountain region, according to EIA.

Analysts with Tudor, Pickering, Holt & Co. (TPH) said the bearish miss implies “a less dramatic shift in weather-adjusted undersupply versus expectations — we now sit at 2.5 Bcf/d undersupplied versus” previous estimates of more than 3 Bcf/d. “Though the classic March 15 warning should have alerted us to an impending storage disappointment, Henry Hub traded 2% lower on the day as the market continued the trend of persistent undersupply.

“Overall inventory levels have broken free from five-year minimums and are beginning to close the gap toward normal levels, though March’s late cold snap could bring larger than normal draws,” the TPH analysts said. “Early storage estimates for next week are calling for draws twice as large as norms of -50 Bcf given severe weather in the Northeast and widespread colder-than-normal temperatures across much of the U.S.”

The Desk’s Early View storage survey showed 14 respondents on average estimating EIA will report an 88.3 Bcf withdrawal from U.S. gas stocks for the week ending March 16. Responses ranged from -68 Bcf to -108 Bcf. Last year, 137 Bcf was withdrawn during the period, and the five-year average is a withdrawal of 53 Bcf.

Analysts with Jefferies LLC said Thursday they expect Lower 48 inventories to exit March at around 1.4 Tcf.

“Storage is likely to enter the refill season around 33% below last year, when storage volumes never dipped below 2 Tcf,” the Jefferies analysts said. “In 2017, 1.7 Tcf was injected into storage to reach 3.8 Tcf by the end of October, roughly in-line with the five-year average. In order to reach 3.8 Tcf of storage prior to Oct. 31, the U.S. will need to inject around 3 Bcf/d more in storage than 2017 injections.”

The market will have more production to tap as injection season ramps up, according to Jefferies.

“After production growth flattened in the back half of February, it has moved slightly higher in March, averaging 77.6 Bcf/d month-to-date, up 0.3 Bcf/d from the prior month average,” the analysts said. “Supply has now gained around 4.2 Bcf/d since October 2017 and is up 6.2 Bcf/d year/year. Northeast production has averaged 27.1 Bcf/d in March month-to-date, in-line with the December 2017 record high.

“Total demand is up 8.4 Bcf/d year/year and down only 3.3. Bcf/d sequentially. The year/year demand increase has been driven by higher residential/commercial (res/com) demand,” up 4.4 Bcf/d, as well as liquefied natural gas (LNG), up 1.5 Bcf/d, power generation, up 1.3 Bcf/d, industrial, up 0.6 Bcf/d, and exports to Mexico, up 0.4 Bcf/d, according to the firm.

“Market sentiment remains inconsistent,” Societe Generale analyst Breanne Dougherty said in a note to clients Thursday. “After solid gains in price early this week due to a constructive weather outlook through the end of March, indications of a slightly less cold outlook in the last couple days and a bearish storage report Thursday morning prompted retreat. The front-month is now back under $2.70 after reaching $2.80 only a few days ago.

“As for us, our near-term view has held more steady than market sentiment,” Dougherty said. “…We are bullish in the near term with our forecast for the second quarter at $2.89, versus the forward market’s $2.71; third quarter at $3 versus the forward market’s $2.82; and fourth quarter at $2.98 versus the forward market’s $2.90. We recommend looking at dips, like Thursday’s, for entry into long positions on core summer 2018 and first quarter 2019 contracts given their potential for distinct upside pressure.”

In the spot market Friday, weekend deals traded lower across most regions amid declining Lower 48 demand, although a few points in New England and California bucked the trend; the NGI National Spot Gas Average declined a nickel to $2.65/MMBtu.

U.S. demand Friday measured “marginally higher at best, moving just above 77.5 Bcf on the day,” OPIS analyst Luke Larsen said in a note to clients. “…The forecast calls for a Saturday-Sunday average of 74.77 Bcf/d and the following work week to average 77.35 Bcf/d. This would be a decline from the 80.3 Bcf/d for the current Monday through Friday period, or down about 2.95 Bcf/d.”

In the firm’s one- to five-day forecast outlook, OPIS analyst Alan Lammey on Friday called for a “forecast mean population-weighted temperature of about 48.4 degrees, which is 0.8 degrees colder than normal. Natural gas demand will remain somewhat elevated as temperatures cool across the upper Midwest and the Northeast.

“The daytime high in Washington, DC, will peak near 50 degrees heading into the weekend, while New York City and Boston will struggle to break above 40 degrees, all of which is upwards of 10 degrees colder than the historical averages,” according to Lammey.

Several points in the Northeast worked their way higher Friday, including Algonquin Citygate, up 25 cents to $7.62, and Transco Zone 6 New York, up 3 cents to $2.84.

Meanwhile, wintry precipitation moving through the north-central United States wasn’t enough to lift prices in the Midwest and Midcontinent Friday.

A storm system over the central to northern Plains was expected to “produce a wintry mix” before moving east into Saturday morning, the National Weather Service said Friday. “Rain, sleet and freezing rain are expected from Iowa into northern Illinois and east-southeastward into West Virginia Saturday morning. The largest hazard from this system is expected to be ice accumulation, with perhaps greater than 0.1 inch accretion in a few locations, while snowfall accumulations should remain light.”

Genscape Inc. was forecasting Midwest demand to decline through the weekend to 12.84 Bcf/d by Sunday, down from 14.18 Bcf/d Friday. The firm’s Midcontinent regional forecast called for demand to total 2.36 Bcf/d Sunday, down from just under 3 Bcf/d Friday.

Chicago Citygate tumbled 9 cents to average $2.45, while Northern Natural Ventura gave up 13 cents to $2.32. In Appalachia, Dominion South eased 4 cents to $2.45.

In the West, SoCal Citygate climbed 20 cents to $3.44 as Southern California Gas Co. (SoCalGas) was calling for demand to rise through the weekend. SoCalGas was forecasting total system demand to increase to around 3 Bcf/d Saturday through Monday, up from demand of around 2.7-2.9 Bcf/d Thursday and Friday.

Maintenance work affecting imports through SoCalGas Southern Zone contributed to volatility at SoCal Citygate during the week. On Friday, the utility announced that capacity through the Southern Zone would be lowered to 700 MMcf/d through the weekend and increased to 800 MMcf/d on Monday. According to Genscape, the Southern Zone’s normal operational level is 1,256 MMcf/d.

Elsewhere in California, SoCal Border Average gave up 24 cents to average $2.06. Further upstream, El Paso S. Mainline/N. Baja dropped 13 cents to $2.15, while El Paso Permian tumbled 17 cents to $1.58.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |