U.S. Oil Projected to Fill 80% of Global Demand Growth Over the Next Three Years

Oil production growth led by the United States, Brazil, Canada and Norway will keep the world well oiled through 2020, but investments are needed to boost output in the longer term, the International Energy Agency (IEA) said Monday.

Gains from the United States alone are predicted to cover 80% of global demand growth in the next three years, with Canada, Brazil and Norway covering the remaining demand, according to “Oil 2018.”

The global energy watchdog’s latest annual report was unveiled in Houston by IEA Executive Director Fatih Birol on the opening day of CERAWeek by IHS Markit.

“The United States is set to put its stamp on global oil markets for the next five years,” said Birol. “But as we’ve highlighted repeatedly, the weak global investment picture remains a source of concern. More investments will be needed to make up for declining oilfields.

“The world needs to replace 3 million b/d of declines each year, the equivalent of the North Sea, while also meeting robust demand growth.”

Global oil production capacity is forecast to grow by 6.4 million b/d and reach 107 million b/d by 2023.

“Thanks to the shale revolution, the United States leads the picture, with total liquids production reaching nearly 17 million b/d in 2023, up from 13.2 million b/d in 2017,” according to IEA. “Growth is led by the Permian Basin, where output is expected to double by 2023.”

In its flagship publication,World Energy Outlook-2017 issued last fall, IEA said resilient shale and tight resources production had cemented the United States as the biggest producer in the world.

The path to carry U.S. crude to world markets “looks clear,” driven by expansions in Texas, said researchers in the new report. Because of investments in pipelines and other infrastructure to ease the current bottlenecks, domestic crude export capacity is forecast to hit nearly 5 million b/d by 2020.

The South Texas port area anchored by Corpus Christi, home to a gaggle of proposed oil, petrochemical and liquefied natural gas (LNG) projects, “solidifies its position as the primary North American crude-oil outlet” over the five-year forecast, IEA said.

The Port of Corpus Christi’s strategic goals include providing surface infrastructure and services in support of maritime and industrial development. The port, a gateway to Mexico and other Latin American ports, is the fourth largest in the United States in total tonnage.

A long list of expansion projects has been proposed for the Corpus Christi region, including the newly announced Cactus II Pipeline sponsored by Plains All American Pipeline LP, which would connect Permian oil to South Texas.

Last year, ExxonMobil Corp. and Saudi partner Saudi Basic Industries Corp. agreed to develop a world-class ethane steam cracker near Corpus, which if given final approval would be able to produce 1.8 million metric tons/year of ethylene. Cheniere Energy Inc. is also advancing plans to export LNG from a new terminal near Corpus, with the first train ready in 2019.

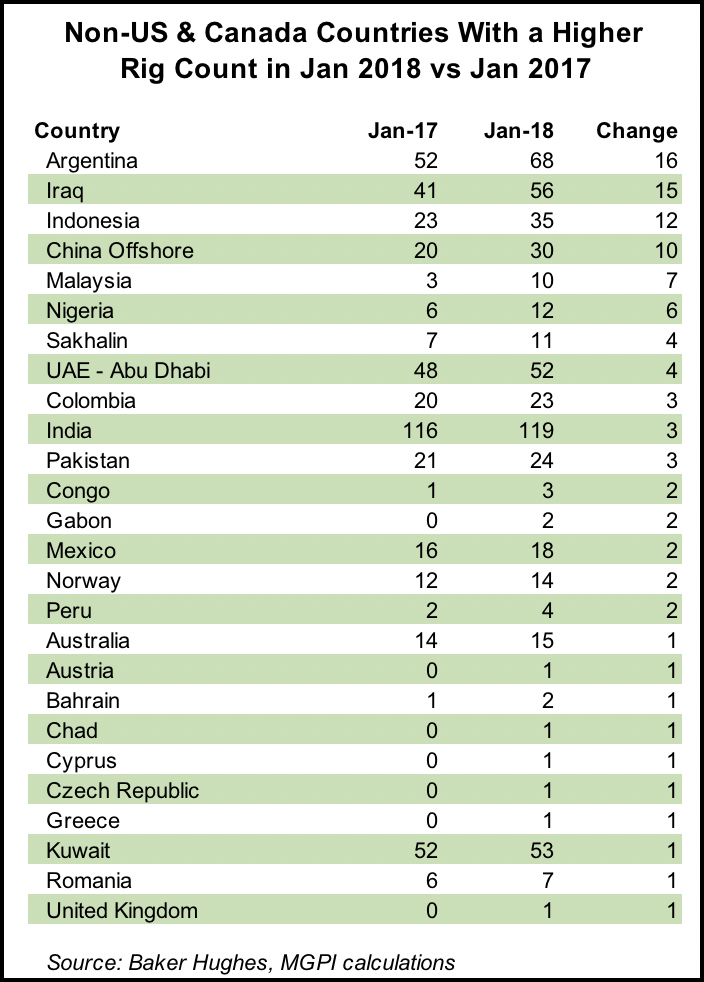

For the Organization of the Petroleum Exporting Countries (OPEC), nearly all of its growth in the next half-decade is seen coming from Middle East cartel members. OPEC member Venezuela has seen its oil production fall by more than half in the past 20 years, and declines are expected to accelerate.

“Sharply falling production in Venezuela will offset gains in Iraq, resulting in OPEC crude oil capacity growth of just 750,000 b/d by 2023,” IEA said. “Unless there is a change to the fundamentals, the effective global spare capacity cushion will fall to only 2.2% of demand by 2023, the lowest number since 2007.”

Declining oil and gas costs have helped producers, but researchers said investments outside the United States are necessary to spur supplies after 2020.

“The oil industry has yet to recover from an unprecedented two-year drop in investment in 2015-2016, and the IEA sees little-to-no increase in upstream spending outside of the United States in 2017 and 2018.”

Economic growth in Asia and a resurgent U.S. petrochemicals industry should lead to a 6.9 million b/d increase in oil demand by 2023 to 104.7 million b/d, according to the IEA.

China is forecast to remain the main engine of global demand growth. However, the country’s more stringent policies to curb air pollution may slow growth.

Meanwhile, the increasing penetration of electric buses and LNG-fueled trucks may have a bigger impact on curbing consumption of transport fuels than the electrification of passenger vehicles, IEA said.

In the United States, fuel-economy standards for passenger cars are seen curbing gasoline demand, but growth should come from the petrochemical sector, now thriving because of low-cost ethane.

“New global petrochemicals capacity will account for 25% of oil-demand growth by 2023,” according to IEA’s U.S. forecast.

Meanwhile, a new marine fuel rule with lower sulfur content that is to come into force in 2020 is creating uncertainty in the market.

IEA’s annual forecast also examines crude quality issues arising from the rapid increase in U.S. production, changing trade flows and a growing global refining capacity surplus.

“Global oil trade routes are moving East, as China and India replace the United States as top oil importers. With seaborne oil traveling longer distances, energy security, one of the IEA’s core missions, will remain as critical as ever.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9966 |