NGI Weekly Gas Price Index | Markets | NGI All News Access

Weekly NatGas Cash, Futures Take Last Summer Vacation As Markets Show Small Moves

Apart from some weather and power-price driven gains on the East and West Coasts, weekly natural gas prices moved little for the week ended August 19 with producing basins and Midwest market centers moving within a few pennies of unchanged.

The NGI Weekly Spot Gas Average eased 2 cents to $2.51. Futures trading was equally uninspired with modest gains made following the weekly Energy Information Administration (EIA) storage report being given back and then some in Friday’s trading.

The Northeast proved to be home to market points showing the week’s greatest gainers and losers with Algonquin Citygate and Iroquois Zone 2 both adding 33 cents to $3.68 and $3.55, respectively. Bringing up the rear was Tennessee Zone 5 200 L with a 25 cent decline to $2.83.

Regionally California proved to be the week’s greatest gainer with a rise of 7 cents to $2.88 and the Rocky Mountains were at the opposite end of the spectrum with a loss of 8 cents to $2.47.

The Midcontinent shed 7 cents to $2.52, and three regions South Texas, East Texas, and the Midwest all lost 4 cents to $2.59, $2.60, and $2.63, respectively.

South Louisiana was seen 3 cents lower at $2.62, and Appalachia came in a penny lower at $1.40. The Southeast added a penny to $2.75 and the Northeast crept into the win column with a 4 cent advance to average $2.83.

September futures scored one of the smallest weekly moves on record losing two-tenths of a cent to $2.584.

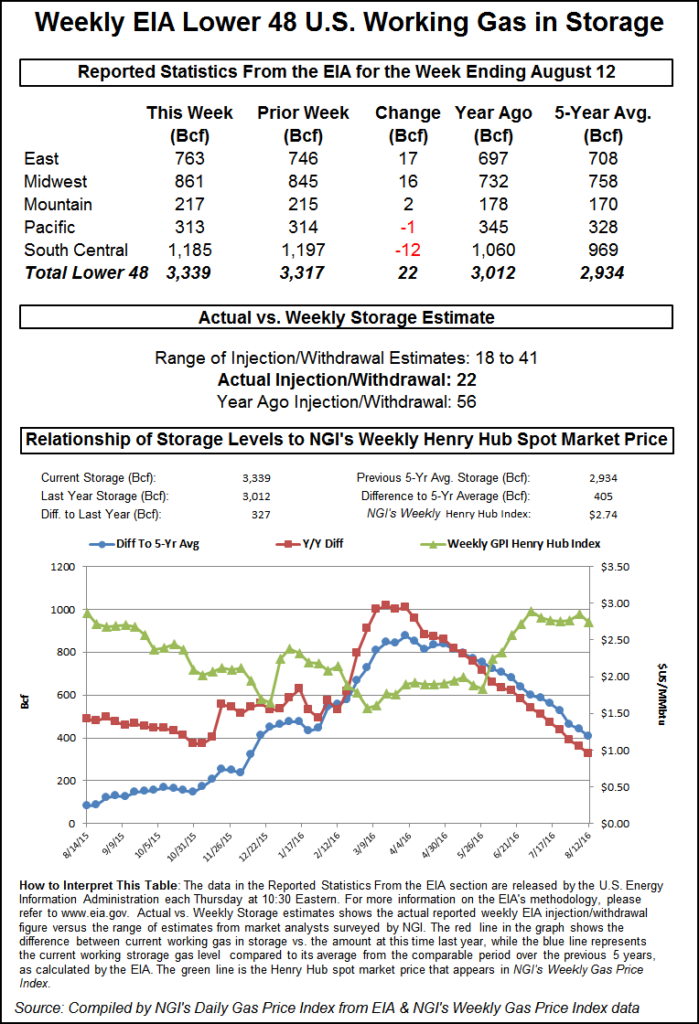

Futures bulls Thursday awakened from their sleep of the previous few sessions and managed to post a nickel gain on the heels of moderately constructive storage figures. The EIA reported a build of 22 Bcf, about 5 Bcf less than market expectations, and at the close on Thursday September had added 5.5 cents to $2.674 and October had risen 5.3 cents to $2.712.

When the 22 Bcf storage figure rattled across trading screens, the result had bulls in the driver’s seat. September futures reached a high of $2.675 immediately after the figures were released and by 10:45 a.m. September was trading at $2.654 up 3.5 cents from Wednesday’s settlement.

“It seems like the market moves, and then we go right back to where we were,” a New York floor trader told NGI.

“Crude oil was less than $40 not too long ago, and think about it. You are up almost $10 in crude. Natgas bulls should be grateful for crude oil, but we are still stuck in that range between $2.50 to $2.75.”

“The data for last week showed a somewhat smaller than expected 22 Bcf net injection into US natural gas storage,” said Tim Evans of Citi Futures Perspective. “While not a major surprise, this suggests some ongoing volatility from prior weeks that had featured both an unexpected 6 Bcf withdrawal and then a larger than expected 29 Bcf build. The market continues to show greater sensitivity to extreme summer heat than anticipated.

“The market does keep making progress in reducing the storage surplus, which remains constructive for the intermediate term, but doesn’t necessarily preclude a further downside price correction in our view.”

Inventories now stand at 3,339 Bcf and are 327 Bcf greater than last year and 405 Bcf more than the five-year average. In the East Region 17 Bcf were injected and the Midwest Region saw inventories increase by 16 Bcf. Stocks in the Mountain Region rose 2 Bcf, and the Pacific Region was lower by 1 Bcf. The South Central Region shed 12 Bcf.

In Friday’s trading physical natural gas for weekend and Monday delivery and the September futures contract joined hands and both waltzed to similar declines.

Most producing zones and the Midwest market zone came in about a nickel lower, but outsize declines in and around New York City and Southern California skewed the averages lower. The NGI National Spot Gas Average fell 10 cents to $2.38, and futures fared equally poorly. At the close, September futures had fallen 9.0 cents to $2.584 and October had shed 9.3 cents to $2.619. The about-to-expire September crude oil contract continued to press the upside with a rise of 30 cents to $48.52/bbl.

Midcontinent pricing for the weekend and Monday delivery was unaffected by a Northern Natural force majeure in West Texas that was lifted later in the day.

Gas for delivery on ANR SW fell 4 cents to $2.42 and deliveries to the NGPL Midcontinent Pool also dropped 4 cents to $2.49. Packages priced at Northern Natural Demarcation skidded 9 cents to $2.52, and gas at Northern Natural Ventura shed a dime to $2.52. Gas on Panhandle Eastern fell 6 cents to $2.41.

Weekend and Monday gas in southern California retreated as Monday on-peak power in California and market points serving California declined. Intercontinental Exchange reported that on-peak Monday power at NP-15 fell $2.08 to $37.50/MWh and Monday power at SP-15 gave up $2.28 to $37.05/MWh. Monday power at COB tumbled $11.72 to $29.47/MWh.

Deliveries to the PG&E Citygate were quoted 6 cents lower at $3.12 but gas at the SoCal Citygate came in 16 cents lower at $2.63, and gas priced at the SoCal Border Avg. changed hands 15 cents lower at $2.56. Gas on El Paso S. Mainline/N. Baja also gave up 15 cents to $2.59, and Kern Delivery shed 16 cents to $2.57.

Expected lower power loads in New York City helped take some of the bite out of weekend and Monday gas pricing. The New York ISO forecast that New York City’s peak power load Friday of 9,573 MW would take its predictable drop Saturday to 8,367 MW, but by Monday peak power was estimated at only 9,263 MW.

Gas bound for southeasternmost Pennsylvania, Trenton, and southern New Jersey on Transco Zone 6 non-NY North skidded 38 cents to $1.58, and gas headed for New York City on Transco Zone 6 gave up 46 cents to $1.55.

Futures opened lower and continued downward throughout the day on Friday, according to one market observer. Overnight weather models predicted more severe temperature declines in the middle third of the country, and when the midday model updates rolled around they supported this trend through August 28. The 11-15 day forecast was warmed at midday, but declining normals and the upcoming Labor Day holiday likely caused this period to be less important as a pricing mechanism.

Analysts see ending storage at close to last year’s record levels, but they recommend standing aside the market for now.

“This market [had] received a lift off of a supportive EIA storage figure as well as some minor bullish adjustments to the short-term temperature views,” said Jim Ritterbusch of Ritterbusch and Associates in a Friday morning note to clients. “Expected cooling across a large portion of the nation’s Midcontinent is giving way to some normalization while hot temps along the Eastern Seaboard are looking a bit more pronounced.

“Additionally, this year’s combination of reduced production and increased electricity generation demand continues to eat away at a large surplus that has been cut by more than half for this year. Yesterday’s smaller than expected storage increase cut the overhang to 405 Bcf, and additional reductions would appear to lie ahead. But with end-of-season supply still headed toward the 4 Tcf level, in our view, storage would appear ample to easily meet the needs of an unusually cold winter.”

Gas buyers for power generation across the PJM footprint will have a modest amount of wind generation to offset power purchases over the weekend. “Warm, humid and occasional stormy conditions will give way a cooldown. Seasonably hot and moderately humid conditions are expected across the majority of the power pool during the next couple of days, but this air mass will trigger scattered thunderstorms each day,” said WSI Corp. in a Friday morning report.

“High temps will generally vary in the 80s to low 90s. Minimums will range in the mid 60s and 70s. A cold front will traverse the power pool from west to east with rounds of showers and thunderstorms late Saturday into early Monday morning. It will remain warm and humid ahead of the front, but a cooler and drier air mass will filter into the power pool early next week. High temps will retreat into the 70s to mid 80s. Minimums will dip into the 50s and 60s.

“A southwest-to-northwest wind associated with a cold front will lead to a sharp boost in wind generation tonight through early Monday with output around 3-4 GW. High pressure will cause wind and wind gen to drop off early next week.”

At 5 p.m. EDT Friday the National Hurricane Center (NHC) reported that Tropical Storm Fiona continued on its trajectory toward Bermuda and was 1,130 miles east of the Lesser Antilles. It was traveling west-northwest at 10 mph, and maximum sustained winds were 40 mph. NHC also identified a tropical wave 600 miles southwest of the Cabo Verde Islands and gave it a 10% chance of tropical storm formation within the succeeding 48 hours.

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |