NGI Archives | NGI All News Access

NatGas Market Prices Drop As Winter Fades; April Futures Expire Sub-$2.60

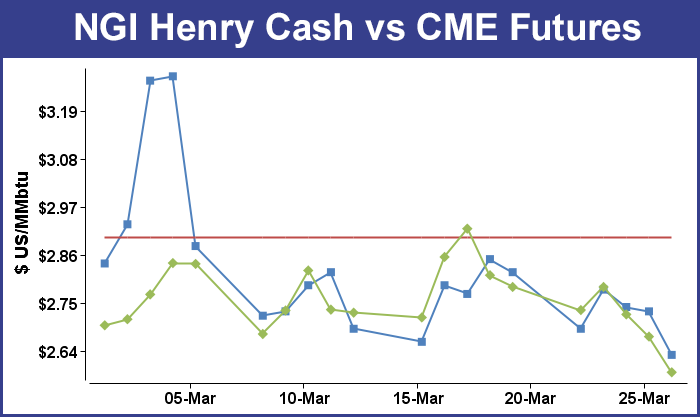

For the week ending March 27, physical natural gas prices dropped from a couple of pennies to a dime at points across the country as spring began to make an appearance and the industry digested the first storage injection of the year. April futures expired Friday at $2.590, down 19.6 cents from the previous week’s finish.

NGI‘s Weekly Natural Gas spot Average for the week declined 23 cents to $2.56, helped significantly by the Northeast Region, which declined 66 cents for the week to the same average of $2.56. All other major regions saw much smaller declines that ranged from a nickel to 7 cents. Only three individual indexes registered gains or were unchanged for the week. Westcoast Station 2 in Canada added 33 cents to average $1.59 and Tennessee Zone 4 Marcellus gained 2 cents to $1.42, while Transco-Leidy Line went unchanged at $1.49.

Besides April futures expiration, the big news on the week was the first injection to gas storage for the year.

For the week ended Mar. 20 the Energy Information Administration (EIA) reported an increase of 12 Bcf in its 10:30 a.m. EDT release Thursday, which sent futures values scurrying lower. Prior to the release of the data, analysts were looking for an increase averaging less than 10 Bcf. A Reuters survey of 22 traders and analysts showed an average 6 Bcf build with a range of minus 7 Bcf to plus 25 Bcf.

Most eyes on Friday were on the expiring April natural gas futures contract, which failed to recover from Thursday’s bearish storage injection. The front-month contract traded a slim $2.604 to $2.675 range before terminating at $2.590, down 8.2 cents from Thursday’s finish. The May contract moved in lockstep, dropping 4.9 cents from Thursday’s close to $2.639.

Traders see the market’s decline consistent with their market objectives. Steve Mosley of the SMC Report said, “we have seen the market give back all of last week’s gains and we are currently in another serious downward test of the $2.567 low.

“We will just have to see how this plays out as to whether this week’s downward market move is just part of the relatively brief, wide-swinging, upwardly biased consolidation that we expected for this year’s pre-summer recovery, or whether it is going to result in a late continuation of the winter seasonal decline that would finally achieve our $2.20-$2.55 winter target range.”

Other traders saw a bearish report but still within the framework of a broad trading range. “Earlier in the week I was hearing negative numbers, but as of yesterday I was hearing +6 Bcf. We are still in a trading range from $2.50 to $3 and not much has changed,” said a New York floor trader.

“The build for last week was more than expected and also bearish compared with the 20-Bcf five-year average net withdrawal,” said Tim Evans of Citi Futures Perspective. “It also suggests a weaker background supply/demand balance, with bearish implications for the reports to follow relative to the base case.”

Inventories now stand at 1,479 Bcf and are 575 Bcf greater than last year and 194 Bcf below the five-year average. In the East Region 22 Bcf was withdrawn and the West Region saw inventories increase by 6 Bcf. Stocks in the Producing Region rose by 28 Bcf.

“It is continuing to be a market where the supply just keeps coming on and our demand was moderate as we left this winter,” said David Thompson, executive vice president of Washington, DC-based energy brokerage firm Powerhouse. “I think that is why we’ve had this slow but steady decline in natural gas futures values. The interesting thing is the natural gas community has the ability to teach the oil guys a lesson. When you look at the continuing decline in natural gas rigs, which has been going on for years now, and look at the continued increase in natural gas production, the oil side should take notice. They are wondering about the reduction in rigs and when that is going to translate into a decline in crude oil production. They might want to ask their gas friends how that goes. There are some smart engineers in this country, and when the price is right, they find a way to do things.”

With futures currently under $3, Thompson told NGI the next support is in the $2.550 to $2.570 area, and below that is the April 2012 low of $1.902, but he doesn’t foresee any sort of freefall.

Physical natural gas prices nationally for weekend and Monday delivery were a sea of red ink on Friday as traders studied weather forecasts calling for colder Canadian air to mostly stay north of the border. The only points that recorded gains Friday were the Algonquin Citygate and those tied to the Marcellus Shale, which often times follow their own set of fundamentals due to the region’s complex lineup of supply glut and capacity constraints. Moderating weather forecasts had most market points declining by a dime or more, as traders squared their books ahead of the weekend. Of significant note was the SoCal Citygate 21-cent decline to average $2.46.

Marcellus points painted an interesting picture on Friday for weekend and Monday delivery as Columbia Gas, which is typically the market leader among the Marcellus/Utica pipes, fell 11 cents to average $2.54, while Dominion North, Dominion South, Tennessee Zone 4 Marcellus, and Transco-Leidy line all posted daily gains.

King of the large swings for the last couple of weeks, Algonquin Citygate, and Tennessee Zone 6 200 Line kept their titles Friday. Algonquin jumped $3.79 to average $8.94 and Tennessee Zone 6 200 Line added $2.54 to average $7.85.

Canadians could be keeping their latest burst of cold air if forecasters at NatGasWeather are to be believed. “The latest weather data continues streaming in and so far we still don’t see any significant changes showing up through the first week of April, and believe the onus remains on cooler temperatures proving they will continue spilling into the northeastern U.S. during the second week of April or weather sentiment will trend more bearish,” NatGasWeather said Friday afternoon. “There will remain very cold air over Canada in April, which is always a bit unnerving; however, the data has still yet to prove it will aggressively push across the border.”

The forecasters noted that weather data “continues struggling” on what the second week of April might bring, but would need to trend convincingly colder to prevent longer-term weather sentiment from becoming more bearish.

Andrea Paltrinieri, who analyzes natural gas markets for NatGasWeather, said the decline in futures prices on Friday was likely the market digesting Thursday’s above estimates number, that showed the first injection of the shoulder season. She added that the market’s focus will now be on weather patterns, “trying to evaluate if the models trend warmer during the weekend, and for next Thursday’s [storage] number, that now seems to be another draw. Given that we are now entering into the shoulder season, we have to expect some softness in prices until we see some signs of increased demand due to switch from coal or stronger nuke outages.”

Attention is also being paid to the U.S. production forecast and what this summer might look like. In a Genscape webinar on Wednesday, senior natural gas analyst Rick Margolin and Randall Collum, managing director of supply side analytics, presented the firm’s domestic summer supply and demand forecast.

Genscape’s outlook for U.S. gas production is well below what it was last August, all because of the decline in crude and gas prices. “April 2015 crude is trading about $50 lower than it was back in August. And natural gas is trading almost $1.00 down,” Collum said. “The one thing that keeps production propped up even as rigs have already been dropping is the deferred inventory that’s already been built up from pad drilling over the last year or so,” the drilled but uncompleted wells. “It takes a while before that price actually impacts the production. Right now we’re seeing about a five- to six-month lag between a price impact and a rig impact, and then another two- to three-month, sometimes four or five, before you a actually see a production impact on that.”

Genscape now is calling for gas production overall to peak in the May-June period. “That’s about a seven-month lag between when the rig count peaked at the end of October 2014. For this summer, we’re thinking we’re going to see around a 3.3 Bcf/d [production] year-on-year increase. It’s slightly lower than last year’s summer increase, where we had a 4.3 Bcf/d year-on-year increase.”

Turning attention back to futures, Jim Ritterbusch of Ritterbusch and Associates is also reading a lot into receiving the first storage injection of the season and “anticipates gradual downside price follow-through going forward. The 12 Bcf injection was only a few Bcf larger than industry ideas. But the market appeared to be responding to the fact that the increase developed a couple of weeks earlier than normal and was partially reflective of a significant production upswing.

“The supply shortfall against five-year average levels narrowed to 194 Bcf and will likely disappear next month if temperature forecasts shift toward the mild side,” Ritterbusch said. “We still see the dynamic of rising production as a key pricing determinant during the next couple of months that will require further discounting. We suggest simply staying with the program for now in maintaining any shorts established above the $2.82 level as we still target the $2.50 area. The breakdown in the May contract to lowest level since early February will place longs on the defensive well into next month.”

Gas buyers for power generation across the MISO footprint were expected to have their hands full going into the weekend as forecasts called for cold along with fluctuating renewable supplies. WSI Corp. in its Friday morning outlook said, “Unseasonably cold high pressure will continue to slide across the power pool during the next one to two days. Highs may only range in the 30s, 40s to low 50s along with lows in the teens, 20s and 30s. High pressure will gradually depart during the weekend, which may lead to a moderating trend. However, a fast-moving Alberta Clipper may race across the power pool late Saturday night into Sunday with a chance of rain and snow showers, as well as gusty winds.

“Wind generation is expected to subside and become relatively light [Friday]. Wind gen is expected to ramp back up and become strong during the weekend due in part to the clipper. Output may peak near 8-10 GW during Saturday night into Sunday. Wind gen will likely subside from this peak but may remain elevated early next week.”

© 2024 Natural Gas Intelligence. All rights reserved.

ISSN © 2577-9877 | ISSN © 1532-1258 |