Shale Daily | E&P | NGI All News Access

EIA Forecasts Modest Gains For Oil, NatGas Benchmarks In 2017

Debuting its 2017 forecasts with the release of its Short-Term Energy Outlook Tuesday, the Energy Information Administration (EIA) is projecting modest gains for both crude oil and natural gas benchmarks to arrive next year as the market slowly adjusts to the current oversupply.

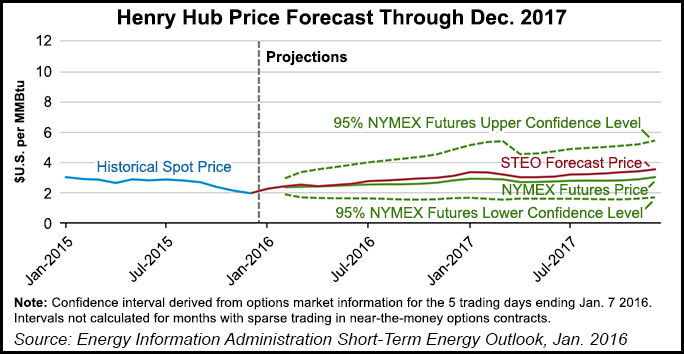

At the Henry Hub, EIA said it expects an average price of $2.73/Mcf in 2016, with the price jumping to $3.32/Mcf in 2017. Total dry gas production will remain essentially flat in 2016 at 74.82 Bcf/d, up slightly from 74.45 Bcf/d in 2015, according to EIA’s projections. In 2017, production is expected to increase to 76.21 Bcf/d.

An increase in exports and a decrease in Canadian imports are expected to help sustain current gas production levels even as domestic consumption levels off, EIA said. Demand for gas in Mexico is expected to increase as a result of growth in its electric power sector, while Cheniere Energy Inc.’s Sabine Pass liquefied natural gas (LNG) terminal is expected to add to an increase in U.S. gas exports as it comes online this month, EIA said. Driven by activity at Sabine Pass, gross U.S. LNG exports will average 0.7 Bcf/d in 2016, increasing to 1.4 Bcf/d in 2017, EIA said.

U.S. crude oil production is expected to slide this year and in 2017, EIA said. The 9.43 million b/d produced in 2015 will decline to 8.73 million b/d in 2016 and 8.46 million b/d in 2017. Brent crude prices are expected to average around $40/bbl in 2016 before climbing to $50/bbl in 2017, with West Texas Intermediate (WTI) trading $2/bbl less in 2016 and $3/bbl less in 2017, EIA said.

In a conference call with reporters Tuesday, EIA Administrator Adam Sieminski said a recovery is on the horizon for the commodity markets that took such a beating in 2015.

“I’ve been following the energy sector of the global economy for a lot of years. I’ve seen prices for various energy products go up and go down, and I’ve weathered through a bunch of cycles. I think we are likely to see prices recovering because that’s typically what they do,” Sieminski said. “You tend to get overreactions both to the upside and the downside, and now we’re in one of those likely dips that go below what replacement costs really are, so we’ll see a recovery, but there’s a lot of pain involved in this.”

Sieminski said he doesn’t think Congress’s lifting of the crude oil export ban will have much market impact unless the WTI-Brent spread “really opens back up again, and we don’t expect that that’s going to happen.”

Domestic oil and gas producers were “very clever” at finding ways to increase efficiency and continue production growth in 2015 despite a dropping rig count necessitated by depressed prices.

“I think it took longer for the U.S. production to slow down than we would have anticipated a year ago,” Sieminski said, though he added that domestic producers are “getting closer to a point where you’re turning and things will start to get better.”

EIA Senior Economist Tancred Lidderdale said the decisions coming from the Organization of the Petroleum Exporting Countries (OPEC) have been another factor in prices, adding that production from those countries “really has been surprising us on the upside.”

Sieminski said forecasts of demand growth for crude oil suggest that prices will have to recover at some point as the market rebalances.

“Longer term, whether fuel efficiency standards for automobiles and changes in carbon rules and so on put some downward pressure on oil demand, that’s a big, long, complicated issue, but in the near term, demand is going to go up and so production has to respond to that,” Sieminski said. “I think the problem that we’ve had for the past year is that production has continued, actually, to stay at levels higher than demand, and the inventories have been building, and so we’ve got to work our way through those inventories.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 2158-8023 |